GST Return Filing Online in India

File your GST returns online in India with RegisterKaro. Get expert assistance with GSTR-1, GSTR-3B, GSTR-9, & ITC claims, ensuring timely, accurate, and compliant submissions every filing period.

Complete Your GST Return Filing in No Time

Curious about how GST return filing works with RegisterKaro? This short video walks you through the real process—how businesses just like yours get their returns filed smoothly without delays or confusion.

See what happens behind the scenes and why thousands trust us for timely, accurate GST return filing.

Got questions?

What is the GST Return?

A GST (Goods and Services Tax) return is an official document providing a comprehensive record of a business's financial activities. It provides a summary of sales and purchases, including the tax collected on sales (output tax) and the tax paid on purchases (input tax). Businesses must submit these returns electronically through the Government of India's official GST portal.

Under the GST regime, regular businesses with an annual aggregate turnover exceeding Rs. 5 crore are required to file two main monthly returns: GSTR-1 (details of outward supplies) and GSTR-3B (a summary return). In addition to these, most regular taxpayers must also file an annual return, bringing the total to as many as 25 returns per year for a monthly filer.

This process ensures compliance with tax regulations and forms the backbone of the Goods and Services Tax Network (GSTN). Even if a business has no activity during a tax period, filing a 'nil' return is mandatory to maintain compliance.

What Information is Submitted in a GST Return?

GST returns require detailed information on all sales and purchases of goods and services. Businesses report two key GST details: the GST they collect on sales (output GST) and the GST they pay on purchases, which they can claim as Input Tax Credit (ITC).

Key details required include:

| Category | Details to Submit |

| Basic Information |

|

| Outward Supplies (Sales) |

|

| Inward Supplies (Purchases) |

|

| Tax & Credit |

|

| Adjustments |

|

The Role of GST Return Filing in India's Tax System

The GST system transformed India's indirect tax landscape in 2017 by replacing multiple central and state levies with a unified structure. This change required businesses to file regular GST returns to comply with tax regulations.

Here’s why GST Return Filing has evolved the Indian Tax System:

- Enable accurate calculation of a business’s net tax liability

- Ensure compliance with Indian tax laws and regulations

- Maintain transparent, auditable records of business transactions

- Help the government monitor tax collection and track supply chains

- Aid in detecting and preventing tax evasion

- Allow businesses to claim Input Tax Credit (ITC)

- Prevent the cascading effect of taxes (tax on tax)

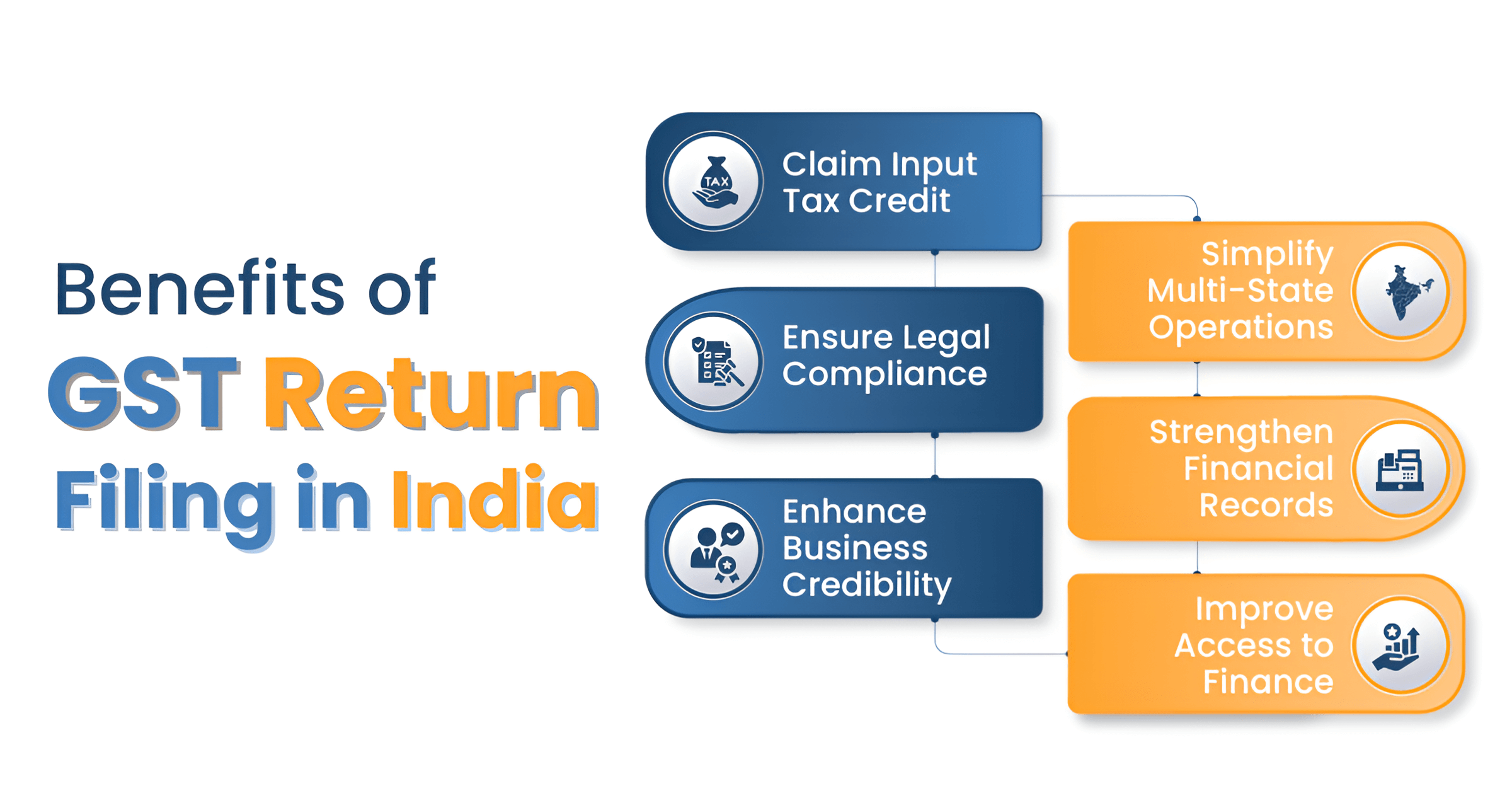

Importance of Accurate and Timely Filing

Filing GST returns within the specified deadlines is crucial to avoid financial penalties. Late filing incurs interest charges and late fees of up to Rs. 100 per day. Apart from avoiding fines, the return filing also presents a vital aspect of business operations and credibility.

- Avoiding Penalties and Late Fees: Timely submission prevents financial burdens from penalties and late fees. These charges can significantly impact a business's profitability.

- Claiming Input Tax Credit (ITC): ITC allows businesses to claim credit for the GST paid on purchases used for business purposes. This valuable credit can only be claimed if GST returns are filed on time.

- Maintaining Compliance and Credibility: Regular and accurate filing demonstrates a business's commitment to tax compliance. A good compliance rating enhances a business's reputation, which can be beneficial when applying for loans, tenders, or attracting investors.

- Tracking Business Performance: The data derived from regular checks offers a clear snapshot of sales, purchases, and tax flows, aiding strategic planning. Businesses can use this data to track their performance, spot areas that need improvement, and make smarter financial decisions.

- Reduced Risk of Audits: Timely and accurate filing significantly decreases the likelihood of a business being selected for an audit by tax authorities. This saves considerable time, resources, and potential stress associated with tax audits, allowing businesses to focus on core operations.

- Streamlined Business Operations: Consistent GST return filing helps maintain organized financial records. This simplifies overall tax compliance for a business, making operations smoother and more efficient.

Who Should File GST Return?

Requirements for filing GST returns vary based on business turnover and type.

Registered Dealers and Businesses

Every business registered under GST must file its returns regularly. The general thresholds for GST registration, which then mandate filing, are:

- Businesses with an annual turnover exceeding Rs. 20 Lakhs.

- For businesses dealing exclusively in goods, the threshold is higher, at Rs. 40 Lakhs.

- For businesses providing only services or dealing in both goods and services, the threshold remains Rs. 20 Lakhs.

- Special category states have lower thresholds of Rs. 20 Lakhs for goods and Rs. 10 Lakhs for services:

- Arunachal Pradesh

- Manipur

- Meghalaya

- Mizoram

- Nagaland

- Tripura

- Sikkim

- Himachal Pradesh

- Uttarakhand

- Jammu & Kashmir

All normal taxpayers and casual taxpayers are required to file Form GSTR-3B.

Taxpayers Under the Composition Scheme

Small traders with a yearly turnover of Rs. 1.5 Crores or less can opt for the Composition Scheme. This scheme simplifies GST compliance, allowing them to file a single annual return, GSTR-4. Additionally, they must file a simple challan in Form CMP-08 quarterly for tax payments.

It recognizes that a "one-size-fits-all" approach would be overly burdensome for micro and small enterprises.

Specific Cases of GST Return Filing

Beyond general businesses, specific entities have distinct GST filing obligations:

- E-commerce Operators: E-commerce operators must obtain GST registration irrespective of their value of supply. They must file GSTR-8 monthly, detailing supplies affected through their platform and Tax Collected at Source (TCS).

- Input Service Distributors (ISD): An Input Service Distributor (ISD) is a business office that receives invoices for services used by its various branches and then distributes the tax credit to those branches. ISDs must register as such, in addition to their normal taxpayer registration, and file GSTR-6 monthly by the 13th of the succeeding month.

- Non-Resident Taxable Persons: Individuals or entities conducting taxable transactions in India without a fixed business location must file GSTR-5 monthly.

- TDS Deductors: Registered persons required to deduct tax at source under GST rules must file GSTR-7 monthly.

- Persons with Unique Identification Number (UIN): Entities like UN bodies or embassies, granted a UIN, must file GSTR-11 monthly, detailing inward supplies for refund claims.

Exemptions from GST Return Filing

While most registered businesses must file GST returns, certain situations or entities may have specific exemptions or simplified requirements.

- Agriculturalists (Farmers): Generally exempt from GST.

- Small Businesses: Individuals and companies with yearly sales below the prescribed turnover thresholds (Rs. 40 Lakhs for goods, Rs. 20 Lakhs for services/mixed, or lower for special category states).

- Suppliers of Exempt/Nil-Rated Goods & Services: Those dealing exclusively in supplies such as certain food products, healthcare, and education services.

- Non-GST Supplies: Entities dealing with goods or services that fall outside the purview of GST law (e.g., alcohol for human consumption, petrol).

- Government Entities and PSUs: Entities dealing with non-GST supplies or exempted/nil-rated goods/services.

- UN Bodies and Foreign Consulates: While they must register for a unique GST ID, they are only required to file returns for months during which they make purchases.

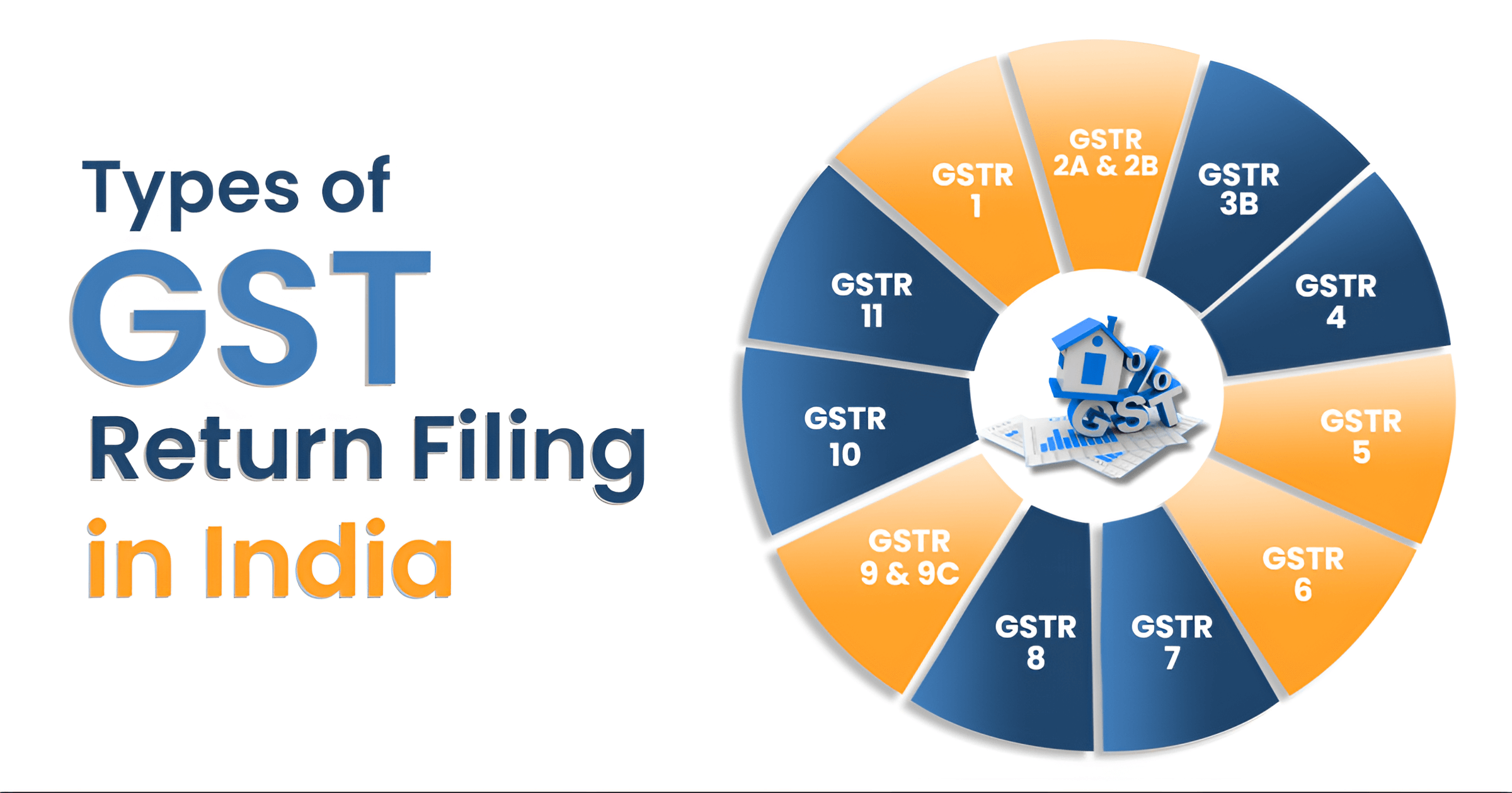

How Many Returns Are There Under GST: Types of Returns

While there are a total of 13 different GST return forms, not all apply to every business. GST returns are primarily structured into monthly, quarterly, and annual filings, depending on the taxpayer's Aggregate Annual Turnover (AATO) and business type.

-

Monthly GST Returns

Businesses with an annual turnover exceeding Rs. 5 crore are generally required to file monthly returns, specifically GSTR-1 (outward supplies) and GSTR-3B (summary return). This frequency ensures faster Input Tax Credit (ITC) claims and smoother compliance for high-volume businesses.

-

Quarterly GST Returns (QRMP Scheme)

Businesses with an annual turnover of up to Rs. 5 crore can choose to file GST returns quarterly under the Quarterly Return Monthly Payment (QRMP) scheme. Under this scheme, taxpayers file GSTR-3B quarterly but pay tax monthly.

They also have the option to file GSTR-1 monthly or quarterly. This reduces the compliance burden for Micro, Small, and Medium Enterprises (MSMEs).

-

Annual Filings

All regular taxpayers must file an annual return, GSTR-9, by December 31st of the next financial year. Composition scheme taxpayers file GSTR-4 annually.

GST Return Filing Categorization: Based on Taxpayer Type

The variety of GST returns caters to different taxpayer categories, ensuring tailored compliance requirements:

| Return Type | Applicable To | Purpose | Frequency | Due Date |

| GSTR-1 | Regular Taxpayers | Report outward supplies and tax liability | Monthly/Quarterly | 11th (monthly) / 13th (quarterly) of next month |

| GSTR-2A | Regular Taxpayers | Auto-drafted purchase return (dynamic) | Auto-generated | Ongoing (view-only) |

| GSTR-2B | Regular Taxpayers | Static monthly purchase return with ITC info | Auto-generated Monthly | 14th of next month |

| GSTR-3B | Regular Taxpayers | Summary of sales, ITC, and tax payable | Monthly/Quarterly | 20th / 22nd / 24th of next month (based on state) |

| GSTR-4 | Composition Scheme Taxpayers | Annual return declaring turnover and tax paid | Annually | 30th April of the following FY |

| CMP-08 | Composition Scheme Taxpayers | Statement for self-assessed tax payment | Quarterly | 18th of the month following the quarter |

| GSTR-5 | Non-Resident Taxable Persons | Report taxable supplies and tax payable | Monthly | 20th or within 7 days of business closure |

| GSTR-6 | Input Service Distributors (ISD) | Distribute ITC to branches | Monthly | 13th of the following month |

| GSTR-7 | TDS Deductors | Report tax deducted and credits to deductees | Monthly | 10th of the following month |

| GSTR-8 | E-commerce Operators | Report supplies made and TCS collected | Monthly | 10th of the following month |

| GSTR-9 | Regular Taxpayers | Annual return summarizing GSTR-1 & 3B | Annually | 31st December of the following FY |

| GSTR-9C | Businesses with turnover > Rs. 5 crore | Audit & reconciliation statement | Annually | 31st December of the following FY |

| GSTR-10 | Taxpayers with Cancelled GSTIN | Final return post cancellation | One-time | Within 3 months of cancellation |

| GSTR-11 | UIN Holders (e.g., Embassies) | Claim GST refund on inward supplies | Monthly | 28th of each month |

Simplification of the Return Filing Process Over Time

The GST Council has consistently introduced measures to simplify the GST return filing process, aiming to ease compliance, especially for small businesses. Key initiatives include:

- Sahaj and Sugam forms for simplified return filing.

- For businesses with a turnover up to Rs. 5 crore, quarterly filing options are available.

- Auto-drafted GSTR-2B to assist with Input Tax Credit (ITC) reconciliation.

These steps reduce filing frequency and minimize errors in reporting. Additional simplifications include:

- Real-time invoice matching

- Offline tools and APIs for return preparation

- Digital authentication via DSC or EVC

- Facility to file NIL returns via SMS.

Taxpayers can also amend returns to correct errors, helping avoid penalties.

How to File GST Returns Online?

To file GST returns online, taxpayers need a GST Identification Number (GSTIN) and a registered account on the official GST portal. Here is a step-by-step guide to filing GST returns online:

Step 1 - Log in to the GST Portal

Visit the official GST website (gst.gov.in). Enter your GSTIN, username, and password. Complete the CAPTCHA verification and click "Login".

Step 2 - Select the GST Return Form

Navigate to the 'Services' tab, then click on 'Returns' and select 'Returns Dashboard'. Choose the financial year and the relevant return filing period (month/quarter). Select the appropriate GST return form (e.g., GSTR-1, GSTR-3B).

Step 3 - Enter Business Details

Fill in details of your sales (outward supplies), purchases (inward supplies), input tax credit (ITC), and tax liabilities. Make sure all details are accurate before uploading, as any errors can result in penalties.

Step 4 - Upload Invoices and Sales Data

Upload invoices for outward supplies in the prescribed format. If applicable, add invoices for purchases to claim Input Tax Credit (ITC).

Step 5 - Review and Validate Data

Cross-check all entered details before submission. The system may auto-calculate the tax payable after ITC adjustment.

Step 6 - Make GST Payment (If Required)

If there is any net tax liability, proceed with the payment. You can pay using multiple options like net banking, debit/credit card, NEFT/RTGS, or UPI.

Step 7 - Submit the GST Return

Click on 'Submit' to freeze the return data. Once submitted, no further changes can be made for that period. Complete verification using a Digital Signature Certificate (DSC) (mandatory for companies/LLPs) or an Electronic Verification Code (EVC) (OTP sent to registered mobile number).

After successful filing, an Application Reference Number (ARN) is generated, and an acknowledgment receipt can be downloaded for records.

Documents Required for GST Return Filing

Essential documents required for GST return filing include:

- Invoices for Outward Supplies (Sales): These are sales invoices issued to customers. They must include details like GSTIN, name, address, invoice number, date, description of goods/services, value, tax charged, and the supplier's signature.

- Invoices for Inward Supplies (Purchases): These are purchase invoices received from suppliers and contain similar details to sales invoices, including GSTIN, name, address, invoice number, etc. These are vital for claiming the Input Tax Credit (ITC).

- Bank Statements for Reconciliation: Monthly bank statements provide a record of transactions and are essential for reconciling financial records with GST filings.

- Details of Debit and Credit Notes Issued: These notes are issued for returns of goods or changes in value. They must include the original invoice number, revised amount, and differential tax.

- Summary of Inter-state and Intra-state Sales: A consolidated summary of sales categorized by GST rates, distinguishing between sales within the state and to other states.

- Bills of Supply: Issued when selling exempted goods/services or if the business opted for the composition levy. They include basic business details, description, and value of supplies.

- Advance Receipt Vouchers: Required if advance payments are received for future supplies. These vouchers detail the supplier, recipient, description, value, and tax payable on the advance.

- Delivery Challans: Necessary when goods are transported for reasons other than supply (e.g., for job work). They contain details like name, address, GSTIN, goods description, and purpose of transportation.

- Account Ledgers: Comprehensive records of all financial transactions are essential for accurate reporting and audits.

GST Return Filing Due Dates

Adhering to GST return filing due dates is critical to avoid penalties and maintain compliance. The due dates vary based on the type of return and the taxpayer's turnover.

This table outlines common GST return filing due dates:

| GST Return Name | Filing Frequency | Due Date |

| GSTR-1 | Monthly | 11th of the next month |

| GSTR-1 | Quarterly (QRMP Scheme) | 13th of the month succeeding the quarter |

| GSTR-3B | Monthly | 20th of the next month |

| GSTR-3B | Quarterly (QRMP Scheme) | 22nd or 24th of the month succeeding the quarter (depending on state) |

| GSTR-4 | Annually | 30th of the month succeeding the financial year (from FY 2024-25, it's April 30th) |

| GSTR-5 | Monthly (Non-resident taxpayers) | 13th of the next month (amended by Budget 2022, yet to be notified) |

| GSTR-6 | Monthly (ISD) | 13th of the next month |

| GSTR-7 | Monthly (TDS Deductors) | 10th of the next month |

| GSTR-8 | Monthly (E-commerce Operators) | 10th of the next month |

| GSTR-9 / GSTR-9C | Annually | 31st December of the next financial year |

| GSTR-10 | Once (Final Return) | Within 3 months of the cancellation date or order |

| CMP-08 | Quarterly (Composition Levy) | 18th of the month succeeding the quarter |

| ITC-04 | Annually/Half-yearly | 25th April / 25th October |

Note: Due dates are subject to changes by CBIC notifications/orders.

Penalty for Delayed GST Return Filing: Interest and Late Fees

Failing to submit GST returns on time incurs financial penalties, including late fees and interest.

- Interest Charges: Interest is applicable at 18% per annum on the outstanding tax amount. Interest starts accumulating from the day after the filing due date and continues until the payment is made.

- Late Fees Structure:

- GSTR-1: Rs. 200 per day (Rs. 100 CGST + Rs. 100 SGST).

- GSTR-3B:

- Rs. 20 per day (Rs. 10 CGST + Rs. 10 SGST) for Nil returns.

- Rs. 50 per day (Rs. 25 CGST + Rs. 25 SGST) for all other situations.

- The maximum late fee for GSTR-3B is Rs. 10,000 (Rs. 5,000 CGST + Rs. 5,000 SGST).

- GSTR-9 and GSTR-9A: Rs. 200 per day (Rs. 100 CGST + Rs. 100 SGST) up to a limit of 0.50% (0.25% CGST + 0.25% SGST) of turnover.

- GSTR-10 (Final Return): Rs. 200 per day (Rs. 100 CGST + Rs. 100 SGST), with no upper limit to the penalty.

- General Penalty: Beyond late fees and interest, a general penalty of up to Rs. 5,000 may be imposed for violating any provision of the GST Act or rules.

- Late Fee Payment Rule: Late fees must be paid in cash only. They cannot be adjusted using the Input Tax Credit (ITC) from your electronic credit ledger.

Failure to file GSTRs for six continuous months can lead to the suspension and potential cancellation of GST registration.

How to Check GST Return Status?

Taxpayers can track their GST return filing status online through the official GST portal using various options.

-

Tracking Through ARN

The Application Reference Number (ARN) is a unique 15-digit code received after submitting a GST application or return. It confirms that the GST system has received the application.

To track using ARN:

- Visit the GST Portal: Go to the official GST website (www.gst.gov.in).

- Log in to Your Account: Click the 'Login' button and enter your username and password.

- Navigate to Track Return Status: On the dashboard, click 'Services' > 'Returns' > 'Track Return Status'.

- Choose ARN Option: Select 'ARN' from the tracking methods.

- Enter ARN: Input the ARN received via email or SMS.

- Click Search: Click the 'Search' button to view the return status.

b. Tracking through GST Returns Filing Period

This method allows checking the status of all returns filed within a specific timeframe.

To track using the filing period:

- Visit the GST Portal and Log in: Similar to the ARN method, you need to log in through the GST portal with your username & password.

- Navigate to Track Return Status: Click “Returns” on the “Services” option from the navigation menu. Then select “Track Return Status”.

- Choose Return Filing Period Option: Select 'Return Filing Period'.

- Select Dates: Use the calendar to select the start and end dates for the period (DD/MM/YYYY).

- Click Search: Click the 'Search' button. The portal will display the status of all returns filed during that period.

c. Tracking by Filing Status

This method allows filtering returns by their current processing status.

To track using status:

- Visit the GST Portal and Log in: Log in through your GST account and select Track Return Status.

- Choose Status Option: Select 'Status' from the tracking methods.

- Select Specific Status: Choose the desired status (e.g., Filed-Valid, Filed-Invalid, Validated but not filed) from the dropdown menu.

- Click Search: Click the 'Search' button. A list of all returns matching the selected status will be shown.

How to Download GST Returns Online?

Taxpayers can easily download their filed GST return forms from the official GST portal for record-keeping and verification purposes.

Here are the steps to download GST return forms:

- Visit the GST Portal: Go to the official GST website.

- Log in to Your GST Account: Click the “Login” button, enter your Username and Password, and input the Captcha code. Click “LOGIN”.

- Navigate to the ‘Returns Dashboard’: Once logged in, click on the “Services” tab, then “Returns,” and select “Returns Dashboard”.

- Select the Financial Year and Period: Choose the specific financial year and the appropriate return period (monthly, quarterly, or annually) for which you want to download the return form.

- Download the GST Return Form: Click on the specific form type (e.g., GSTR-1, GSTR-3B) to open it. Look for the “Download” option and click on it. The form will be downloaded to your device, typically in PDF or Excel format.

Past GST return forms can be accessed by selecting the relevant financial year and return period on the "Returns Dashboard".

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

What is Input Tax Credit (ITC), and how does it relate to GST returns?

−Input Tax Credit (ITC) is the credit of tax paid on purchases of goods or services used for business purposes. When you file your GST returns (specifically GSTR-3B), you declare the ITC you wish to claim. This claimed ITC is then offset against your output GST liability (tax on sales), reducing your overall tax payable. Accurate reporting of ITC in your returns is crucial to avoid discrepancies and maximize your credit benefit.

Is filing a nil GST return necessary?

+What are the consequences of late GST return filing?

+Can a GST return be filed offline?

+What documents are needed for GST return filing?

+How often should GST returns be filed?

+Who is eligible for GST return filing?

+What is the turnover limit for GST return filing?

+How can one check if a vendor has filed their GST return?

+What is the difference between GSTR-2A and GSTR-2B? Which one should I rely on for ITC?

+What is GSTR-9 (Annual Return), and who needs to file it?

+What is GSTR-9C, and its importance?

+What is GSTR-10 (Final Return), and when should it be filed?

+How can I check my GST return filing status online?

+What happens if I stop my business but don't cancel my GST registration?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for GST Return Filing?

Here’s why countless businesses trust RegisterKaro for their GST compliance:

- End-to-End GST Management: We handle your GSTR-1, GSTR-3B, annual returns (GSTR-9/9C), ITC reconciliation, and all other essential GST filings.

- Expert Tax Advisors: Get tailored solutions and proactive guidance from our seasoned team of GST professionals, ensuring accurate and compliant submissions.

- Transparent Fees & Timelines: Benefit from clear, upfront pricing and efficient processes, designed for timely GST return filing without hidden costs.

- Seamless Compliance: Rely on us not just for filing, but for ongoing GST advisory, notice handling, and statutory compliance, keeping your business stress-free.

- Proven Reliability: Join thousands of businesses that trust our expertise for accurate GST compliance and financial peace of mind.

Contact RegisterKaro to avail of GST Return Filing services with a customized quotation and affordable prices.

What Our Clients Say

View AllDebjit Chakraborty

I had a mixed experience at the beginning with many people calling and trying to give misleading information to take the complete payment asap, till M... Read more

Rimisha Dehuri

I had a fantastic experience with RegisterKaro! Satyapriya Tripathi was incredibly helpful and knowledgeable. I needed assistance with ROC filing, GST... Read more

Shekh Kamsuddeen

I’ve been using RegisterKaro for my GST compliance for quite some time now, and the experience has been consistently smooth. The team ensures timely f... Read more

Abhisar Pratap Singh

My experience with registerkaro has been very bittersweet. The Incorporation experience has been very smooth, special thanks to Prathistha, but my vir... Read more

Prem Kumar

I opted for register Karo for getting my company registered. And there work is magnificent. I really liked how they call every single time if there is... Read more

Kapil Kumar

I am very satisfied with the services provided by RegisterKaro. Diksha supported us throughout the entire compliance process, including GST and MSME r... Read more

Rupam Chaudhuri

Great experience so far engaging with RegisterKaro team. All the team members are exceptionally polite and knowledgeable. I had my point of contact wi... Read more

Rishi Bakshi

Purvi Gupta has been exceptionally reliable in managing all GST-related work, including filings and compliance tasks. Her dedication, patience, and at... Read more

WINS MARINE

I had a great experience getting my Section 8 company registered with the help of Shruti Pandey. She was very professional, knowledgeable, and guided... Read more

Arnav singh

In managing the company incorporation tasks, SnehaLata Yadav’s exceptional dedication and professional approach have stood out. Her efficiency, eye fo... Read more

Related Blogs

View All

How to Apply for GST Registration After Rejection in India

GST Notice Guide: Types, Reasons, Reply Format, and Penalties

GST for Advertising & Digital Marketing Services 2026 Guide

GST Registration for Export of Services in 2026: Conditions, LUT & Refund

GST for Consultancy Services in India 2026: Rates, SAC Codes & Compliance

How to Reply to GST Registration Notice 2026: REG-04, REG-18 & Format

GST for Software & IT Services in India 2026: Rate, SAC Codes & Exports

GST for Professional Services in India 2026: Limit, Rate & Process

GST for Freelancers in India 2026: Registration, Rates & RCM Guide

GST Compliance Calendar 2026-27: GST Return Due Dates, Forms & Deadlines