Every newly incorporated company in India must appoint its first auditor within a strict timeline from the date of registration. The process to appoint the first auditor of a company is governed by Section 139 of the Companies Act, 2013. It is a mandatory compliance obligation, not an optional task that can be deferred until the first AGM.

Under Section 139, the authority to appoint the first auditor depends on the type of company:

- For private and non-government public companies, the Board of Directors must appoint the first auditor within 30 days of incorporation.

- If the Board fails to appoint, members of the company must appoint the auditor at an Extraordinary General Meeting (EGM) within 90 days.

- Government companies: The Comptroller and Auditor General (CAG) of India must appoint the first auditor within 60 days of registration.

- If the CAG fails, the Board of Directors must appoint within the next 30 days.

- If the Board also fails, members must appoint at an EGM within the next 60 days.

- Term of the first auditor, from the date of appointment until the conclusion of the first AGM.

This guide covers who appoints the first auditor of a company, the applicable time limits, and the step-by-step procedure. It also covers board resolution and consent letter formats, Form ADT-1 filing requirements, and the penalties for non-compliance.

Key Takeaways

- Under Section 139(6), the Board of Directors must appoint the first auditor of a private or non-government public company within 30 days of incorporation. If the Board fails, members must appoint at an EGM within 90 days.

- For government companies, the CAG of India appoints the first auditor within 60 days of registration under Section 139(7). If the CAG fails, the Board gets 30 days, followed by members who get 60 days at an EGM.

- As per the Companies (Audit and Auditors) Amendment Rules, 2025, filing Form ADT-1 is mandatory for all first auditor appointments effective July 14, 2025. The form must be filed within 15 days of the Board Meeting.

- Failure to appoint the first auditor within the prescribed timeline attracts penalties under Section 147, a fine of ₹25,000 to ₹5,00,000 on the company.

- Every officer in default faces a fine of ₹10,000 to ₹1,00,000 or imprisonment up to one year, or both, under Section 147 of the Companies Act, 2013.

What Does the Companies Act 2013 Say About the Appointment of First Auditor?

The appointment of the first auditor of a company is governed by Section 139 of the Companies Act, 2013. It covers who appoints the auditor, the applicable time limits, and the consequences of non-appointment.

Section 139 has two separate provisions that deal specifically with the first auditor appointment. Here is what each provision covers:

- Section 139(6): Applies to all companies other than government firms. It mandates the Board of Directors to appoint the first auditor within 30 days of incorporation.

- Section 139(7): Applies to companies in which the Central Government or one or more State Governments hold a majority stake. It also applies to companies that the Central or State Government controls indirectly through another entity. It mandates the CAG of India to appoint the first auditor within 60 days of registration.

Who is Eligible to Be Appointed as First Auditor of a Company?

Under Section 141 of the Companies Act, 2013, only a qualified professional can be appointed as an auditor of a company. This ensures that the person auditing the company’s financial statements has the necessary expertise and independence.

The following are eligible to be appointed as the first auditor:

- A practicing Chartered Accountant (CA) holding a valid certificate of practice issued by the Institute of Chartered Accountants of India (ICAI).

- A firm of Chartered Accountants where the majority of partners are practicing CAs in India.

- A Limited Liability Partnership (LLP) of Chartered Accountants, where the majority of partners are practicing CAs in India.

Note: A body corporate, an officer, or an employee of the company cannot be appointed as its auditor. Only a practicing CA or a CA firm is eligible.

Who Appoints the First Auditor of a Company?

The authority to appoint the first auditor depends on the type of company. The Companies Act, 2013, lays down a separate process for government companies and non-government companies.

1. Appointment of First Auditor in a Pvt Ltd and Non-Government Public Company

The Board of Directors appoints the first auditor of a private limited company or a non-government public company. The Board must make this appointment within 30 days of the date of incorporation.

If the Board fails to act within 30 days, the members of the company take over the responsibility. Here is how it works:

- The Board of Directors must appoint the first auditor within 30 days of incorporation.

- If the Board fails, it must immediately inform the members of the company.

- Members must then appoint the first auditor at an EGM within 90 days of being informed by the Board.

Note: The Managing Director or any individual director cannot appoint the first auditor on their own. Section 139(6) authorizes only the full Board of Directors to make this appointment. Any appointment made by an individual director alone is invalid under the Companies Act, 2013.

2. Appointment of First Auditor in a Government Company

The Comptroller and Auditor General (CAG) of India appoints the first auditor of a government company. A government company is one in which the Central Government, one or more State Governments, or both together hold 51% or more of the paid-up share capital.

If the CAG fails to act within the prescribed timeline, the appointment responsibility passes down to the Board and then to the members.

Here is how the complete chain of authority works:

- CAG of India must appoint the first auditor within 60 days from the date of registration.

- If the CAG fails, the Board of Directors must appoint within the next 30 days.

- If the Board also fails, the members must appoint at an EGM within the next 60 days.

Note: The CAG selects auditors from its own approved list of audit firms. A government company cannot directly appoint a CA firm of its own choice as the first auditor.

Private Company vs. Government Company: Who Appoints the First Auditor?

The appointment authority, governing provision, and fallback timelines differ significantly between the two types of companies.

Here is a complete side-by-side comparison:

| Particulars | Private / Non-Govt. Public Company | Government Company |

| Governing provision | Section 139(6) | Section 139(7) |

| Primary appointing authority | Board of Directors | CAG of India |

| Time limit for the primary authority | 30 days from incorporation | 60 days from registration |

| If the primary authority fails | Members at EGM within 90 days | Board of Directors within 30 days |

| If the secondary authority also fails | Not applicable | Members at EGM within 60 days |

| Can a CA firm be directly appointed? | Yes | Only through CAG empanelment |

Note: In both cases, the first auditor serves only until the first AGM. At the first AGM, the members appoint a subsequent statutory auditor who holds office for up to five consecutive years, until the conclusion of the sixth AGM.

Documents Required for Appointment of First Auditor

The following documents must be prepared and maintained before and after the appointment of the first auditor. These documents are required for the Board Meeting, the letter of appointment, and the filing of Form ADT-1 with the ROC.

| Document | Purpose |

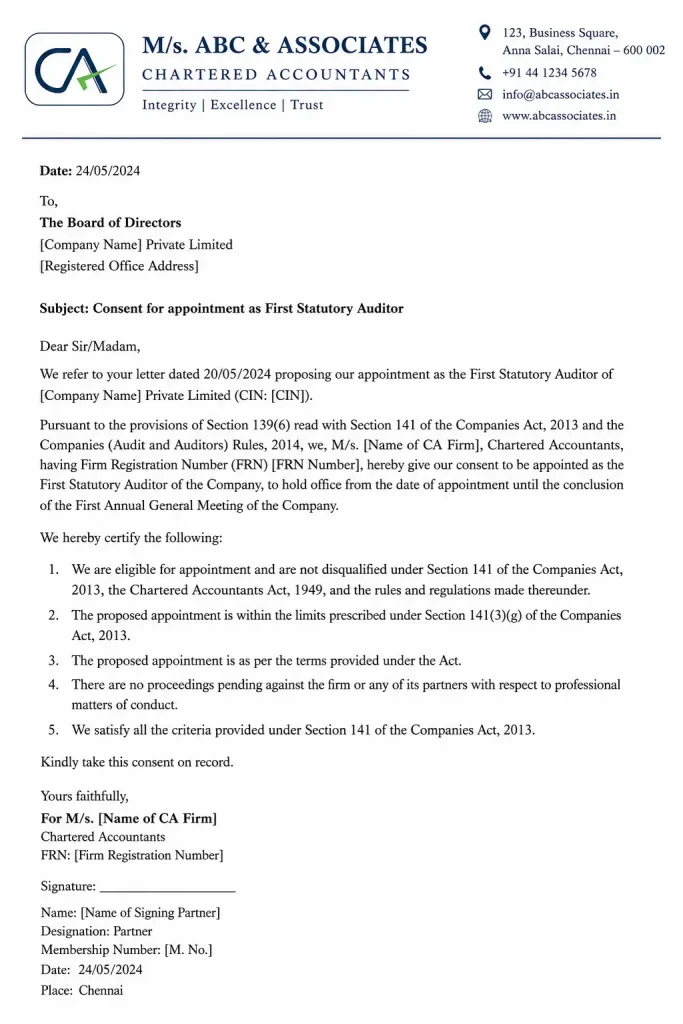

| Consent letter from the auditor | Confirms the auditor’s willingness to accept the appointment under Section 139 |

| Eligibility certificate from the auditor | Confirms the auditor is not disqualified under Section 141 |

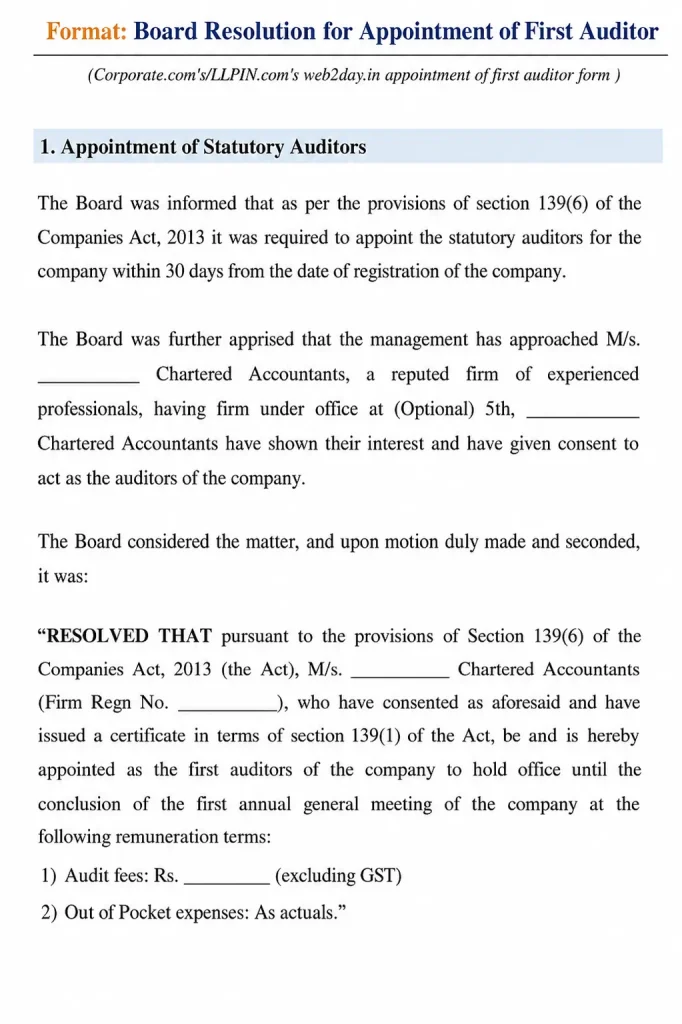

| Board Resolution | Records the formal appointment of the first auditor by the Board of Directors |

| Letter of appointment | Formally communicates the appointment to the auditor |

| Intimation letter from the company to the auditor | Informs the auditor of their appointment, required as an attachment with Form ADT-1 |

| Certified true copy of Board Resolution | Accompanies the letter of appointment issued to the auditor |

| Form ADT-1 | Filed with the ROC within 15 days of the Board Meeting to notify of the appointment |

| Digital Signature Certificate (DSC) | Required for the authorized director signing and verifying Form ADT-1 on the MCA portal |

Note: All documents submitted with Form ADT-1 must be in PDF format, digitally signed, and must not exceed 10 MB per file.

Procedure for Appointment of First Auditor of a Company

The first auditor is appointed through a set process under the Companies Act, 2013:

Step 1. Identify an Eligible Auditor

The Board of Directors must identify a practicing Chartered Accountant or CA firm. The proposed auditor must be eligible under Section 141.

Step 2. Obtain Written Consent from the Auditor

The company must obtain a written consent letter from the proposed auditor before the meeting. The letter must confirm the auditor’s willingness to accept the appointment.

Step 3. Obtain an Eligibility Certificate from the Auditor

The company must obtain a certificate from the proposed auditor confirming that:

- The auditor is not disqualified under Section 141.

- The appointment complies with all conditions prescribed under the Act.

- The appointment will not cause the auditor to exceed the prescribed limit on the number of audits.

Step 4. Issue Notice of Board Meeting

The company must issue a written notice of the Board Meeting to all directors at least 7 days in advance.

Step 5. Hold the Board Meeting and Pass a Resolution

The Board must hold the meeting within 30 days of incorporation. At this meeting, the Board must pass a resolution appointing the first auditor. The resolution must record the auditor’s name, firm registration number, and remuneration.

Step 6. Issue Letter of Appointment

The company must issue a formal letter of appointment to the auditor. The letter must be accompanied by a certified true copy of the Board Resolution.

Step 7. File Form ADT-1 with the ROC

The company must file Form ADT-1 on the MCA portal within 15 days of the Board Meeting. As per the Companies (Audit and Auditors) Amendment Rules, 2025, this filing is mandatory for all companies incorporated on or after July 14, 2025.

Note: The Board of Directors fixes the remuneration of the first auditor under Section 142(1). For subsequent auditors, remuneration is fixed at the general meeting of the members.

Form ADT-1 for Appointment of First Auditor

Form ADT-1 is a statutory return filed by a company on the MCA V3 portal with the ROC to formally notify the appointment of an auditor.

As per the Companies (Audit and Auditors) Amendment Rules, 2025, effective from July 14, 2025, filing Form ADT-1 is now mandatory for all first auditor appointments.

The company must file Form ADT-1 within 15 days of the Board Meeting in which it appoints the first auditor. The following documents must be attached:

- Certified true copy of the Board Resolution.

- Written consent letter from the auditor.

- An eligibility certificate from the auditor under Section 141.

- An intimation letter sent by the company to the auditor.

Penalty for Late Filing of Form ADT-1

Failure to file Form ADT-1 within 15 days attracts late filing fees based on the period of delay. The longer the delay, the higher the penalty:

| Period of Delay | Penalty |

| Up to 30 days | 2x the normal filing fee |

| More than 30 days and up to 60 days | 4x the normal filing fee |

| More than 60 days and up to 90 days | 6x the normal filing fee |

| More than 90 days and up to 180 days | 10x the normal filing fee |

| Beyond 180 days | 12x the normal filing fee |

Note: Companies incorporated before July 14, 2025, generally do not need to file ADT-1 retrospectively. Without a valid ADT-1 SRN, companies may face technical blocks when filing annual returns (MGT-7) or financial statements (AOC-4) later in the year.

Penalty for Non-Appointment of First Auditor

Non-appointment of the first auditor within the prescribed timeline attracts penalties under Section 147 on the company and every officer in default.

The penalties are as follows:

| Party | Penalty |

| Company | Fine of ₹25,000 to ₹5,00,000 |

| Every officer in default | Imprisonment up to 1 year or fine of ₹10,000 to ₹1,00,000 or both |

Beyond financial penalties, non-appointment of the first auditor reflects as a compliance gap on the MCA portal. Investors and lenders routinely check MCA records during funding due diligence, and a missing first auditor appointment can raise red flags and delay funding rounds.

Note: Non-appointment of the first auditor is a compoundable offence. The company can apply for compounding before the NCLT by establishing genuine reasons for the delay.

First Auditor vs. Subsequent Auditor: Key Differences

The first auditor and the subsequent auditor differ significantly in appointment authority, timing, and tenure.

Here is a quick comparison:

| Particulars | First Auditor | Subsequent Auditor |

| Governing provision | Section 139(6) / 139(7) | Section 139(1) |

| Who appoints | Board of Directors / CAG | Members at AGM |

| When appointed | Within 30 days of incorporation | At the first AGM |

| Term | Until the conclusion of the first AGM | Up to 5 consecutive AGMs |

| Form ADT-1 filing | Mandatory (w.e.f. July 14, 2025) | Mandatory within 15 days of AGM |

| Removal | By members at a general meeting | By special resolution with Central Government approval |

Note: Before July 14, 2025, filing Form ADT-1 for the first auditor appointed by the Board was optional. The Companies (Audit and Auditors) Amendment Rules, 2025, made it mandatory for all auditor appointments without exception.

Need help appointing your first auditor on time? RegisterKaro’s experts handle the entire process, from obtaining the consent letter to filing Form ADT-1, so your company stays fully compliant from day one. Contact us today for a first auditor appointment!