GST Cancellation & Revocation

Restore or cancel your GST registration effortlessly with RegisterKaro. We handle compliance, documentation, and filing, ensuring fast GSTIN revival under Rule 23 of the CGST Rules.

What is the Revocation of Cancellation of GST Registration?

Revocation of cancellation of GST registration means getting your cancelled GST number back. If the GST officer cancels your registration because you didn’t follow the rules, you can apply to get it restored by filling out Form GST REG-21 within 30 days of the cancellation order. But this is only allowed if the officer initiated the cancellation, not if you cancelled it voluntarily.

Before applying, you must file all pending GST returns and pay any taxes due. If everything is in order, the officer may approve your request, and your GST registration will become active again so you can continue your business legally.

What is the Cancellation of GST Registration?

Cancellation of GST registration means that your GST number is no longer active and you are not allowed to collect GST or file GST returns anymore. It’s like officially closing your GST account with the government.

This usually happens when:

- You stop doing business

- Your business is transferred or merged

- You don’t need GST anymore (like your turnover is below the limit)

- You break the GST rules, and the government cancels it

After cancellation, you must stop issuing GST invoices, and you won’t be able to claim input tax credit.

Who Can Cancel GST Registration?

GST registration can be cancelled by different parties depending on the situation.

1. Cancellation by the Business Owner (Voluntary Cancellation)

If you're a registered taxpayer and no longer require GST registration, you can apply for cancellation voluntarily. Common reasons include:

- Closure of business

- Turnover has fallen below the GST threshold

- Change in business structure (e.g., sole proprietorship to partnership)

2. Cancellation by the GST Department

The GST department can cancel your registration on its own (suo moto) under the following conditions:

- Failure to file GST returns for a continuous period

- Registration obtained using false information

- Violation of GST provisions

3. Cancellation by Legal Heirs (In Case of Death)

If a sole proprietor passes away, the legal heirs or family members can apply to cancel the GST registration of the deceased.

Forms You May Need During the Cancellation Process

To successfully cancel your GST registration, certain forms must be submitted depending on who initiates the cancellation and why.

| Form Name | Purpose |

| GST REG-16 | Application for voluntary cancellation |

| GST REG-17 | Show Cause Notice from the GST officer |

| GST REG-18 | Reply to notice issued under REG-17 |

| GST REG-19 | Final order for cancellation |

| GST REG-20 | Order for dropping cancellation proceedings |

| GSTR-10 | Final return after cancellation (mandatory) |

Who Can’t Cancel GST Registration?

Certain types of registered persons are not allowed to cancel their GST registration:

- TDS/TCS Deductors: People registered only to deduct/collect tax can't cancel registration.

- UIN Holders: Foreign embassies or UN bodies with a Unique ID Number (UIN) cannot apply for cancellation. They get UINs just to claim refunds.

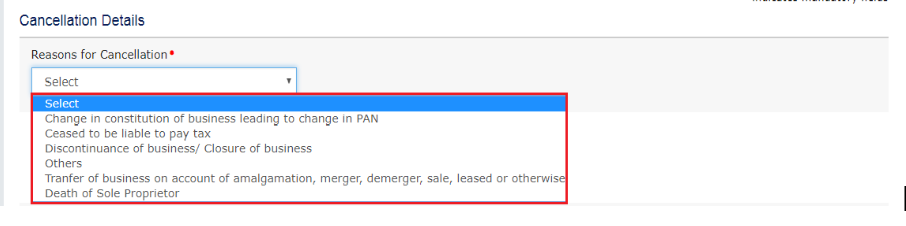

Reasons for GST Cancellation

There are several situations where GST registration may need to be cancelled. This section lists the main reasons why a taxpayer or the GST department might decide to cancel it.

1. When a Business Owner Requests Cancellation

- Business is closed

- Business is sold or merged

- Business type changed

- Turnover below the GST limit

- Wants to cancel registration for any personal/business reason.

2. When the GST Officer Cancels

- Not filing GST returns (6 months for regular, 3 for composition)

- Got GST by giving false information

- Breaking GST laws

- Doing fake or illegal business

- Not started a business after getting GST

- Claiming wrong Input Tax Credit (ITC)

Time Limit for Cancellation

Learn about when you need to apply for cancellation and how much time you have to do it.

- Voluntary: You can apply for cancellation anytime after registration if you're no longer required to be under GST.

- By Officer: Cancellation starts automatically if you don't file returns for 6 months (or 3 months for composition).

- Important: Apply for cancellation within 30 days of stopping business or for any other reason.

Consequences of GST Cancellation

Cancelling GST registration brings certain changes and responsibilities for the business.

- Stop Charging GST: You can’t charge GST on your bills after cancellation. Update your invoices accordingly.

- No Input Tax Credit: You can't claim credit on purchases after cancellation. You may also have to pay tax equal to the ITC on any remaining stock.

- File Final Return: You must file a final return (Form GSTR-10) within 3 months of cancellation.

- Keep Records: You must keep all business records for 6 years after cancellation for audits or inspections.

- Legal Trouble: If you don't file the final return or pay taxes due, you may get penalties or face legal issues.

- Business Impact: Your operations may be affected. To restart GST, you must apply again and go through checks.

- Refunds: If you paid extra GST, you can get a refund—apply within the time limit.

- PAN-Wide Effect: If your business has GST in many states or verticals, cancellation in one may affect all with the same PAN.

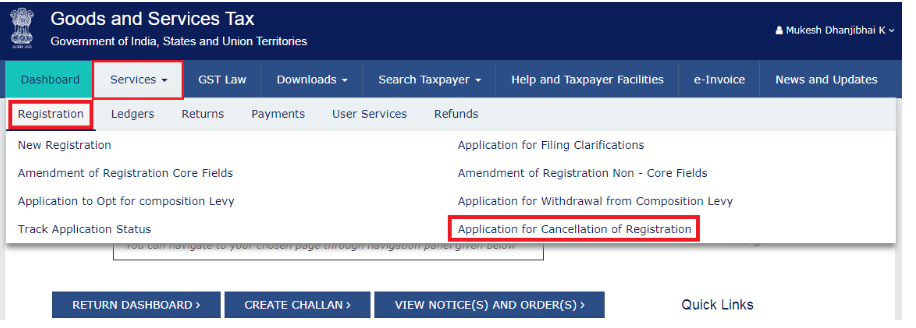

How to Cancel GST Registration in India?

Follow these easy steps to apply for cancellation through the GST portal.

- Log in to gst.gov.in

- Go to Services > Registration > Application for Cancellation

- Enter Details like:

- Reason for cancellation

- Date of cancellation

- Details of remaining stock and ITC

- Pay Dues: Make sure all returns are filed and dues are cleared with the cancellation effective date.

- Submit Application using Digital Signature Certificate (DSC) or OTP (EVC).

- Get ARN: You’ll receive an Acknowledgement Reference Number to track your application.

- Officer Review: GST officer may ask for more info—reply if needed.

- Cancellation Order: If everything is okay, you’ll get Form GST REG-19 with the cancellation date.

Understanding Rule 23: Revocation of Cancelled GST Registration

Rule 23 of the GST Rules allows taxpayers to request the restoration of their cancelled GST registration.

Form GST REG-21: Application for Reversal of GST Cancellation

If a GST officer cancels your registration, you can request to get it back by filing Form GST REG-21. This form must be submitted within 30 days of the date you received the cancellation order.

If your GST registration was cancelled because you did not file your GST returns, you can file Form REG-21 only after submitting all the pending returns and paying any interest or late fees due.

Follow the steps below to file GST REG-21 for revocation of GST registration:

Step 1: Log in to the GST Portal

Go to the GST portal, log in with your credentials, and go to ‘Services’ > ‘Registration’ > ‘Application for Revocation of GST Registration Cancellation’.

Step 2: Fill in the Details

Enter the required details and mention the reason why your GST registration should be restored.

You can also attach any supporting documents, if needed.

Once all the information is filled in, tick the verification checkbox, choose the authorised signatory and place, and move to the next step.

Step 3: Submit the Application

File Form GST REG-21 using either your Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

Once submitted, you will get a confirmation message saying that your application has been successfully filed.

Form GST REG-23: Notice for Cancellation of Revocation Application

This form is issued by the GST officer when they are not satisfied with the revocation application submitted by the taxpayer whose GST registration was cancelled. It acts as a show-cause notice, giving the taxpayer an opportunity to explain why the revocation should not be rejected.

- Purpose: To notify the taxpayer that the application for revocation of cancellation is being considered for rejection.

- Response Time: The taxpayer must respond within 7 working days from the date of issue.

Form GST REG-24: Reply to Show-Cause Notice (REG-23)

If a taxpayer receives a notice in Form REG-23, they must submit their reply through Form REG-24. This form allows the taxpayer to present their justification, provide additional documents, and explain why the revocation application should be accepted.

- Purpose: To reply to the officer’s concerns raised in REG-23.

- Deadline: Must be filed within 7 working days from the date of the REG-23 notice.

Last Update: The government had allowed a one-time extension under Notification No. 03/2023 for taxpayers whose GST registration was cancelled on or before 31st Dec 2022. They could apply for revocation until 30th June 2023 after filing pending returns and clearing dues.

Who Else Can Apply Under This Extension?

The following taxpayers can also apply for revocation under this extended window:

- Those whose appeal against cancellation was rejected due to late filing.

- Those whose appeal against the rejection of the revocation application was dismissed due to time limits.

CBIC Circular on Extended Revocation Period

The CBIC issued Circular No. 158/14/2021-GST on 6th September 2021 to explain the earlier extension given under Notification No. 34/2021 dated 29th August 2021.

- This allowed taxpayers whose revocation deadline expired between 1st March 2020 and 31st August 2021 to apply for revocation by 30th September 2021.

- Many taxpayers were confused about whether they could apply again if their previous application was rejected, in process, or an appeal.

The circular clarified that the relief applies to all such cases, regardless of whether the revocation application was:

- Already applied

- Under review

- Rejected

- With appellate authority

Key Steps to Follow When Applying for Revocation of a Cancelled GST Registration

Revocation of GST registration means reactivating your GST number after it has been cancelled by the tax department. Follow the steps below to apply:

Step 1: Check Eligibility

Make sure that the GST registration was cancelled by the GST officer (not voluntarily by you) and that you are applying within 90 or 180 days from the date of the cancellation order.

Step 2: Review the Cancellation Order

Go through the reasons mentioned in the cancellation order carefully and identify the compliance issues that led to the cancellation.

Step 3: Fix Compliance Issues

Before applying, file all pending GST returns and clear any outstanding dues, including applicable interest, late fees, and penalties.

Step 4: Log in to the GST Portal

Visit the GST Portal and log in using your user ID and password. Go to ‘Services > Registration > Application for Revocation of Cancellation’.

Step 5: Fill Form GST REG-21

Complete the application in Form GST REG-21, clearly stating the reason for revocation, and attach supporting documents, such as return filing confirmations and payment receipts.

Step 6: Upload Required Documents

Ensure all documents are properly formatted, clear, and relevant. Attach them to support your revocation request.

Step 7: Submit the Application

Use your Digital Signature Certificate (DSC) or e-Signature (EVC) to complete the application submission process.

Step 8: Track the Application

After submission, keep checking the application status on the GST portal. If you receive any notices or queries from the GST officer, respond quickly.

Step 9: Outcome – Approval or Rejection

If the officer is satisfied, your GST registration will be restored. If it’s rejected, the reasons for rejection will be shared, and you will have the option to appeal the decision if needed.

How Long Does the Revocation Process Typically Take?

The process to revoke a cancelled GST registration generally follows a set timeline. Here’s how it usually works:

1. Application Submission

After receiving the cancellation order, the taxpayer has up to 90 days to apply for revocation by filing Form GST REG-21.

2. Officer’s Processing Time

Once the application is filed, the GST officer has 30 days to review it and either:

- Approve it by issuing Form GST REG-22, or

- Reject it using Form GST REG-05

3. Responding to Show Cause Notice

If the officer is not satisfied with the application and issues a show cause notice (Form GST REG-23), the taxpayer must reply within 7 working days using Form GST REG-24.

4. Final Decision After Reply

Once the officer receives the response, they will assess the reply and take a final decision within the next 30 days.

5. Overall Timeline

In total, the revocation process may take around 2 to 3 months, depending on the following:

- How quickly the application is submitted

- Timely response to any notices from the GST officer

- Complexity of the case, or if additional clarifications are needed

If all actions are completed on time and there are no complications, the revocation process can be completed smoothly within this period.

Fees for GST Cancellation & Revocation

Cancelling or revoking your GST registration on the GST portal does not involve any government charges. However, if you take help from a tax consultant or a CA, they may charge a professional fee based on the service provided.

| Service | Form Used | Government Fee | Professional Fee (if hired) | Remarks |

| GST Registration Cancellation | Form GST REG-16 | ₹0 | ₹500 – ₹1,000 (approx.) | No fee if done through the GST portal. Professionals may charge for assistance. |

| Revocation of GST Cancellation | Form GST REG-21 | ₹0 | ₹1,000 – ₹2,000 (approx.) | No government fee. File within 30 days of cancellation order. |

| Reply to Show Cause Notice | Form GST REG-24 | ₹0 | ₹500 – ₹1,500 (approx.) | Reply to the REG-23 notice. Professional help may be required. |

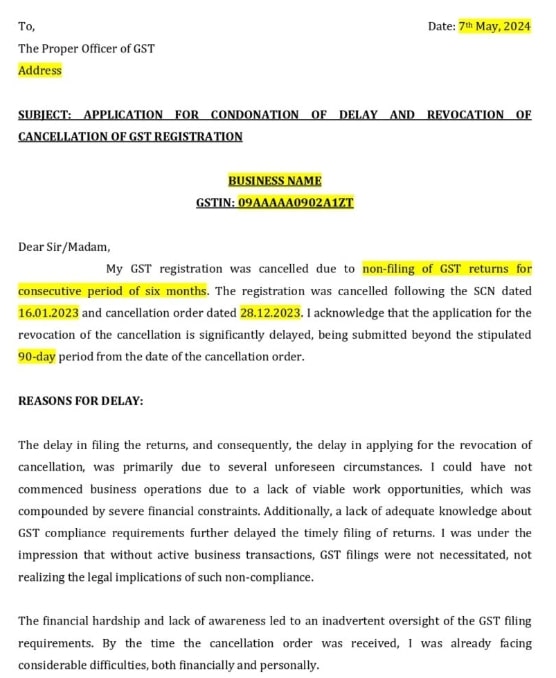

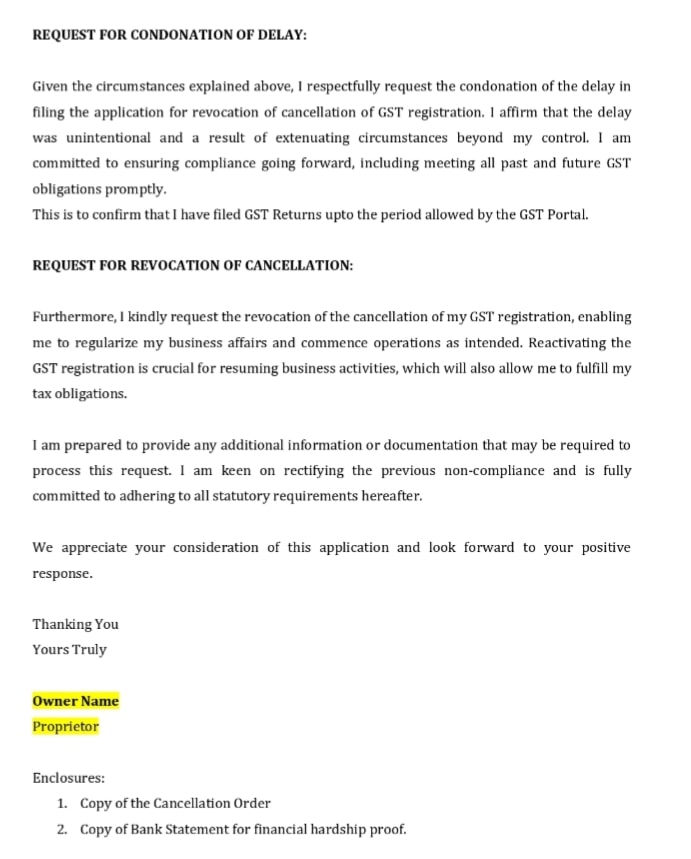

GST Revocation Letter Format

A GST revocation letter is written by the taxpayer to request the reinstatement of their cancelled GST registration. Below is a sample format to help you draft a proper revocation request letter.

GST Revocation Letter Sample Format Page-1

GST Revocation Letter Sample Format Page-2

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

What is the GST revocation rule?

−The GST revocation rule (Rule 23 of the CGST Rules) allows a taxpayer to apply for restoration of their GST registration if it was cancelled by a GST officer. The application must be submitted using Form GST REG-21 within 30 days (extendable in some cases) from the date of the cancellation order.

What is the difference between GST cancellation and revocation?

+How do I revoke GST registration after 90 days?

+How do you write a reason for revocation of GST?

+Can GST be revoked after 180 days?

+Can GST be revoked after 270 days?

+What happens when GST registration is cancelled?

+Can I voluntarily apply for GST revocation?

+What is the GST Revocation Appeal Time Limit?

+What happens to my Input Tax Credit (ITC) if my GST registration is revoked?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for the GST Cancellation & Revocation Service?

When it comes to restoring your cancelled GST registration, having the right support can make all the difference. At RegisterKaro, we simplify the process and ensure your business gets back on track, fast and easy.

- Expert Help: Our GST experts know the rules under Rule 23 and have helped thousands of businesses get their GST numbers back.

- Fast Process: We handle everything, from filing Form REG-21 to replying to notices, so you can restart your business without delay.

- Full Support: We guide you at every step, from checking your cancellation order to clearing compliance issues and pending returns.

- 100% Compliant: We ensure all filings and documents are correct and as per GST laws—so no rejections or penalties.

- Always Available: Got a question? Our support team is here to help you anytime, even after the process is done.

What Our Clients Say

View AllKesha Ram

Register Karo is a company carryout all task which you demand from Registeration process to final compliance of commencement of the new company. My e... Read more

Dhamodaran Narayana...

Thank you for the exceptional support provided by Vishakha throughout this process. My experience with RegisterKaro's company wind-up service was exce... Read more

Jit

Register Karo is the best platform to register your company, @kajal chowhan helped me a lot, to make the process smoothly. Thank you team registerkaro

Guru

professional work, good team work by the team allocated to us, on time delivery for incorporation of my company, Ankit followed a good workflow throug... Read more

yayati

I reached out to registerkro for company windup. Would like to give shout out to Astha gupta who was extremly helpful throughout the process. Kudos to... Read more

Vijay Azad

Hi It was pleasure to contact you@alka for company registration .Happy with the dedication and support during process and working beyond timeline...

aravind raj

We did startup registeration with their team, it was point to point approach and they were clear in those procedures and their followup is too good...

vinay kumar

Your staff Ankita Matta is a polite person the way of handling the issues was good. I hope in future register karo team handle the issues in a same wa... Read more

Riya Singh

Register karo demonstrated professionalism and expertise in navigating complex legal and regulatory issues related to our industry. Special thanks Ank... Read more

ganesh patil

Had a great experience with Register Karo. The LLP registration process was handled smoothly and everything was explained clearly. Highly recommended!

Related Blogs

View All

How to Apply for GST Registration After Rejection in India

GST Notice Guide: Types, Reasons, Reply Format, and Penalties

GST for Advertising & Digital Marketing Services 2026 Guide

GST Registration for Export of Services in 2026: Conditions, LUT & Refund

GST for Consultancy Services in India 2026: Rates, SAC Codes & Compliance

How to Reply to GST Registration Notice 2026: REG-04, REG-18 & Format

GST for Software & IT Services in India 2026: Rate, SAC Codes & Exports

GST for Professional Services in India 2026: Limit, Rate & Process

GST for Freelancers in India 2026: Registration, Rates & RCM Guide

GST Compliance Calendar 2026-27: GST Return Due Dates, Forms & Deadlines