Professional Tax Registration Online in India

Get your professional tax registration done right. We simplify state compliance for businesses and professionals so you can focus on what matters most.

What is Professional Tax Registration?

Professional tax registration is the process where employers and businesses register with their state's Commercial Tax Department for collecting and paying professional tax. It’s a state-level levy regulated by the State Professional Tax Acts, allowing governments to tax professions, trades, and employment.

According to Hindustan Times, Professional tax collections have increased by 27% in major Indian states over the last two years, with enforcement becoming significantly stricter. This trend demonstrates the growing importance of timely professional tax registration for businesses and professionals across India.

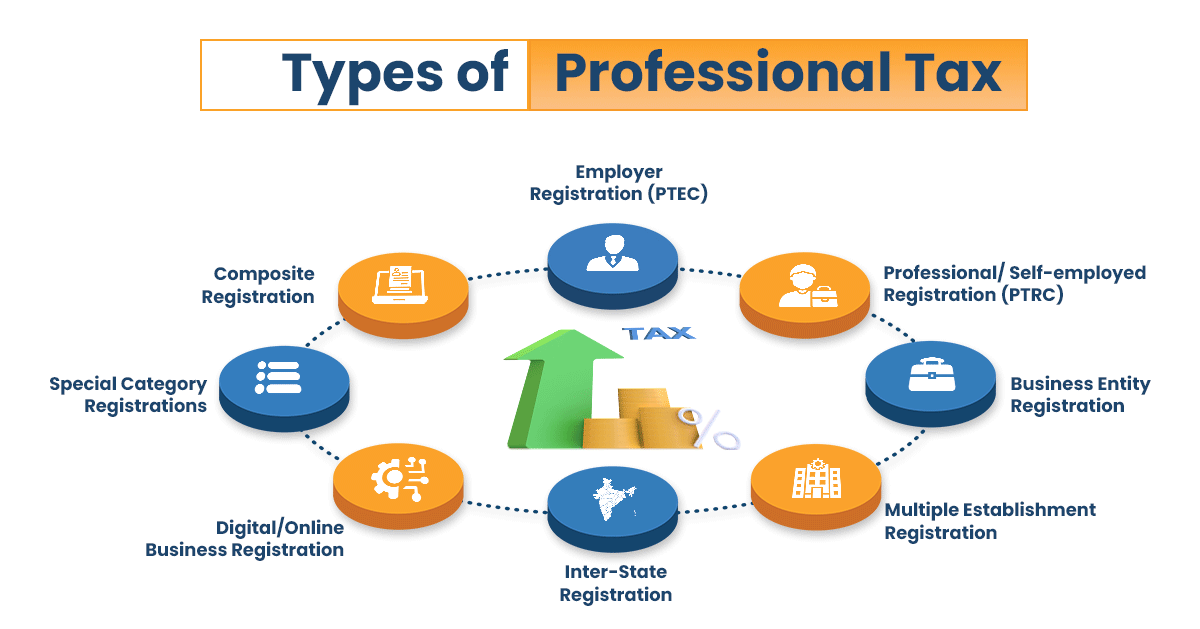

Types of Professional Tax Registration

Professional tax registration applies to various entities and situations. The two main certificates are PTEC and PTRC, but registration is also required in the following scenarios:

1. Employer Registration (PTRC - Professional Tax Registration Certificate)

Employers must obtain PTRC registration to deduct professional tax from employee salaries and remit it to the state. For instance, a software company with 50 employees in Karnataka needs this registration to deduct professional tax from its employees' salaries.

2. Professional/Self-employed Registration (PTEC - Professional Tax Enrollment Certificate)

This is mandatory for self-employed professionals, consultants, and individuals engaged in any trade or profession, for their professional tax liability. For example, a chartered accountant in Maharashtra must obtain PTEC registration for their professional tax compliance.

3. Business Entity Registration

Partnerships, LLPs, and other business entities must register for requirements based on their structure and state laws.

For example: a retail partnership in Tamil Nadu must register for professional tax according to its annual turnover.

a. Multiple Establishment Registration

Businesses with multiple locations in the same state must register each establishment separately.

For instance: a restaurant chain with 5 outlets in West Bengal needs individual professional tax registrations for each location.

b. Inter-State Professional Tax Registration

Businesses operating in multiple states must register in each one.

Example: A consulting firm serving Gujarat and Maharashtra needs separate registrations in both states.

c. Digital Platforms and Online Businesses Registration

Digital businesses and online service providers must meet state-specific registration requirements.

For instance: an e-commerce business in Telangana must register for professional tax, regardless of whether it has a physical retail location.

d. Special Category Registrations

Certain professions, such as doctors, lawyers, and architects, require specialized registration.

For example: lawyers in Kerala must register under a specific category for legal professionals.

e. Composite Registration

Combined registration options for professionals with multiple business structures in certain states.

For example: a doctor in Odisha with a private practice and a consultancy may qualify for combined registration.

Rules and Regulations for Professional Tax Registration

Professional tax registration is governed by state-specific regulations that outline the procedure for professional tax registration, eligibility, and compliance requirements.

1. Article 276 of the Constitution of India - Empowers states to levy taxes on professions, trades, callings, and employments, with a maximum professional tax limit of Rs. 2,500 per person annually.

2. State-specific Professional Tax Acts - Each state has its legislation (e.g., Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975; Karnataka Tax on Professions, Trades, Callings and Employments Act, 1976).

3. Professional Tax Rules - Procedural regulations detailing registration, payment schedules, returns filing, and penalties in each state.

4. State Finance Acts - Annual modifications to professional tax slabs, exemptions, and procedural requirements for professional tax registration.

5. Municipal Corporation Acts - In some states, municipal bodies are authorized to collect professional tax within their jurisdiction.

Characteristics of a Professional Tax Registration

Professional tax registration has distinct characteristics that shape how these compliance frameworks function:

- State-Specific Nature: Professional tax regulations differ widely from one state to another.

-

- This means the requirements, rates, and procedures for professional tax registration vary significantly across different states, with some states not imposing professional tax at all.

- This highlights the critical need for businesses to be aware of and comply with the specific local tax regulations of their respective states.

- Slab-Based Structure: Professional tax is calculated as follows:

-

- Typically, the tax amounts follow a progressive structure: higher income earners or larger businesses may face higher tax rates, while those with smaller incomes or businesses might benefit from lower rates or even exemptions.

- Dual Registration System: It's important to understand that different registrations apply to employers and self-employed professionals. Distinct registration requirements exist:

-

- PTRC (Professional Tax Registration Certificate): Employers must register for PTRC to deduct professional tax from their employees' salaries and remit it to the state.

- PTEC (Professional Tax Enrollment Certificate): Self-employed professionals, such as lawyers, doctors, or consultants, and business entities (like sole proprietorships or companies for their liability), must obtain PTEC for their professional tax compliance.

- Annual Renewal of Professional Tax Registration is Not Required: Unlike many other business registrations, professional tax registration is typically a one-time process. However, this doesn't mean you're done; regular filing of returns and timely payments are continuously required to ensure ongoing compliance with your tax obligations.

- Employer Responsibility: Professional tax laws place a clear legal obligation on employers to deduct and deposit the professional tax for their employees. Employers are directly responsible for ensuring that it is correctly deducted from employees' salaries and remitted to the state government within the stipulated deadlines.

- Location-Based Compliance: Businesses with multiple branches or offices often need separate registrations. If you operate different branches or offices in various locations within the same state, each establishment may require individual professional tax registration. This ensures compliance specific to each operational unit.

- Calendar-Specific Payments: Professional tax features specific payment schedules that vary by state and registration category. Payments can be monthly, quarterly, or half-yearly. Businesses must strictly adhere to the specific payment timeline set by their state, ensuring timely remittance of professional tax to avoid penalties.

- Limited Transferability: Professional tax registration is generally not portable. This means it is typically not transferable between different business entities (e.g., if a sole proprietorship converts to an LLP) or across state boundaries. If you change your business structure or expand to a new state, you'll likely need new registrations.

Why Should You Register for Your Professional Tax?

When establishing professional tax registration in India, professional assistance provides significant advantages:

Legal Compliance

Professional tax registration ensures businesses follow state tax laws.

- Ensures adherence to state-specific tax laws and regulations.

- Helps businesses stay compliant with local professional tax requirements, avoiding legal issues.

Business Credibility

Compliance enhances a business’s trustworthiness and professional image.

- Enhances business reputation with official tax registration status.

- Builds trust with clients, partners, and investors by demonstrating legal tax compliance.

Penalty Avoidance

Timely registration and filing help avoid financial and legal penalties.

- Prevents costly fines and interest charges for non-compliance.

- Ensures businesses avoid penalties by maintaining proper professional tax registration and filings.

Tender Professional Tax Registration Eligibility

Essential for qualifying to bid on government contracts and tenders.

- Enables participation in government tenders and contracts that require professional tax certification.

- Professional tax registration is often a mandatory requirement for securing government contracts.

Loan Facilitation

Tax compliance supports credibility during loan evaluation processes.

- Supports business loan applications by demonstrating regulatory compliance.

- Provides financial institutions with proof that the business meets all legal tax obligations, easing loan approval.

Audit Protection

Having proper tax records ensures readiness for audits and inspections.

- Creates compliance records that simplify tax audits and regulatory inspections.

- Well-maintained professional tax registration ensures that businesses are prepared for audits and inspections.

Professional Tax Applicable States across India

Professional tax is applicable in various states across India in the following manner:

- State-Specific: Professional Tax is a state-level tax, meaning the rates, slabs, and even the method of calculation (monthly, half-yearly, annually) differ significantly from one state to another.

- Slab-Based: The amount of Professional Tax payable is almost always based on categories of profession/turnover for:

-

- Income slabs (monthly or annual salary/gross income) or,

- Self-employed professionals/businesses.

- Maximum Limit: As per Article 276 of the Constitution of India, the maximum amount of Professional Tax that can be levied on any individual or entity in a financial year cannot exceed Rs. 2,500.

This means the highest monthly deduction would typically be Rs. 200 - Rs. 208 for 11 months, with sometimes a slightly higher amount in one specific month (e.g., February in Maharashtra) to reach the annual cap of Rs. 2,500.

Exemptions

Many states also provide exemptions for certain categories of individuals, such as very low-income earners, persons with disabilities, senior citizens (above a certain age, which varies by state), or specific military personnel.

Here's a general overview of how amounts typically range, keeping the Rs. 2,500 annual cap in mind:

- Nil Tax: Most states have a "Nil" slab for lower income brackets. This threshold varies widely, from around Rs. 5,000 to Rs. 25,000+ monthly income, depending on the state.

- Tiered Slabs: As income increases, the professional tax amount also increases progressively. Common monthly professional tax amounts in various slabs can be: Rs. 75, Rs. 120, Rs. 150, Rs. 175, Rs. 180, Rs. 200.

- Maximum Monthly: For most income earners above a certain threshold, the tax tends to stabilize at the equivalent of the annual maximum divided by 12 months, which is approximately Rs. 208 per month. Some states might have a slightly higher amount in one month (e.g., Rs. 300 in February for Maharashtra or December for MP/Odisha) to balance out the year and reach the Rs. 2,500 annual limit.

- Annual Payments for Self-Employed: For self-employed individuals or businesses, the tax might be a fixed annual amount (e.g., Rs. 1,000, Rs. 2,000, Rs. 2,500) based on their profession category or annual turnover, or sometimes a monthly payment.

Examples from Key States (illustrative, for current FY 2024-25, subject to change):

- Maharashtra:

- Monthly Income up to Rs. 7,500 (Male) / Rs. 25,000 (Female): NIL

- Monthly Income Rs. 7,501 to Rs. 10,000 (Male): Rs. 175 per month

- Monthly Income above Rs. 10,001 (Male) / above Rs. 25,000 (Female): Rs. 200 per month (Rs. 300 in February)

- Karnataka:

- Monthly Income up to Rs. 24,999: NIL

- Monthly Income Rs. 25,000 and above: Rs. 200 per month

- Tamil Nadu:

- Half-yearly income up to Rs. 21,000: NIL

- Half-yearly income above Rs. 75,001: Rs. 1,250 (which is Rs. 2,500 annually)

- Gujarat:

- Monthly Income up to Rs. 12,000: NIL

- Monthly Income above Rs. 12,000: Rs. 200 per month

Eligibility Criteria for Professional Tax Registration

Professional tax registration is required for individuals and entities engaging in specific professional or business activities as per state regulations.

1. Income Threshold - Individuals earning above the state-specified minimum income level (varies by state, typically ranging from Rs 5,000 to Rs 10,000 monthly).

2. Professional Status - Individuals practicing professions such as medicine, law, accounting, engineering, architecture, and consultancy services.

3. Business Operation - All businesses, including sole proprietorships, partnerships, LLPs, and companies operating within a professional tax-levying state.

4. Employer Status - Any entity employing individuals and liable to deduct professional tax from employee salaries.

5. State Presence - Physical location or business operations within the jurisdiction of a state that imposes professional tax.

6. Trade Engagement - Individuals or entities engaged in specified trades or commercial activities as defined in the state's professional tax schedule.

7. Service Provision - Providers of professional services, including coaching, training, technical services, and specialized consultations.

Meeting these statutory and operational requirements necessitates registration under the respective state's professional tax regime to maintain compliance and avoid penalties.

Documents Required for Professional Tax Registration

An effective professional tax registration requires proper documentation to establish business legitimacy and professional status:

- Identity Proof

- PAN card: Required for tax identification.

- Aadhaar card: Used for identity verification.

- Voter ID: Can also serve as proof of identity for individuals.

- Incorporation certificate: Required for business entities.

- Partnership deed: Needed for partnership firms.

- Address Proof

- Utility bills: Showing the address of the business premises.

- Property documents: Verifying ownership of business premises.

- Rental agreements: Proof of rented premises used for business operations.

- Business Registration Documents

- GSTIN certificate: Proof of GST registration for businesses.

- Shop and establishment license: Required for businesses operating in specific states.

- MSME registration: Certificate for MSME registration.

- Other business registration certificates: Additional documents based on business type.

- Bank Account Details

- Bank statements: For business or professional transactions.

- Canceled cheque leaf: Proof of business account used for transactions.

- Employee Details

- List of employees: Including their salary details for employer registration.

- Designation and salary structure: Required for tax compliance regarding employees.

- Professional Credentials

- Certificates of practice: For regulated professions like doctors or lawyers.

- Professional degrees: Required for specific professions such as CA, doctors, etc.

- Licenses: For specialized professionals needing legal or regulatory approval.

- Recent passport-sized photographs: Of the proprietor, partners, or authorized representatives as required by the state.

- Digital Signature

- Digital Signature Certificate: DSC is needed for the online professional tax registration process in states with a digital system.

How to Register for Professional Tax

Establishing effective professional tax registration requires careful planning and execution:

1. Determine Registration Requirement

Assess whether your business or profession falls under the professional tax purview in your state and identify the applicable registration category.

2. Collect Required Documents

Gather all required documents, including business registration certificates, identity proofs, address verification, and other state-specific requirements.

3. Complete Application Form

Fill the appropriate professional tax registration form (typically Form I for employers/PTEC and Form II for professionals/PTRC) with accurate business or professional details.

While professional tax is a state-level tax, leading to variations across India, it's less about one state having a unique process and more about differences in specific details, forms, online portals, and compliance nuances.

For instance, states like:

Maharashtra Professional Tax: Maharashtra has well-established online systems and explicitly uses Form I for PTRC and Form II for PTEC, which, while a common structure, isn't universally adopted across all professional tax-levying states.

Karnataka Professional Tax: The professional tax registration process is primarily handled through the e-PRERANA portal (Profession Tax Enrolment Registration And Administration), managed by the Commercial Taxes Department, Government of Karnataka.

West Bengal Professional Tax: In West Bengal, professional tax is regulated by the West Bengal State Tax on Professions, Trades, Callings and Employment Act, 1979, with the primary online portal being professiontax.wb.gov.in. Employers typically file Form III as their return and remit the collected tax by the 15th day of the following month, though smaller payers might have an annual return option by April 30th, following the end of their accounting year.

Tamil Nadu Professional Tax: In Tamil Nadu, professional tax is levied by local bodies such as Municipalities and Corporations, rather than a single state-wide authority, under the Tamil Nadu Municipal Laws. Consequently, the registration and payment processes are often handled through the specific municipal corporation's online portal.

Therefore, it's crucial for individuals and businesses to always consult the official website of the Commercial Tax Department (or equivalent authority) of the relevant state for accurate and current registration procedures and forms.

4. Pay Registration Fees

Submit the applicable professional tax registration fees as prescribed by the state government, which may vary based on business category and state, such as Rs. 2,500 annually in Maharashtra for certain businesses.

5. Submit Application

File the completed application along with supporting documents either online or physically at the designated office.

6. Verification Process

Undergo any verification procedures required by the tax authorities, which may include document scrutiny or physical premises verification in some states.

7. Certificate Issuance

PTEC (Professional Tax Enrollment Certificate) is for professionals (self-employed individuals) and entities paying their professional tax.

PTRC (Professional Tax Registration Certificate) is for employers who deduct professional tax from their employees' salaries and remit it to the state government.

8. Display Registration Certificate

Prominently display the registration certificate at your business premises as required by most state professional tax laws.

9. Periodic Compliance

Maintain ongoing compliance by timely tax deduction, payment, and returns filing as per the state-specific schedule.

Complete your professional tax registration in no time. RegisterKaro ensures you meet all the professional tax registration requirements and deadlines, avoiding any potential issues. Leave the paperwork to us. Get in touch with our experts today!

Professional Tax Registration Fees and Penalties in India

Understanding the financial aspects and potential penalties associated with professional tax registration is essential for professionals and businesses:

Registration Costs

The registration costs for professional tax registration vary depending on the application, as follows:

- Application Fees: Rs. 100 - Rs. 500, depending on the state and category of registration.

- Certificate Issuance Charges: Rs. 200 - Rs. 1,000 based on business category and state regulations.

- Professional Assistance Fees: Rs. 1,000 - Rs. 5,000 if utilizing services of tax professionals or consultants for registration.

- Digital Signature Costs: Rs. 1,000 - Rs. 3,000 for states requiring a digital signature for online registration.

Professional Tax Payment Structure

Payment structure for a professional tax registration depends on the person seeking it, as follows:

- Salaried Individuals: Typically ranges from Rs. 0 to Rs. 2,500 annually based on salary slabs.

- Professionals/Self-employed: Annual tax between Rs. 1,000 to Rs. 2,500 depending on income and state.

- Business Entities: Fixed amounts or slab-based rates ranging from Rs. 1,000 to Rs. 2,500 annually, based on state and business category.

Charges & Fines

Delays in registration can lead to different types of fines and penalties, as follows:

- Late Registration Penalty: Typically Rs. 5 - Rs. 10 per day of delay, varying by state regulations.

- Non-Registration Penalty: Fines ranging from Rs. 1,000 to Rs. 5,000, depending on the duration of non-compliance and state laws.

- Late Payment Interest: 1-2% per month on the unpaid tax amount in most states.

- Late Filing Penalties: Fixed penalties of Rs. 100 - Rs. 1,000 for delayed submission of returns.

- False Information Submission: Penalties up to Rs. 5,000 plus potential prosecution in severe cases.

- No Deduction by Employers: Additional penalties for employers failing to deduct professional tax from employee salaries.

- Non-Maintenance of Records: Fines of Rs. 1,000 - Rs. 2,000 for failing to maintain required documentation.

Ensure your professional tax registration compliance with RegisterKaro! Get expert guidance and avoid penalties by completing your registration seamlessly today.

Compliance for Professional Tax Registration

Professional Tax compliance in India is a mandatory requirement for individuals and entities earning income from a profession, trade, or employment, depending on the specific state laws.

Here are the key aspects of Professional Tax compliance:

- Mandatory Requirement: Professional Tax compliance is compulsory for individuals and entities earning income from professions, trades, or employment, as per specific state laws.

- Payment Obligation: Once registered, taxpayers are legally bound to pay the professional tax regularly, typically monthly or annually, based on their income slabs or business category.

- Return Filing: Alongside payments, registered entities and individuals must file periodic returns (e.g., monthly, quarterly, or annually) with the respective state professional tax authorities.

- State-Specific Rules: Compliance obligations, including payment amounts, return frequencies, and penalties, vary significantly from one Indian state to another.

- Employers' Role: Employers are responsible for deducting professional tax from their employees' salaries and remitting it to the state government.

- Self-Employed/Professionals: Individuals who are self-employed or run their professions must directly pay their professional tax as per their income or profession.

- Avoidance of Penalties: Timely payment and accurate filing are critical to avoid various penalties, late fees, interest charges, and potential legal issues imposed by state governments for non-compliance.

Professional Tax Registration Certificate

A Professional Tax Registration Certificate is the official document issued by the state's professional tax department upon successful completion of the registration process. This certificate serves as undeniable proof that an individual or entity is legally authorized to operate under the state's professional tax regulations.

Possessing this certificate is not just a formality; it's a legal requirement that enables you to fulfill your professional tax obligations correctly and without impediment. The registration number on the certificate acts as your primary identifier when remitting tax or filing returns with the government authorities.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

What is Professional Tax registration?

Professional tax registration is the process by which individuals and entities liable to pay professional tax register with the respective state's professional tax department. This registration is a mandatory compliance step to ensure they can legally collect or pay this state-level tax. This certificate signifies your compliance and enables you to fulfill your professional tax obligations

How to do Professional Tax registration?

Professional tax registration is primarily done online through the official professional tax portal of the relevant state government. The process generally involves navigating to the "New Registration" section and accurately filling out an application form with business and personal details.

Which states in India levy Professional Tax?

Professional tax is currently levied by several Indian states, reflecting their legislative powers to tax professions, trades, and employment. Key states where it is collected include Maharashtra, Karnataka, Tamil Nadu, Gujarat, Madhya Pradesh, and Odisha. Other states like Kerala, Assam, Meghalaya, and Sikkim also impose this tax, making it crucial to check the specific regulations of your operating state.

Who needs to register for Professional Tax?

Anyone engaged in a profession, trade, or employment within states that levy professional tax is generally required to register. This includes employers who are obligated to deduct professional tax from their employees' salaries. Additionally, self-employed professionals (like doctors, lawyers, consultants) and all forms of business entities operating in these states must also complete the necessary registration.

How long does the Professional Tax registration process take?

The duration for professional tax registration typically ranges from 7 to 15 working days. This timeframe can fluctuate based on the specific state's administrative efficiency and how quickly the submitted documentation is processed. Ensuring all required documents are complete and accurate from the outset can help expedite the registration process.

How much does Professional Tax registration cost?

The cost of professional tax registration varies depending on the specific state and the category of registration. Typically, it includes an application fee ranging from Rs. 100 to Rs. 500. If you choose to utilize the services of tax professionals or consultants for assistance, their fees, usually between Rs. 1,000 to Rs. 5,000, would be an additional cost.

What is the difference between PTEC and PTRC?

PTEC (Professional Tax Enrollment Certificate) is for individuals and entities to pay their professional tax, including self-employed professionals and businesses for their liability. PTRC (Professional Tax Registration Certificate) is for employers to deduct and remit professional tax from their employees' salaries. A business with employees typically needs both PTEC for itself and PTRC for its workforce. Professional Tax is state-specific in India.

Can I apply for Professional Tax registration online?

Yes, the process for professional tax registration has largely moved online in many Indian states. Most state commercial tax departments now provide dedicated portals where you can submit your application electronically. However, it's advisable to check the specific requirements of your state, as some may still necessitate the physical submission of certain documents after online application.

What happens if I don't register for Professional Tax?

Failure to register for professional tax can lead to significant financial penalties imposed by state authorities. You may also incur interest charges on any unpaid tax amounts from the date it was due. Furthermore, non-compliance can result in legal notices, difficulty in obtaining other necessary business licenses, and potential complications with your business operations.

Can I use the same Professional Tax registration for multiple business locations?

Generally, professional tax registration is location-specific within a state. This means that in most states, you would need to obtain separate professional tax registrations for each distinct business location, even if all locations operate under the same business entity. It's crucial to confirm this with the professional tax department of the specific state where your multiple locations are situated.

What happens if my business relocates to another state?

If your business relocates to another state in India, you will need to apply for a new professional tax registration in that new state, provided it levies professional tax. Professional tax registrations are state-specific and are not transferable across state borders. You may also need to formally close or cancel your registration in the previous state.

Is Professional Tax registration different from GST Registration?

Yes, professional tax registration is distinctly different from GST Registration. Professional tax is a direct tax levied by state governments on professions, trades, and employment. In contrast, GST (Goods and Services Tax) is an indirect tax on the supply of goods and services, which is levied and managed jointly by both the central and state governments across India.

How often do I need to file Professional Tax returns?

The frequency for filing professional tax returns varies significantly based on state regulations and often depends on your registration category or tax liability. Returns may be required monthly, quarterly, or half-yearly. It is essential to refer to the specific rules of the state where your business is registered to ensure timely and accurate filing.

Can Professional Tax registration be transferred if ownership of the company changes?

In most states, a new professional tax registration is required if there's a significant change in the ownership structure of the company, especially if it leads to a change in the legal entity. However, for minor changes in ownership that don't alter the fundamental legal structure, some states might permit amendments to the existing registration. It's best to consult the state's professional tax department for precise guidance.

What is the maximum Professional Tax amount payable annually?

As per the provisions of Article 276 of the Constitution of India, there is a constitutional cap on the maximum professional tax payable by any individual. This annual cap is set at Rs. 2,500. This ensures uniformity in the maximum tax burden across different states that levy professional tax.

How do I verify my Professional Tax registration status?

Most states offer convenient online verification facilities through their respective commercial tax department websites. You can typically verify your professional tax registration status by entering your registration number or Permanent Account Number (PAN) into the designated portal. This allows for quick confirmation of your registration's active status.

Do I need Professional Tax registration if I'm already registered for Income Tax?

Yes, professional tax registration is a separate and distinct state-level tax requirement, regardless of whether you are already registered for Income Tax. Income Tax is a central government levy on income, whereas professional tax is imposed by individual state governments on the privilege of engaging in a profession, trade, or employment within their jurisdiction.

How do I update my Professional Tax registration if business details change?

If there are changes in your business details, such as address, business name, or nature of operations, you must file an amendment application with the professional tax department. This application should be accompanied by relevant supporting documents that provide evidence of the changes. Timely updates ensure your registration details remain accurate and compliant.

How to check the Professional Tax registration number?

Your professional tax registration number is typically found on the certificate issued by the state authorities. If you've registered online, you can usually log in to the specific state's professional tax portal using your credentials.

How to close Professional Tax registration?

Closing professional tax registration typically involves submitting a formal application to the professional tax department of the concerned state. The application will require details regarding the cessation of activity and may necessitate supporting documentation. The exact procedure for professional tax registration and required forms for closure vary by state.

How to get a Professional Tax registration certificate online?

You can usually download your professional tax registration certificate online directly from the official professional tax portal of the respective state government. Within the portal, there should be a dedicated section like "Download Certificate," "View Registration," or "Print Certificate" from which you can retrieve and save your certificate.

Is Professional Tax registration mandatory?

Yes, professional tax registration is mandatory for all individuals and entities who are legally required to pay professional tax in a particular state. Failure to register can lead to penalties and legal consequences. Compliance ensures adherence to state tax regulations.

What documents are required for Professional Tax registration?

The documents required for professional tax registration vary based on the state and the type of entity (e.g., individual, proprietorship, company). Commonly requested documents include the PAN Card of the applicant or entity, proof of business address (like a utility bill or rent agreement), and proof of the entity's constitution (e.g., Partnership Deed, Certificate of Incorporation).

What is a Professional Tax registration number?

The professional tax registration number is a unique identification code issued by the state's professional tax department upon successful registration. This number serves as the primary identifier for all professional tax-related compliances and communications.

When is Professional Tax registration required?

Professional tax registration is required when an individual or an entity becomes liable to pay professional tax under the specific state's professional tax act. This typically occurs when a business begins employing individuals in a state that levies professional tax, or when an individual starts practicing a profession or engages in a calling in such a state.

Why is Professional Tax different in every state?

Professional tax varies across Indian states because it is a state-level tax, empowered by Article 276 of the Indian Constitution. This leads to differences in tax rates, professional tax registration applicability criteria for various professions, exemption limits, and compliance procedures.

What is the penalty for violating Professional Tax regulations?

Violating Professional Tax regulations can lead to various penalties, which differ from state to state. Common penalties include fines for non-registration, interest charges for delayed payment of the tax, and penalties for late or non-filing of returns. Severe violations, such as providing false information, can even result in higher financial penalties or legal prosecution. It is crucial to adhere to deadlines and regulations to avoid these consequences.

How is Professional Tax calculated?

For salaried employees, it's typically a monthly deduction from their gross salary, determined by their income bracket as per the state's schedule. For self-employed professionals, it might be a fixed annual amount or based on their gross receipts/income, also specified in pre-defined slabs. The maximum annual professional tax amount payable is capped at Rs. 2,500 by the Indian Constitution.

How does Professional Tax differ from Income Tax?

Professional Tax and Income Tax are distinct in several key aspects. Professional Tax is a state-level tax levied on income from professions, trades, callings, and employment, with a maximum annual limit of Rs. 2,500. Income Tax, conversely, is a central-level tax on total income from all sources (salary, business, capital gains, etc.), without a maximum limit.

Is Professional Tax applicable to all employees and employers?

No, Professional Tax is not uniformly applicable to all employees and employers across India. Professional tax registration applicability is limited to those states that have enacted their professional tax laws. Even within these states, there might be specific income thresholds or categories of employees and employers who are exempt from this tax.

What is Form 1 for Professional Tax registration?

In many Indian states, Form 1 for professional tax registration refers to the application form for a Certificate of Registration (RC) for professional tax. It's the primary document an employer (or sometimes a self-employed individual) uses to register with the state's tax authorities for professional tax purposes.

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for Your Professional Tax Registration Needs?

Here's why we are the trusted choice for professional tax registration services:

- Our specialized tax experts have extensive experience in navigating state-specific professional tax regulations across India.

- We provide step-by-step guidance through the entire professional tax registration process, from document collection to certificate issuance.

- Our team combines local tax expertise with comprehensive knowledge of state variations to create efficient compliance strategies.

- We offer transparent pricing with no hidden costs, ensuring you know exactly what you're paying for.

- Our experts handle all documentation preparation, government liaison, and follow-ups, minimizing your administrative burden.

Stay compliant and avoid penalties with ease. Let RegisterKaro handle your professional tax registration while you focus on growing your business. We simplify the process for you.

What Our Clients Say

View AllNitu Agarwal

A huge credit goes to Registerkaro team for successfully completing my Professional tax registration service. Assigned person was very supportive thro... Read more

sonu kumar

Registerkaro has done a wonderful job. They have completed my Professional tax registration service. The process went smoothly. A huge credit goes to... Read more

Mahesh Kamble

Register karo register karo filed my all GST from the last 6 months . Register karo registered has registered my company and helped me to grow Neha Ch... Read more

Shubham Kumar

I had a great experience with Register Karo. I was assisted by Pranjal, and the process was seamless from start to finish. Pranjal was very cooperativ... Read more

RGRK

Register Karo provides excellent services with strong client satisfaction in terms of time and cost efficiency. Special thanks to Mr. Abhay Bisht, SPO... Read more

deepu star

RegisterKaro has been handling my GST filing for 6 months now and all filings have been on time without delays. Purvi Gupta is responsive and provides... Read more

srijit nair

Very satisfied with the service. The incorporation process was quick, transparent, and well-managed. The team was always available to help whenever ne... Read more

Dimple Parikh

Rahul was very prompt & completed formalities for getting "shop & establishment" certificate seamlessly. He was very courteous during entire proce... Read more

Sanyog Gupta

Internal team is very good & responsive. I like to mention specially Mr. Jagjeevan Singh ji who explained me everything very well and made the things... Read more

Vanshika Agrawal

Working with Amarsh Kesarwani was an incredible experience. His guidance, encouragement, and inspiring leadership made every challenge easier to overc... Read more

Related Blogs

View All

Section 54B of Income Tax Act – Capital Gains Exemption on Agricultural Land

Section 194JB of Income Tax Act,1961 – TDS Rate, Threshold Limit, and Applicability

RTGS Timings in India: Latest Transfer Time, Limits & Rules

Old vs New Tax Regime in India: Comparison for FY 2026-27

Income Tax Refund Delay: Reasons, Status & Faster Refund Tips

ITR Processing Time for AY 2027-28: Refund & Status Guide

New Income Tax Rules 2026 in India: Key Changes & Impact

How to File Nil ITR Online for Companies & Individuals?

Top 10 Tax Consultants in India You Should Know in 2026

TDS Compliance Checklist for Private Limited Company