Income Tax Return Filing Online in India

Simplify your tax season with RegisterKaro’s expert-led income tax return filing services. We ensure accurate ITR e-filing, personalized assistance, and maximum deductions, keeping you compliant and penalty-free.

How to File Your Income Tax Return Online – Complete Video Guide

Want to file your income tax return but not sure how to start? Our video guide walks you through the complete ITR e-filing process, explains which documents you need, and highlights key deductions to help you reduce your tax liability.

Make your ITR filing fast, accurate, and stress-free.

Still have questions? Our experts are here to clarify the process and help you file.

Overview of Income Tax Return (ITR)

An Income Tax Return (ITR) is a mandatory annual declaration filed by individuals and businesses with the Income Tax Department of India. It details all income earned from various sources (like salary, business, property, capital gains, and other sources) during a specific financial year.

By submitting an ITR, taxpayers comply with legal requirements, establish proof of income for financial dealings, and facilitate the accurate assessment of their tax obligations to the government.

What is Income Tax Return (ITR) Filing?

Income Tax Return (ITR) filing is the annual process where individuals and entities report their earnings and claim deductions to the Income Tax Department of India. This declaration involves submitting a specific ITR form that details all income sources (like salary, business profits, or capital gains) and claims eligible tax-saving deductions, such as Section 80C for life insurance premiums, PPF, and EPF contributions, and Section 80D for health insurance premiums.

The ITR form that a taxpayer needs to file depends on the nature and complexity of their income. There are different forms (ITR-1, ITR-2, ITR-3, etc.), each tailored for specific types of income and taxpayers.

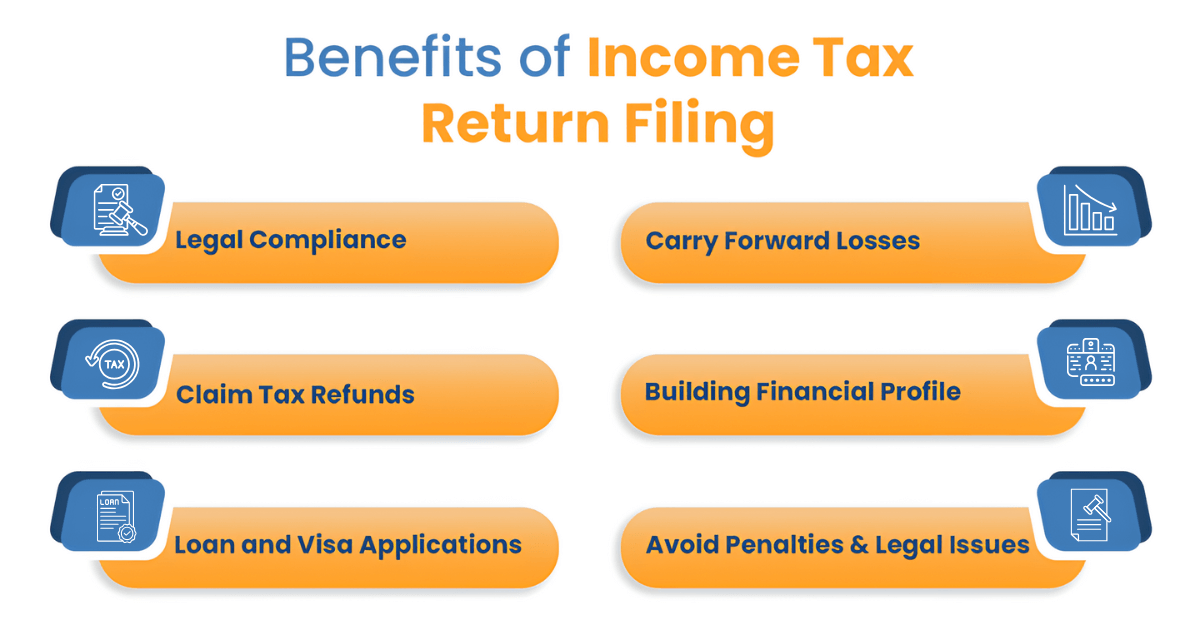

Why is Filing Your Income Tax Return Important?

Filing your income tax return offers significant benefits that go beyond just legal compliance. It helps you to:

- Avoid penalties: Failing to file or filing late can lead to significant penalties.

- Claim refunds: If you've paid excess tax (TDS), filing allows you to claim your income tax refund.

- Carry forward losses: Business losses can be carried forward to offset future income, reducing tax liability.

- Loan and Visa applications: ITR acknowledgments are often required for loan applications, visa processing, and other financial transactions.

- Proof of income: It serves as legitimate proof of your income for various purposes.

Assessment Year vs. Financial Year: Key Difference

In Income Tax Return (ITR) filing, understanding the distinction between the Financial Year (FY) and the Assessment Year (AY) is fundamental. While often confused, they represent different periods for income earning and tax assessment.

| Feature | Financial Year (FY) | Assessment Year (AY) |

| Definition | The year in which you earn your income. | The year in which the income earned in the Financial Year is assessed and taxed. |

| Period | Always starts on April 1st and ends on March 31st of the following calendar year. | Always starts on April 1st and ends on March 31st of the year succeeding the Financial Year. |

| Purpose | Period for income generation, expenses incurred, and financial transactions. | Period for filing Income Tax Returns (ITR), calculating tax liability, and paying taxes on the income earned in the preceding FY. |

| Examples | FY 2025-26: April 1, 2025, to March 31, 2026 (Income earned during this period). | AY 2026-27: April 1, 2026, to March 31, 2027 (ITR filed for income earned in FY 2025-26). |

| ITR Form | Income is earned during this period, but you don't file an ITR for the FY itself. | All Income Tax Return (ITR) forms explicitly ask for the Assessment Year, not the Financial Year, as you are assessing past income. |

| Relation | The Assessment Year is always the year immediately following the Financial Year. | The Financial Year is always the year immediately preceding the Assessment Year. |

Latest Income Tax Slabs and Rates

Understanding the applicable tax slabs is crucial for accurate income tax return filing. India offers two tax regimes:

New Tax Regime

The New Tax Regime (default from FY 2023-24) offers lower tax rates but fewer deductions and exemptions. For individuals, the tax slabs for FY 2025-26 (AY 2026-27) are:

| Income Slabs (Rs.) | Income Tax Rate (%) |

| 0 - 4,00,000 | Nil |

| 4,00,001 - 8,00,000 | 5 |

| 8,00,001 - 12,00,000 | 10 |

| 12,00,001 - 16,00,000 | 15 |

| 16,00,001 - 20,00,000 | 20 |

| 20,00,000 - 24,00,000 | 25% |

| Above 24,00,000 | 30% |

(₹12 Lakh rebate applicable under new regime for tax calculation)

Section 87A provides tax relief to resident individuals falling under lower income brackets by offering a rebate on tax payable. For FY 2025-26:

-

Under the new tax regime, a rebate of ₹25,000 is available for a total income up to ₹7 lakh.

-

Under the old tax regime, a rebate of ₹12,500 is available for a total income up to ₹5 lakh.

From FY 2025-26 (AY 2026-27) onwards, the rebate under the new tax regime has been significantly enhanced. A rebate of ₹60,000 is now available for resident individuals with total income up to ₹12 lakh, effectively making such income fully tax-free.

As a result, marginal relief, which earlier applied to income marginally exceeding ₹7 lakh, will now apply to income slightly above ₹12 lakh, ensuring taxpayers do not face a disproportionate tax burden for small income increases.

Further, salaried taxpayers under the new tax regime can claim a standard deduction of ₹75,000, making income up to ₹12.75 lakh effectively tax-free.

Old Tax Regime

The Old Tax Regime allows taxpayers to claim various deductions and exemptions (e.g., 80C, HRA, LTA). The slabs under the old regime depend on the taxpayer's age:

For Individuals below 60 years and HUF:

| Income Slabs (Rs.) | Income Tax Rate (%) |

| 0 - 2,50,000 | 0 |

| 2,50,001 - 5,00,000 | 5 |

| 5,00,001 - 10,00,000 | 20 |

| Above 10,00,000 | 30 |

For Senior Citizens (60 years to less than 80 years):

| Income Slabs (Rs.) | Income Tax Rate (%) |

| 0 - 3,00,000 | 0 |

| 3,00,001 - 5,00,000 | 5 |

| 5,00,001 - 10,00,000 | 20 |

| Above 10,00,000 | 30 |

For Super Senior Citizens (80 years and above):

| Income Slabs (Rs.) | Income Tax Rate (%) |

| 0 - 5,00,000 | 0 |

| 5,00,001 - 10,00,000 | 20 |

| Above 10,00,000 | 30 |

Example for New and Old Regimes

Let's illustrate with examples for FY 2025-26 (AY 2026-27):

Example Scenario: Mr. Sharma, aged 40, is a salaried employee with a gross annual salary of Rs. 15,00,000. He pays Rs. 2,00,000 in house rent annually and has made the following investments:

- PPF: Rs. 1,50,000 (eligible for Section 80C)

- Medical Insurance Premium: Rs. 25,000 (eligible for Section 80D)

- Interest on Housing Loan for Self-Occupied Property: Rs. 1,50,000 (eligible for Section 24(b))

- Old Tax Regime:

Under the Old Tax Regime, Mr. Sharma can claim various deductions and exemptions to reduce his taxable income.

Income Calculation (Old Regime):

- Gross Salary: Rs. 15,00,000

- Less: Standard Deduction (Sec 16): Rs. 50,000

- Less: HRA Exemption (as per rules): Let's assume an HRA exemption of Rs. 1,00,000 (calculated based on actual HRA received, rent paid, and salary components).

- Less: Interest on Housing Loan (Sec 24(b)): Rs. 1,50,000 (up to Rs. 2,00,000 for self-occupied)

- Less: Section 80C Deductions: Rs. 1,50,000 (for PPF, max allowed is Rs. 1.5 lakhs)

- Less: Section 80D Deductions: Rs. 25,000 (for medical insurance premium)

Taxable Income: 15,00,000 − 50,000 −1,00,000 − 1,50,000 − 1,50,000 − 25,000 = Rs.10,25,000

Tax Calculation (Old Regime - for individuals below 60 years for FY 2025-26):

- Up to Rs. 2,50,000: Nil

- Rs. 2,50,001 to Rs. 5,00,000: 5% of (5,00,000 - 2,50,000) = 5% of 2,50,000 = Rs. 12,500

- Rs. 5,00,001 to Rs. 10,00,000: 20% of (10,00,000 - 5,00,000) = 20% of 5,00,000 = Rs. 1,00,000

- Above Rs. 10,00,000 (i.e., Rs. 10,25,000 - 10,00,000 = Rs. 25,000): 30% of Rs. 25,000 = Rs. 7,500

Total Tax before Cess: 12,500 + 1,00,000 + 7,500 = Rs. 1,20,000

Add: 4% Health and Education Cess: 4% of 1,20,000 = Rs. 4,800

Total Tax Payable (Old Regime): 1,20,000 + 4,800 = Rs. 1,24,800

- New Tax Regime:

Under the New Tax Regime, Mr. Sharma cannot claim most of the common deductions and exemptions like HRA, Section 80C, Section 80D, or interest on a self-occupied housing loan. However, he benefits from lower tax slab rates and an enhanced standard deduction.

Income Calculation (New Regime):

- Gross Salary: Rs. 15,00,000

- Less: Standard Deduction (Sec 16): Rs. 75,000 (for FY 2024-25 onwards)

- Taxable Income: 15,00,000−75,000= Rs. 14,25,000

Tax Calculation (New Regime for FY 2025-26 / AY 2026-27):

- Up to Rs. 4,00,000: Nil

- Rs. 4,00,001 to Rs. 8,00,000: 5% of (8,00,000 - 4,00,000) = 5% of 4,00,000 = Rs. 20,000

- Rs. 8,00,001 to Rs. 12,00,000: 10% of (12,00,000 - 8,00,000) = 10% of 3,00,000 = Rs. 30,000

- Rs. 12,00,001 to Rs. 16,00,000: 15% of ₹14,25,000 -₹12,00,001 = 15% of ₹2,25,000 = Rs. ₹33,750

Total Tax before Cess: ₹20,000 + ₹40,000 + ₹33,750 = ₹93,750

Add: 4% Health and Education Cess: 4% of ₹93,750 = ₹3,750

Total Tax Payable (New Regime): ₹93,750 + ₹3,750 = ₹97,500

Conclusion for Mr. Sharma: Under the New Tax Regime, Mr. Sharma’s total tax liability comes to ₹97,500 for FY 2025-26 after claiming the standard deduction of ₹75,000.

This demonstrates how the optimal choice depends heavily on an individual's financial planning and the quantum of eligible deductions they can claim. Taxpayers must carefully evaluate both regimes based on their specific financial situation before filing their ITR.

Which Tax Regime Should You Choose?

The choice between the old and new tax regimes depends largely on the deductions and exemptions you plan to claim. If you have significant tax-saving investments and expenses, the old regime might be more beneficial. If you prefer simplicity and fewer deductions, the new regime could be better.

Connect with experts and make an informed decision for your income tax return filing.

Tax Rates for Different Entities (Individuals, HUF, Companies)

Tax rates vary based on the entity type. While individuals and HUFs follow the slab rates, companies have different tax structures. Domestic companies can opt for various concessional rates (e.g., 22% under Section 115BAA, 15% under Section 115BAB) based on certain conditions, or a standard rate of 25%/30% depending on turnover. Surcharge and cess are applicable in addition to the base tax rates.

Who Needs to e-File an ITR (Income Tax Return)?

Generally, any individual or entity whose gross total income exceeds the basic exemption limit is required to file an ITR. Refer to the tax slabs mentioned above for the specific exemption limits under both the Old and New Tax Regimes for FY 2025-26.

This includes:

- Salaried individuals

- Self-employed professionals and freelancers

- Businesses (companies, firms, LLPs)

- Individuals with income from house property, capital gains, or other sources.

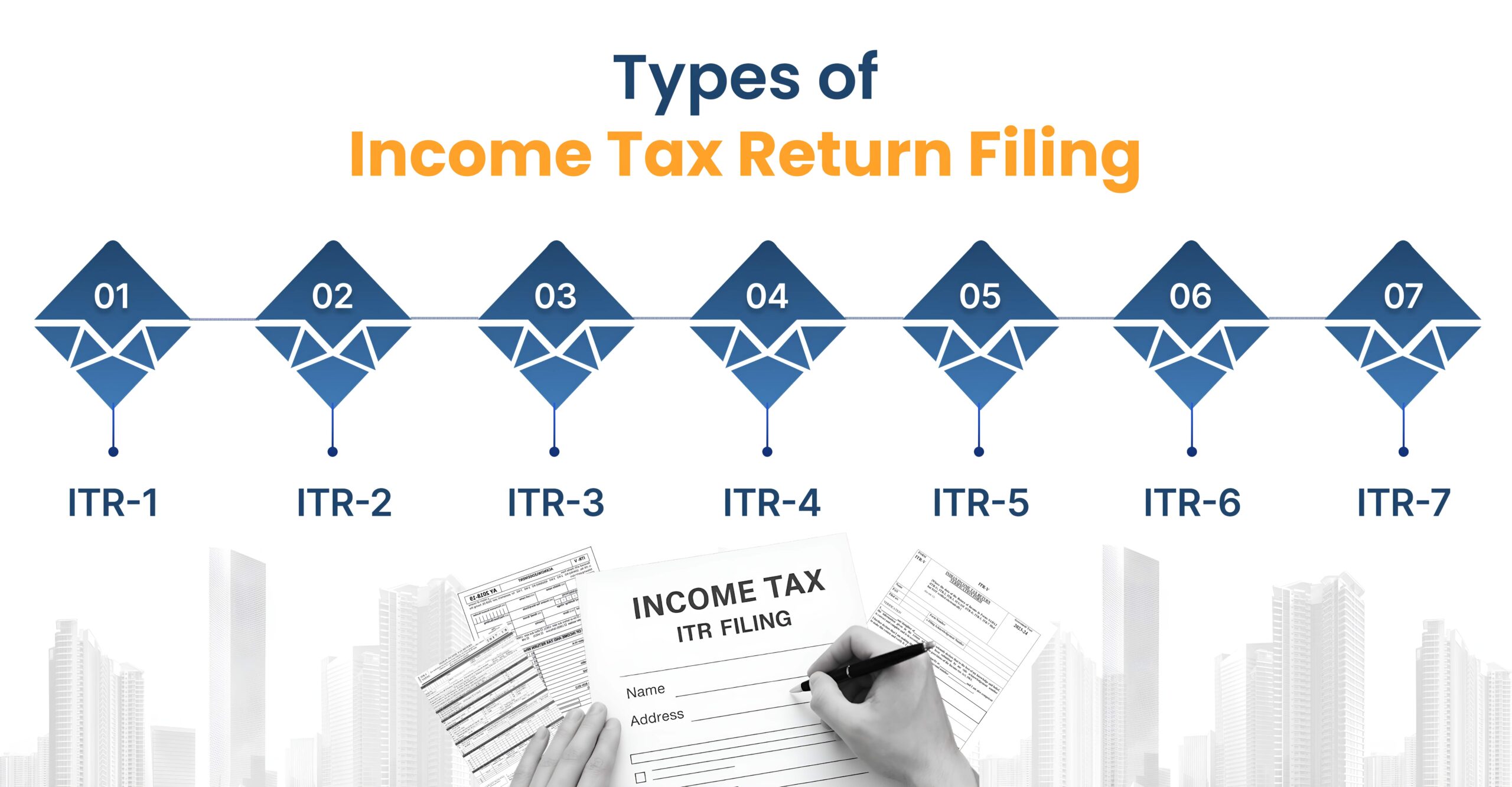

Different Income Tax Return Forms in India

Selecting the right ITR form is a critical step in how to file an income tax return. Choosing an incorrect form can lead to your return being treated as defective.

| Form Name | Applicable To | Types of Income Covered | Exclusions |

| ITR-1 (SAHAJ) | Salaried Individuals, Pensioners, and Residents (Income ≤ Rs. 50 lakh). | Salary or Pension Income, Income from one house property (excluding losses brought forward), Income from other sources (e.g., savings account interest), Agricultural income up to Rs. 5,000. | Capital gains, Business or professional income, Foreign assets. |

| ITR-2 | Individuals and Hindu Undivided Families (HUFs) with income other than business or profession. | Salary or Pension Income, Income from more than one house property, Capital gains (short-term/long-term, including Section 112A), Income from other sources (e.g., lottery, foreign dividends), Income from foreign assets. | Income from profits and gains of business or profession. |

| ITR-3 | Individuals and HUFs with business income. | Income from proprietorship business, Professional income (e.g., doctors, lawyers), Income from partnership firm, Salary, house property, capital gains, and other sources. | None (Comprehensive form for all income streams, including business income). |

| ITR-4 (SUGAM) | Small Businesses and Professionals under Presumptive Taxation Schemes. | Resident individuals, HUFs, and firms (excluding LLPs), Income under Section 44AD, 44ADA, or 44AE (presumptive taxation schemes). | Income exceeding Rs. 50 lakh, Detailed accounting requirements (as income is presumed). |

| ITR-5 | Firms, LLPs, AOPs, BOIs, AJPs, Co-operative Societies, and Local Authorities. | Applicable to entities like firms, LLPs, co-operative societies, etc. | Not applicable for individuals, HUFs, or companies claiming exemptions under Section 11 of the Act. |

| ITR-6 | Companies (excluding those claiming exemption under Section 11). | Companies. | Companies claiming exemptions under Section 11 (e.g., income from property held for charitable purposes). |

| ITR-7 | Persons (including companies) required to file under specific sections of the Income Tax Act. | Charitable or religious trusts (Section 139(4A)), Political parties (Section 139(4B)), Scientific research institutions, universities (Section 139(4C)), Educational institutions (Section 139(4D)). | None (Specific to entities required under the sections mentioned). |

2026 Update: For AY 2025-26 / FY 2024-25, new Excel utilities for ITR-1 and ITR-4 were released by the Income Tax Department. Additionally, schema changes have occurred in ITR-1, ITR-2, and ITR-5 formats, which affect field names and schedules. So taxpayers should always use the latest forms from the e-filing portal.

Documents Required for Income Tax Return E-Filing

Having these documents ready will significantly speed up your income tax return filing process.

- Your PAN Card and Aadhaar Card: Your PAN card is a unique tax ID, essential for all financial transactions and e-filing of income tax returns. Your Aadhaar card is now mandatory to link with PAN for tax filing, ensuring streamlined verification. Both are fundamental for accurate submissions.

- Form 16 from Your Employer: For salaried individuals, Form 16 is crucial for income tax return filing. Issued by your employer, it details TDS (Tax Deducted at Source) from your salary and provides a breakup of salary components and declared deductions (Part A & B). If you changed jobs, get one from each employer.

- Bank Statements and Interest Certificates: These are vital for accurate income tax return filing. They help report all interest income from savings accounts, FDs, and RDs, even if eligible for deduction. They also assist in identifying high-value transactions and reconciling tax refunds.

- Proof of Investments for Deductions (80C, 80D, etc.): To claim tax deductions, you need proof of investments and expenditures. For Section 80C, gather receipts for PPF, ELSS, life insurance, home loan principal, and children's tuition fees. For Section 80D, keep health insurance premium receipts. These documents reduce your taxable income.

- Form 26AS: Your Annual Tax Statement Form 26AS is an indispensable annual tax statement for income tax return filing. It shows all TDS/TCS, advance tax, self-assessment tax paid, and refunds received linked to your PAN. Reconciling it with your records ensures accuracy. It's now complemented by the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) for a comprehensive financial view.

How to File Income Tax Return Online in India?

Our streamlined income tax return filing process ensures that you can complete your tax obligations with ease.

Step 1: Gathering All Necessary Documents

The foundation of accurate income tax return filing lies in having all your financial documents meticulously organized. Before you even begin the e-filing process, ensure you have gathered all relevant paperwork. This typically includes:

- PAN card and Aadhaar card (mandatory for linking)

- Form 16 (for salaried individuals from each employer)

- Form 16A/16B/16C (for TDS on income other than salary, property sale, or rent, respectively)

- Bank statements (for interest income, significant transactions)

- Interest certificates from banks/financial institutions

- Investment proofs (e.g., PPF, ELSS, life insurance premium receipts under Section 80C)

- Health insurance premium receipts (for Section 80D)

- Home loan statements (for interest and principal repayment)

- Form 26AS (to verify TDS/TCS as per the Income Tax Department's records).

Having these readily available will significantly streamline the data entry and verification process.

Step 2: Calculating Your Total Taxable Income

Once your documents are in order, compute your total taxable income. This involves consolidating income from all five major heads as per the Income Tax Act:

- Income from Salary/Pension: This includes your basic salary, allowances, perquisites, and any pension received, after accounting for standard deduction and professional tax.

- Income from House Property: This covers rental income from let-out properties or the deemed rental value for self-occupied properties (though typically considered nil for one self-occupied house), after deducting municipal taxes and standard deduction (30% of Net Annual Value) and interest on home loans.

- Income from Business or Profession: For self-employed individuals and businesses, this involves calculating profits after deducting eligible business expenses from gross receipts/turnover.

- Income from Capital Gains: This includes profits or losses from the sale of capital assets like shares, mutual funds, property, gold, etc., categorized as short-term or long-term.

- Income from Other Sources: This is a residual category covering income like interest from savings accounts and fixed deposits, family pension, winnings from lotteries, gambling, etc.

Our process helps you systematically account for each income stream to arrive at your Gross Total Income before any deductions.

Step 3: Claiming All Available Deductions

After calculating your Gross Total Income, claim all applicable deductions under various sections of the Income Tax Act. This is where significant tax savings can be achieved. Our guidance ensures you do not miss out on any eligible deductions, such as:

- Section 80C: For investments in instruments like PPF, EPF, ELSS, NSC, life insurance premiums, home loan principal repayment, and tuition fees (up to Rs. 1.5 lakh).

- Section 80D: For health insurance premiums paid for self, family, and parents.

- Section 80E: For interest paid on education loans.

- Section 80G: For donations made to eligible charitable institutions.

- Section 80TTA/80TTB: For interest earned on savings accounts (up to Rs. 10,000 for individuals/HUF, or Rs. 50,000 for senior citizens).

- Section 24(b): For interest paid on home loans. By accurately claiming these, your total taxable income is reduced, leading to a lower tax liability.

Step 4: Uploading Details to the Income Tax Portal

With all your income, deductions, and tax computations finalized, prepare and upload your ITR. This involves entering all the compiled information into the chosen ITR form (ITR-1, ITR-2, etc.) on the official Income Tax e-filing portal.

Many details, such as personal information and TDS/TCS data from Form 26AS and Annual Information Statement (AIS), are often pre-filled, which should be carefully verified. We assist in ensuring all fields are accurately populated, any balance tax payable is paid (self-assessment tax), and the return is generated in the correct format (usually JSON) for seamless upload to the portal.

Step 5: E-Verifying Your Filed ITR

The submission of your ITR is incomplete until it is e-verified. E-verification is a mandatory final step that validates your e-filing of the income tax return and signifies your authentication of the data submitted. Without successful e-verification, your ITR will not be processed by the Income Tax Department and will be treated as if it were never filed.

We guide you through the various convenient methods available for e-verification:

- Aadhaar OTP: A One-Time Password sent to your mobile number registered with Aadhaar.

- Net Banking: Verification through your bank's net banking portal.

- EVC (Electronic Verification Code) through Pre-validated Bank Account/Demat Account: An EVC is generated and sent to your mobile/email linked with a pre-validated bank or demat account.

- EVC through Bank ATM (Offline Method): For certain banks, an EVC can be generated via an ATM.

- Digital Signature Certificate (DSC): DSC is primarily used by businesses and professionals for digital signing. Choosing any of these methods ensures that your income tax return filing is formally accepted by the Income Tax Department.

Income Tax Return Filing Fees, Due Dates & Penalties

Tax compliance is crucial, and understanding the deadlines and consequences of late filing is key to a smooth income tax return filing experience.

Income Tax Return Filing Charges

The charges for ITR (Income Tax Return) filing in India vary significantly based on how you choose to file and the complexity of your income. Here's a breakdown:

1. Free Filing (via Government Portal):

- The Income Tax Department's official e-filing portal (incometax.gov.in) allows you to file your ITR completely free of cost.

- This is the most economical option, especially for individuals with straightforward income sources (like salary and interest) who are comfortable navigating the portal themselves.

- The portal provides pre-filled data (from Form 26AS, AIS, TIS), which simplifies the process for many taxpayers.

2. Online Tax Filing Platforms (Self-Service):

- Several private online platforms offer user-friendly interfaces to simplify ITR filing.

- Many offer a "do-it-yourself" (DIY) or self-service option, which is relatively inexpensive.

- Charges typically range from Rs. 99 to Rs. 800+, depending on the platform and the complexity of your income (e.g., simple salary vs. capital gains, multiple house properties).

- Some platforms might offer free filing for very basic income profiles (e.g., income up to Rs. 1 lakh or for unemployed individuals, students, widows, and retired individuals with only family pension).

- These platforms often provide features like auto-importing data, tax calculations, and easy e-verification.

3. Online Tax Filing Platforms (Expert/CA-Assisted):

- For those who prefer professional help without visiting a physical office, these platforms also offer expert-assisted or CA-assisted services.

- The charges for these services are higher as they involve a tax professional (Chartered Accountant or tax expert) reviewing and filing your return.

- Prices vary widely based on income complexity:

- Simple salaried cases: Can start from around Rs. 800 to Rs. 1,500.

- Form 16s, house property income, or basic business/professional income: May cost Rs. 1,500 to Rs. 3,000+.

- Capital gains (shares, mutual funds, property), F&O trading, cryptocurrency, foreign income, or business income requiring balance sheets/audits: Charges can range from Rs. 3,000 to Rs. 15,000 or more, depending on the volume of transactions and complexity.

- NRI filing with Indian income or resident with foreign income: Often priced higher, starting from Rs. 2,000 and going up to Rs. 10,000+.

- These services usually include tax planning advice, query resolution, and sometimes notice assistance.

4. Chartered Accountants (CAs) / Tax Consultants:

- Hiring a local CA or tax consultant provides personalized service and in-depth advice.

- Their charges are generally higher than online platforms due to the direct human interaction, personalized attention, and often a broader range of services (e.g., detailed tax planning, representation for notices, business advisory).

- Fees typically range from Rs. 1,500 to Rs. 5,000 for basic individual filings.

- For complex cases, high-value transactions, business audits, or specific advisory needs, the fees can easily go into tens of thousands of rupees.

5. Factors Influencing ITR Filing Charges:

- Source of Income: Salary, house property, capital gains, business/profession, foreign income, cryptocurrency, etc., all impact complexity.

- Number of Income Sources: More sources generally mean higher charges.

- Number of Transactions: High volume of stock trades or capital gains transactions can increase fees.

- Type of ITR Form: ITR-1 is the simplest and cheapest to file, while ITR-3, ITR-5, ITR-6, and ITR-7 (for businesses, trusts, etc.) are more complex and costly.

- Assistance Level: Self-filing is free, online automated assistance is low-cost, and expert/CA assistance is higher.

- Additional Services: Tax planning, notice handling, audit assistance, financial advisory, etc., incur extra charges.

What is the Last Date to File Your ITR?

For Financial Year 2025-26 (Assessment Year 2026-27), the due dates for filing Income Tax Returns are as follows:

- For individuals and non-audit cases: The original due date, usually July 31st, has been extended by the Central Board of Direct Taxes (CBDT) to September 15, 2025. This applies to salaried individuals, individuals with income from house property, other sources, etc., who are not required to get their accounts audited. This extension provides taxpayers with more time due to significant changes in ITR forms and system readiness.

- For audit cases: The due date for individuals and entities (excluding companies) whose accounts are required to be audited is generally October 31, 2025. This category includes businesses and professionals exceeding certain turnover limits.

- For taxpayers requiring a report under Section 92E (transfer pricing): The due date is typically November 30, 2025.

Penalty for Late Filing of ITR

If you miss the original due date for income tax return filing, Section 234F of the Income Tax Act imposes a mandatory late filing fee.

This penalty for late filing of the income tax return is designed to encourage timely compliance:

- For ITRs filed on or before December 31st of the Assessment Year:

-

- If your total income is up to Rs. 5 lakh, the penalty is Rs. 1,000.

- If your total income exceeds Rs. 5 lakh, the penalty is Rs. 5,000.

- For ITRs filed after December 31st of the Assessment Year (and up to March 31st of the next financial year, if an updated return is applicable):

-

- If your total income exceeds Rs. 5 lakh, the penalty increases to Rs. 10,000.

- However, the penalty remains Rs. 1,000 if your total income is up to Rs. 5 lakh.

- No penalty is applicable if your total income does not exceed the basic exemption limit (e.g., Rs. 3 lakh for individuals under the new regime for FY 2025-26, or Rs. 2.5 lakh for those under the old regime below 60 years).

Interest Payable on Delayed Tax Payment

Beyond the late filing fee, significant interest charges can apply if there is any unpaid tax liability. These are levied under different sections of the Income Tax Act:

- Section 234A (Interest for default in furnishing return of income): If you have any outstanding tax liability and you file your ITR after the due date, interest is charged at 1% per month or part thereof on the unpaid tax amount. This interest is calculated from the original due date of filing until the actual date you file your return. The longer the delay, the higher the interest.

- Section 234B (Interest for default in payment of advance tax): If you are liable to pay advance tax (i.e., your estimated tax liability after TDS is Rs. 10,000 or more in a financial year) but fail to pay at least 90% of your total tax payable as advance tax by March 31st of the financial year, interest is charged under this section. It's levied at 1% per month or part thereof on the shortfall, calculated from April 1st of the assessment year until the date you pay the tax.

- Section 234C (Interest for deferment of advance tax): This interest is charged if you do not pay your advance tax installments on time or if the installments paid are less than the prescribed percentages by the respective due dates (June 15th, September 15th, December 15th, and March 15th). Interest is generally charged at 1% per month or part thereof for the period of default for each installment.

What Happens if You Miss the ITR Filing Deadline?

Missing the deadline for income tax return filing has several significant consequences beyond just monetary penalties and interest:

- Filing a Belated Return: If you miss the main deadline (September 15, 2025, for non-audit cases), you can still file a "belated return" under Section 139(4) of the Income Tax Act. The last date to file a belated return for FY 2025-26 (AY 2026-27) is December 31, 2025, subject to the applicable late filing fees under Section 234F.

- Loss of Benefits for Carrying Forward Losses: A major disadvantage of late filing is the forfeiture of the right to carry forward certain losses. Losses from business/profession (except house property) or capital gains cannot be carried forward if the original or belated return is not filed by the due date. This can result in a higher tax liability in future years.

- Delayed Tax Refunds: If you are eligible for a tax refund from the Income Tax Department, filing your ITR late will inevitably delay the processing and receipt of your refund. Interest on refund is only granted from April 1st of the assessment year if the return is filed by the due date.

- Inability to Opt for Old Tax Regime: For FY 2025-26 onwards, the New Tax Regime is the default regime. If you wish to opt for the Old Tax Regime to claim various deductions and exemptions (like 80C, 80D, HRA exemption), you typically need to file your original ITR by the due date. Missing this deadline might restrict your ability to choose the Old Tax Regime for that assessment year.

- Increased Scrutiny and Notices: Late filing or non-filing can flag your PAN for increased scrutiny by the Income Tax Department, potentially leading to notices for non-compliance or a call for detailed explanations.

- Difficulty in Loan/Visa Applications: Many financial institutions and foreign embassies require ITR copies for loan applications, visa processing, or proving your financial standing. Missing your income tax return filing can create significant hurdles in such situations.

- Prosecution: In severe cases of persistent non-filing, especially if there's a substantial tax liability, the Income Tax Department can initiate prosecution proceedings, which may lead to imprisonment.

Therefore, it is always advisable to file your income tax return by the stipulated due date to avoid penalties, interest, and other adverse consequences.

How to Save More on Taxes with Smart Deductions?

Understanding and claiming available deductions is a key benefit of filing an income tax return.

1. Popular Deductions under Section 80C

Section 80C is one of the most widely utilized sections for tax saving, allowing a maximum deduction of Rs. 1.5 lakh from your gross total income. This deduction can be claimed by individuals and Hindu Undivided Families (HUFs) for investments made in various specified instruments and certain expenditures.

Key eligible investments and expenses include:

- Public Provident Fund (PPF): Long-term savings cum tax-saving scheme.

- Employees' Provident Fund (EPF): Mandatory contribution from salaried individuals.

- Equity Linked Savings Schemes (ELSS): Tax-saving mutual funds with a lock-in period of 3 years.

- National Savings Certificates (NSC): Government-backed small savings scheme.

- Life Insurance Premiums: Premiums paid for life insurance policies for self, spouse, or dependent children.

- Home Loan Principal Repayment: The principal portion of your EMI towards a housing loan.

- Tuition Fees: Fees paid for the full-time education of up to two children.

- Sukanya Samriddhi Yojana (SSY): Savings scheme for a girl child.

- Senior Citizen Savings Scheme (SCSS): Savings scheme for senior citizens.

- Fixed Deposits (Tax Saving FDs): Specific 5-year lock-in FDs. Leveraging this section effectively is a cornerstone of smart income tax return filing for many taxpayers.

2. Health Insurance Premium Benefits under Section 80D

Section 80D allows deductions for health insurance premiums paid, promoting healthcare savings. This deduction is available to individuals and HUFs. The limits vary based on who is covered:

- For self, spouse, and dependent children: A deduction of up to Rs. 25,000 can be claimed.

- For parents (who are not senior citizens): An additional deduction of up to Rs. 25,000 is available.

- For parents (who are senior citizens - 60 years or above): The deduction limit increases to Rs. 50,000.

- For self and/or spouse who are senior citizens: The deduction for self/spouse/dependent children also increases to Rs. 50,000. This means, if you are below 60 and pay premiums for yourself, spouse, and dependent children (Rs. 25,000), and also for your senior citizen parents (Rs. 50,000), you can claim a total deduction of Rs. 75,000.

Additionally, a deduction of up to Rs. 5,000 for preventive health check-ups is also allowed within these limits, payable in cash. This section is a significant tool for lowering your taxable income during income tax return filing.

3. Deductions on Home Loan Interest

Interest paid on a home loan can provide substantial tax benefits. This deduction is available under Section 24(b) of the Income Tax Act. The amount you can claim depends on whether the property is self-occupied or let out:

- For Self-Occupied Property: You can claim a maximum deduction of up to Rs. 2 lakh on the interest paid towards a home loan for a self-occupied property. This applies to the interest accrued for the financial year.

- For Let-Out Property (Rented Out): There is no upper limit on the interest deduction for a let-out property. You can claim the entire interest paid as a deduction. However, the total loss from house property that can be set off against other income in a financial year is restricted to Rs. 2 lakh.

Any unadjusted loss can be carried forward for 8 subsequent assessment years. This deduction is a major component for individuals having a housing loan, significantly impacting their income tax return filing.

4. Understanding Standard Deduction for Salaried Employees

The Standard Deduction is a fixed deduction allowed to all salaried individuals from their gross salary income. For Financial Year 2025-26 (Assessment Year 2026-27), the standard deduction for salaried employees is Rs. 50,000. This deduction is available irrespective of whether you opt for the Old Tax Regime or the New Tax Regime.

It was reintroduced in Budget 2018, replacing the earlier deductions for transport allowance and medical reimbursement. It simplifies income tax return filing for salaried individuals by providing a standard deduction without the need to submit proofs for specific expenses.

From FY 2024-25 onwards, the standard deduction has been increased to ₹75,000 for salaried taxpayers under the new tax regime, as confirmed by the Finance Act, 2024. This deduction continues to apply for FY 2025-26 (Assessment Year 2026-27), helping reduce taxable income without any additional compliance.

5. Other Key Deductions to Lower Your Taxable Income

Beyond the popular sections mentioned above, several other deductions can further reduce your taxable income during income tax return filing:

- Section 80G (Donations): Allows deduction for donations made to certain approved charitable institutions and funds. The deduction amount varies (50% or 100%) and can be subject to certain limits based on the recipient institution.

- Section 80TTA/80TTB (Interest on Savings/FD for Senior Citizens): Section 80TTA allows a deduction of up to Rs. 10,000 for interest earned on savings accounts for individuals and HUFs (other than senior citizens). For senior citizens (60 years or above), Section 80TTB allows a higher deduction of up to Rs. 50,000 on interest income from savings accounts, fixed deposits, and recurring deposits.

- Section 80E (Education Loan Interest): You can claim a deduction for the entire interest paid on an education loan taken for your higher education, or for that of your spouse, children, or a student for whom you are the legal guardian. There is no upper limit on the amount of interest that can be claimed, and the deduction is available for a maximum of 8 years or until the interest is fully repaid, whichever is earlier.

- Section 80EE/80EEA (Additional Home Loan Interest): These sections provide additional deductions on home loan interest for first-time homebuyers, over and above the Rs. 2 lakh limit under Section 24(b), subject to certain conditions and loan/property value limits. These were introduced to boost affordable housing. Exploring all these avenues is essential for comprehensive tax planning and maximizing your overall tax savings.

Common Mistakes While Filing ITR

Filing your Income Tax Return (ITR) can seem daunting, and even small errors can lead to notices from the Income Tax Department, penalties, or delayed refunds. Here are some of the most common mistakes taxpayers make while filing their ITR:

1. Missing the Filing Deadline:

- Mistake: Not filing the ITR by the stipulated due date (e.g., July 31st for most individuals for the current Assessment Year).

- Consequence: Late filing fees (under Section 234F), interest on unpaid tax (under Section 234A), and inability to carry forward certain losses (like capital losses or business losses) to future years.

2. Choosing the Wrong ITR Form:

- Mistake: Selecting an ITR form (ITR-1, ITR-2, ITR-3, etc.) that doesn't match your income sources and taxpayer category.

- Consequence: The return may be deemed "defective" or even invalid, leading to processing delays, notices, and a requirement to refile, which can be cumbersome.

3. Not Reporting All Sources of Income:

- Mistake: Omitting income from certain sources, often inadvertently. This includes interest from savings accounts, fixed deposits, recurring deposits, dividends, capital gains (from stocks, mutual funds, property), rental income, freelance income, or even interest on income tax refunds.

- Consequence: Under-reporting of income can lead to severe penalties (50% to 200% of the tax due on the undeclared income), additional interest charges, and potential legal proceedings. Remember, the Income Tax Department receives information about almost all your financial transactions.

4. Mismatch between ITR and Form 26AS/AIS/TIS:

- Mistake: Not reconciling the income and TDS details in your ITR with the information available in your Form 26AS, Annual Information Statement (AIS), and Taxpayer Information Summary (TIS).

- Consequence: Discrepancies can trigger notices from the Income Tax Department, as these documents are crucial for cross-verification. Ensure that all TDS deducted reflects in your ITR and matches these statements.

5. Failure to E-Verify the ITR:

- Mistake: Submitting the ITR but forgetting to complete the e-verification process within the stipulated time limit (usually 30 days from filing).

- Consequence: An unverified ITR is considered invalid, meaning it's as good as not filed. This can lead to all the penalties associated with non-filing.

6. Providing Incorrect Personal or Bank Details:

- Mistake: Errors in PAN, Aadhaar number, name, address, email ID, mobile number, or bank account details (especially IFSC code and account number).

- Consequence: Incorrect personal details can lead to notices being sent to the wrong address, communication issues, delays in processing refunds, or even failure to receive them. The Income Tax Department credits refunds directly to the validated bank account provided.

7. Incorrectly Claiming Deductions/Exemptions:

- Mistake: Claiming deductions you are not eligible for, overstating deductions, or failing to keep proper proofs for claimed deductions (e.g., fake rent receipts for HRA, inflating Section 80C investments).

- Consequence: If scrutinized, invalid or inflated claims can lead to penalties (up to 200% of the tax under-reported), interest, and legal action. Also, forgetting to claim eligible deductions (like certain medical expenses, education loan interest, etc.) means paying more tax than necessary.

8. Errors in Residential Status:

- Mistake: Incorrectly determining your residential status (Resident, Non-Resident, or Resident But Not Ordinarily Resident).

- Consequence: This can significantly impact your tax liability, especially if you have foreign income or assets, leading to under-reporting of global income for residents or incorrect tax applicability for NRIs.

How to Check the ITR E-Filing Status?

Checking your Income Tax Return (ITR) e-filing status is crucial to ensure your return has been processed correctly and to track any potential refund. Here's how to do it:

Method 1: Via the Income Tax e-filing Portal (Recommended)

- Log In: Go to the official Income Tax Department's e-filing portal (incometax.gov.in) and log in using your User ID (PAN/Aadhaar), password, and date of birth.

- Navigate to View Returns: Once logged in, click on "e-File" from the top menu, then select "Income Tax Returns," and then "View Filed Returns."

- Select Assessment Year: Choose the relevant Assessment Year for which you want to check the ITR status from the dropdown menu.

- View Details: A list of all your filed ITRs for that Assessment Year will appear. Click on "View Details" next to the specific ITR you want to check.

- Check Status: The screen will display the current status of your ITR (e.g., "Submitted and pending for e-verification," "Successfully e-verified," "Under Processing," "Processed," "Defective," "Case transferred to Assessing Officer"). You can also see the "Lifecycle of ITR" for a detailed timeline.

Method 2: Without Login (using Acknowledgement Number and PAN)

- Visit Portal: Go to the Income Tax Department's e-filing portal (incometax.gov.in).

- Find "ITR Status": On the homepage, look for a "Quick Links" section. There might be a direct link for "ITR Status" or "Know Your ITR Status." (Note: As of recent updates, the pre-login option for ITR status might be redirected to a post-login process for enhanced security, so Method 1 is generally more reliable.)

- Enter Details: If available, you would typically enter your PAN and the ITR Acknowledgement Number (a 15-digit number found on your ITR-V acknowledgment form).

- Validate Mobile Number: Enter your registered mobile number and click "Continue." You will receive an OTP.

- Enter OTP: Enter the OTP received on your mobile number to view the status.

What to Expect After Filing Your Income Tax Return

Finalizing your income tax return filing journey involves a critical step: verification. This section elaborates on the importance of this final action, various methods for its completion, how to monitor your refund, and how to effectively respond to any notices from the Income Tax Department.

1. The Importance of E-Verifying Your Return

E-verification is the digital confirmation that the Income Tax Return (ITR) you have filed is indeed genuine and submitted by you. It is a mandatory step to complete the e-filing of the income tax return process. Without successful e-verification within the stipulated time limit (currently 30 days from the date of filing for returns filed on or after August 1, 2022), your ITR will be considered invalid, meaning it will be treated as if you never filed it.

Consequently, the Income Tax Department will not process your return, and any tax refund due to you will not be issued. E-verification ensures the authenticity and integrity of your tax submission, crucial for the department to initiate processing under Section 143(1) of the Income Tax Act.

2. How to E-Verify Your ITR: Different Methods Explained

The Income Tax Department offers multiple convenient methods for e-verifying your ITR, allowing taxpayers to choose the option that best suits them. This ensures a hassle-free completion of your income tax return filing:

- Aadhaar OTP: This is one of the most popular and easiest methods. An OTP (One-Time Password) is sent to the mobile number registered with your Aadhaar. Ensure your PAN is linked to your Aadhaar, and your mobile number is updated with UIDAI.

- Net Banking: Many banks offer a direct e-verification service through their net banking portals. After logging into your bank account, you can find an option (often under "Tax" or "e-Verify") to directly e-verify your ITR. Your PAN must be linked to your bank account for this method to work.

- EVC (Electronic Verification Code) through a pre-validated Bank Account: An EVC is a 10-digit alphanumeric code generated by the Income Tax Department. If you have a pre-validated and EVC-enabled bank account on the e-filing portal, the EVC will be sent to the mobile number and email ID registered with that account. You then enter this EVC on the e-filing portal to complete verification.

- ATM (Offline Method): Some banks allow the generation of an EVC through their ATMs. You can visit a participating bank's ATM, swipe your card, enter your PIN, and select the option to generate EVC for income tax filing. The EVC will be sent to your mobile number and email ID registered with the e-filing portal.

- Digital Signature Certificate (DSC): This method is generally used by businesses, professionals, and individuals whose accounts are subject to audit. A valid and active DSC can be used to digitally sign and verify the ITR directly while uploading it.

3. Tracking the Status of Your Income Tax Refund

If you are expecting a tax refund after your income tax return filing, you can easily track its status online. This allows you to monitor the progress of your refund and take necessary action if there are delays. You can typically check your refund status through two primary platforms:

i) Income Tax e-filing Portal (incometax.gov.in):

- Log in to your e-filing account.

- Navigate to "e-File" > "Income Tax Returns" > "View Filed Returns".

- Click on the relevant assessment year and then "View Details" to see the status of your ITR, including refund status.

ii) NSDL (Protean eGov Technologies Limited) Website (tin.tin.nsdl.com):

- Visit the NSDL refund status page.

- Enter your PAN and the relevant Assessment Year.

- Enter the captcha code and click "Proceed."

- The page will display your refund status, indicating whether it's processed, sent, failed, or rejected. Common refund statuses include "Refund Processed," "Refund Sent," "Refund Failed" (often due to incorrect bank details), or "Refund Rejected." Ensure your bank account details are pre-validated on the e-filing portal to receive direct credit via RTGS/NEFT.

4. Responding to an Income Tax Notice

Receiving an income tax notice can be unsettling, but it's a common occurrence for various reasons, such as discrepancies found in your filed return, requests for additional information, or selection for scrutiny. When you receive a notice related to your income tax return filing:

- Understand the Notice: The first and most crucial step is to carefully read and understand the reason behind the notice. Notices can be issued under various sections (e.g., Section 139(9) for defective returns, Section 143(2) for scrutiny, Section 148 for income escaping assessment, or Section 156 for demand of tax).

- Note the Deadline: Every notice comes with a specific deadline for response. Failing to respond within this timeframe can lead to penalties or adverse actions from the department.

- Gather Relevant Documents: Collect all documents and information requested in the notice, as well as any supporting documents that can clarify your position or rectify discrepancies.

- Prepare a Comprehensive Response: Your response should be clear, concise, and address each point raised in the notice. If there's a discrepancy, explain the reason and provide supporting evidence. For defective returns, you might need to file a revised or corrected return.

- Online Submission: Most responses to income tax notices can now be filed online through the Income Tax e-filing portal under the "e-Proceedings" section. This ensures a documented and timely submission.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

Can I file my ITR without Form 16?

−Yes, you can certainly file your Income Tax Return even without Form 16. While Form 16 from your employer simplifies the process by providing consolidated salary and TDS details, it's not strictly mandatory. You can gather the necessary information from your monthly payslips, which detail your salary components, allowances, and any TDS deducted.

What should I do if I have made a mistake in my ITR?

+Is it mandatory to file ITR for a NIL return?

+How do I know which ITR form is right for me?

+How can Registerkaro make my tax filing process easier?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose Registerkaro for Your Income Tax Filing?

When it comes to your income tax return filing, choose a partner who offers expertise, convenience, and peace of mind.

- Our Team of Experienced Tax Professionals: Our dedicated team of Chartered Accountants and tax experts possesses in-depth knowledge of Indian tax laws, ensuring accurate and compliant e-filing of income tax returns.

- A Simplified and Secure Online Filing Process: Our user-friendly online platform simplifies the entire filing process. We also prioritize your data's security with robust encryption and strict privacy measures.

- Get Expert Advice on Tax Planning and Savings: Beyond mere filing, we offer strategic tax planning advice to help you maximize deductions, optimize your tax structure, and achieve significant benefits of filing an income tax return through legitimate tax savings. Our competitive income tax return filing charges ensure value for money.

- Dedicated Support for All Your Tax-Related Queries: We provide prompt and personalized support to address all your questions and concerns throughout the income tax return filing process. Your satisfaction is our priority.

What Our Clients Say

View AllJit

Register Karo is the best platform to register your company, @kajal chowhan helped me a lot, to make the process smoothly. Thank you team registerkaro

Guru

professional work, good team work by the team allocated to us, on time delivery for incorporation of my company, Ankit followed a good workflow throug... Read more

yayati

I reached out to registerkro for company windup. Would like to give shout out to Astha gupta who was extremly helpful throughout the process. Kudos to... Read more

Vijay Azad

Hi It was pleasure to contact you@alka for company registration .Happy with the dedication and support during process and working beyond timeline...

aravind raj

We did startup registeration with their team, it was point to point approach and they were clear in those procedures and their followup is too good...

vinay kumar

Your staff Ankita Matta is a polite person the way of handling the issues was good. I hope in future register karo team handle the issues in a same wa... Read more

Riya Singh

Register karo demonstrated professionalism and expertise in navigating complex legal and regulatory issues related to our industry. Special thanks Ank... Read more

ganesh patil

Had a great experience with Register Karo. The LLP registration process was handled smoothly and everything was explained clearly. Highly recommended!

Ayush

Really impressed with the service provided by Prayansh Jindal. He handled everything efficiently and ensured that all my queries were answered promptl... Read more

Amit Kumar

Ms Vandana Sharma has done awesome work for me from Registerkaro . She worked late night with me . I appreciate her for these type of effort . Thanks... Read more

Related Blogs

View All

RTGS Timings in India: Latest Transfer Time, Limits & Rules

Old vs New Tax Regime in India: Comparison for FY 2026-27

Income Tax Refund Delay: Reasons, Status & Faster Refund Tips

ITR Processing Time for AY 2027-28: Refund & Status Guide

New Income Tax Rules 2026 in India: Key Changes & Impact

How to File Nil ITR Online for Companies & Individuals?

Top 10 Tax Consultants in India You Should Know in 2026

TDS Compliance Checklist for Private Limited Company

Understanding Section 194C of the Income Tax Act

A Simple Guide to Income Tax Rebate Under Section 87A