ITR-7 Form Filing Online in India

File ITR-7 form online for trusts, NGOs, and institutions with complete tax compliance and accuracy. Get expert guidance from RegisterKaro for quick, hassle-free filing today.

What is the ITR-7 Form?

The ITR-7 is the income tax return form prescribed by the Income Tax Department of India for filing returns of income for trusts, institutions, political parties, and other similar entities.

It is used by organizations claiming exemptions under sections of the Income Tax Act, 1961, such as:

- Section 11 – Income from property held for charitable or religious purposes

- Section 12 – Income of trusts or institutions from voluntary contributions

- Section 13 – Conditions for claiming exemption

- Section 15 – Income of political parties

- Section 25 – Income of certain companies registered as societies or trusts

- Section 30 – Income of certain funds

- Section 35 and 35AD – Deductions for scientific research and capital expenditure

- Section 44 – Income of news agencies

- Section 80G – Donations eligible for deduction

This form is designed to capture the unique financial details of these organizations, including their income from various sources and how they utilize their funds for their stated objectives. These organizations are required to file this form to maintain their tax-exempt status.

Who Must File ITR-7?

The ITR-7 form is for entities that are not individuals, HUFs, companies, or firms. It must be filed by:

- Charitable and Religious Trusts or Institutions: Entities claiming exemption under Sections 11 and 12 for income derived from property held under trust for charitable or religious purposes must file ITR-7 under Section 139(4A).

- Educational and Medical Institutions: Institutions such as schools, colleges, and hospitals claiming exemption under Section 10(23C) (specifically under sub-clauses iv, v, vi, or via) must file ITR-7 under Section 139(4C).

- Political Parties: Registered political parties whose income exceeds the maximum exemption limit (without claiming benefit under Section 11) must file ITR-7 under Section 139(4B).

- Scientific Research Associations and News Agencies: Entities registered under Section 10(21) (scientific research associations) and Section 10(22B) (news agencies) are required to file under Section 139(4C).

- Universities, Colleges, and Other Educational Institutions: Even if not covered under Section 10(23C), such institutions are required to file ITR-7 under Section 139(4D), regardless of whether they earn taxable income.

- Hospitals and Medical Institutions: Similar to educational institutions, hospitals falling under Section 10(23C)(via) must also file under Section 139(4D).

- Business Trusts: Business trusts, such as REITs (Real Estate Investment Trusts) or InvITs (Infrastructure Investment Trusts), are required to file ITR-7 under Section 139(4E).

- Investment Funds: Investment funds referred to in Section 115UB, such as Alternative Investment Funds (AIFs), must file under Section 139(4F).

Note: This form is filed electronically, and if applicable, it should be verified using a digital signature or Electronic Verification Code (EVC).

ITR-7 Changes for FY 2024-25 (AY 2025-26)

For FY 2024-25 (AY 2025-26), the ITR-7 form has undergone important updates impacting trusts, political parties, and other tax-exempt entities.

- New and Specific Disclosure Requirements: Entities are now required to provide detailed reporting on:

-

- Foreign contributions received

- Voluntary donations and accumulated income

- Utilization of funds with category-wise breakup

- Capital gains disclosures, segregated based on transfer dates as per recent Finance Act amendments

- Donor-Wise Information: Trusts and institutions claiming exemption under Section 11 must furnish donor-wise details to ensure greater transparency.

- Mandatory Audit Report Integration: Audit reports in Form 10B/10BB must be submitted electronically at least one month before the ITR-7 due date. The system will not allow filing of ITR-7 unless the audit report is already uploaded.

- Filing Deadline and Penalties: The due date for ITR-7 filing remains 31st October 2025 for entities subject to audit. Late filing will attract penalties under Section 234F.

- Pre-Filled Information: Certain fields, such as donations and exemption claims, will be pre-filled by the Income Tax Department to reduce errors and make the process easier.

- Enhanced Scrutiny: Entities, particularly those receiving foreign funds, will face stricter monitoring to ensure funds are utilised only for stated purposes.

- Compulsory Digital Verification: ITR-7 must be verified electronically using Aadhaar OTP, net banking, or other approved e-verification methods.

Objective of the Changes: These measures are aimed at strengthening compliance, improving transparency, and making the return-filing process more streamlined for exempt organisations.

Due Dates for Filing ITR-7 in India

The Income Tax Department has set specific deadlines for filing the ITR-7 form. These dates vary based on whether the accounts of the entity need to be audited or not.

Key Due Dates:

- 31st October of the financial year for entities whose accounts are required to be audited under the Income Tax Act or any other law.

- 15th September of the financial year for entities not required to get their accounts audited.

- 30th November of the financial year for entities that are required to furnish a report under Section 92E (applicable to international or specified domestic transactions).

Note: If the return is filed after the due date, late fees and interest under Sections 234F and 234A may apply.

How to File Your ITR-7 Return Online in India?

The process of filing ITR-7 is completely digital and must be done through the e-filing portal of the Income Tax Department. Here’s a step-by-step guide:

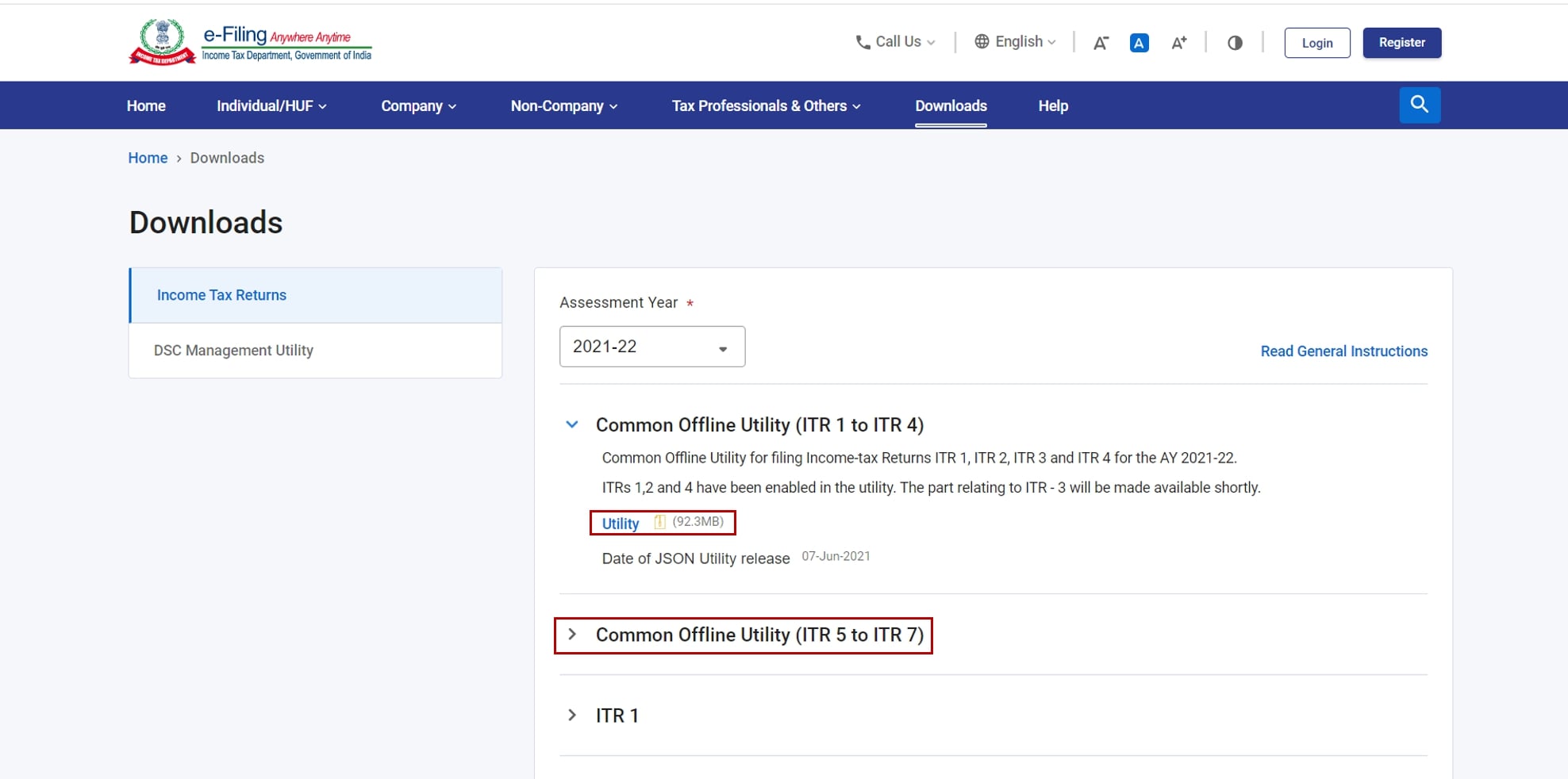

Step 1: Download the Utility

First, you need to go to the official e-filing portal (incometax.gov.in) and download the latest ITR-7 utility. This utility is an offline tool that helps you prepare your return. It's available in either Java or Excel-based ZIP format.

Step 2: Prepare the Return

Open the utility and enter all required data, such as:

- PAN and Aadhaar number

- Registration details under the Income Tax Act sections

- Income and exemption details

- Financial statements, donor list, and asset/liability info

Select applicable schedules like EI, VC (Voluntary Contributions), and others. Ensure accurate and consistent entries with supporting documents.

Step 3: Validate the Return

The utility has a 'Validate' button that checks for any common errors or inconsistencies in the data you've entered. You must validate each section to ensure the information is correct and complete.

Step 4: Generate JSON File

Once all the sections are validated, you can generate a JSON file. This file contains all the data you've entered in a format that can be uploaded to the e-filing portal.

Step 5: Upload the Return

Log in to the e-filing portal, then:

- Go to e-File → Income Tax Return → Upload Return

- Select ITR-7, AY 2025–26, and upload the JSON file

- Attach any required reports (like audit reports under Section 44AB or Section 10(23C))

Step 6: E-Verifying Your ITR-7

After filing ITR-7, it is mandatory to verify the return. You must e-Verify within 30 days of filing; otherwise, the return will be treated as invalid and incomplete. The accepted methods for verification include:

- Digital Signature Certificate (DSC): Mandatory for most trusts and political parties. Use a valid DSC registered on the e-filing portal.

- Aadhaar OTP: If the principal officer’s Aadhaar is linked with PAN, an OTP can be sent to their Aadhaar-linked mobile for quick verification.

- Electronic Verification Code (EVC): The EVC is a 10-digit alphanumeric code that can be generated using net banking, a bank account, a Demat account, or an ATM. It is valid for a limited time and must be used before the expiration date.

- Send ITR-V to CPC: If digital options fail, send a signed physical copy of ITR-V to Centralized Processing Centre (CPC) Bengaluru within 30 days. However, this method is being phased out and should be used only when no digital option is available.

Step 7: Acknowledgement (ITR-V)

After successful submission and e-verification, an acknowledgement (ITR-V) is generated. You can download this for your records. It serves as proof that your ITR-7 has been filed and verified.

Structure of the ITR-7 Form

The ITR-7 is a detailed form with multiple parts and schedules to capture all the necessary information.

Part A: General Information and Entity Details

This section contains basic information about the entity, such as its PAN, name, address, registration details, and filing status. It also includes details of the principal officer and the person responsible for filing the return.

Part B: Calculating Your Total Income and Tax Liability

Part B is divided into three main subsections:

- TI (Total Income): Contains details of gross income for the financial year (including any loss set-offs), deductions claimed, exemptions applied, and the total taxable income.

- TTI (Tax Computation): Reflects the computation of tax payable, including surcharge, cess, tax relief, any penal interest for delayed payment, taxes due, and refunds if applicable.

- Tax Details: Contains information about total tax paid through various modes like TDS (Tax Deducted at Source), TCS (Tax Collected at Source), GST, advance tax, and self-assessment tax.

Key Schedules in ITR-7

The schedules in ITR-7 are designed to provide a detailed breakdown of the entity’s finances.

- Schedule I: For taxpayers covered under Section 11(2) and Section 10(23C), mainly related to charitable or religious trusts.

- Schedule AI: For entities claiming exemptions under Sections 11, 12, or various subsections of 10(23C).

- Schedule J: For assessees registered under Sections 12A, 12AA, or subsections of 10(23C) and to report investments held by the trust or institution as of the previous fiscal year-end.

- Schedule LA: Applicable specifically to political parties for reporting income and expenses.

- Schedule ET: Relevant for electoral trusts to disclose income and donations received.

- Schedule VC (Compulsory): For reporting voluntary contributions received by the trust or institution during the year.

- Schedule K: Contains details of the founders, trustees, managers, or authors involved in the trust or institution.

- Schedule ER: For reporting revenue expenditures incurred in the course of the entity’s activities.

- Schedule EC: Captures expenses specifically related to charitable or religious purposes.

- Schedule HP: Details income earned from house property owned by the trust or institution.

- Schedule CG: Reports short-term and long-term capital gains during the financial year.

- Schedule SH: For disclosing unlisted shareholdings owned by the trust or institution.

- Schedule OS: Includes income earned under the head “Other Sources.”

- Schedule OA: Contains information related to the business or profession carried out by the entity.

- Schedule BP: For reporting gains from business or professional activities.

- Schedule CYLA: Shows income after set-off of losses from previous years or the current year.

Penalties for Missing the ITR-7 Filing Deadline

Filing your ITR-7 after the deadline can lead to several penalties. These affect both your finances and tax benefits.

Late Filing Fee Under Section 234F

If you file your return late, you must pay a fee as per Section 234F. The fee you pay for filing your ITR-7 late depends on your total income and when you file:

- If your income is ₹5 lakh or less, the maximum late fee is ₹1,000, no matter when you file after the due date.

- If your income is more than ₹5 lakh:

- File late but on or before 31st December — pay up to ₹5,000.

- File late after 31st December — pay up to ₹10,000.

Interest on Unpaid Tax Under Section 234A

If you owe tax and file late, interest is charged on the unpaid amount under Section 234A. The interest rate is 1% per month or part of a month, from the due date to the actual filing date.

Inability to Carry Forward Losses and Delayed Refunds

Late filing may prevent you from carrying forward certain losses to future years. Also, any refunds due will be delayed until the return is filed and processed.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

What is the main difference between ITR-5 and ITR-7?

−ITR-5 is for firms, LLPs, and Associations of Persons (AOPs), while ITR-7 is for charitable trusts, political parties, and other institutions claiming exemptions under specific sections of the Income Tax Act.

Is it mandatory to file an audit report before filing ITR-7?

+Can I file a revised ITR-7 if I make a mistake?

+What is a "charitable purpose" according to the Income Tax Act?

+Do I need to attach any documents when I file ITR-7 online?

+Is a Digital Signature Certificate (DSC) compulsory for filing ITR-7?

+What happens if my trust has no income in a financial year? Do I still need to file?

+How do I report foreign contributions in ITR-7?

+Can I claim deductions like 80G in ITR-7?

+What is an Updated Return (ITR-U), and can it be used for ITR-7?

+My trust runs a small business. How is that income treated in ITR-7?

+What are the rules for accumulating income under Section 11(2)?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for Your ITR-7 Filing?

Choosing the right partner for ITR-7 filing can save time, ensure accuracy, and keep your organisation fully compliant. Here’s why thousands of trusts and institutions prefer RegisterKaro:

- Expertise in Non-Profit & Institutional Filings: We specialise in ITR-7 returns for trusts, NGOs, political parties, educational institutions, and more.

- End-to-End Filing Support: From data preparation to final e-verification, we guide you through every step of the process.

- Error-Free Filing, Every Time: Our experts double-check all entries to avoid mistakes, rejections, or notices.

- On-Time Compliance: Stay ahead of due dates and avoid late fees or interest with our timely filing alerts.

- MCA and Income Tax Portal Know-How: We’re well-versed with the latest changes in the e-filing system and tax rules.

What Our Clients Say

View AllShyam Nandan Singh

Delighted to share my experience with RegisterKaro during the registration of Taglinked LLP. The end-to-end process was handled with efficiency and cl... Read more

MSM V'RESH

I had a good experience with RegisterKaro for my business compliance requirements. Their team was supportive and guided me through the registration pr... Read more

Vimal

I’m extremely satisfied with the incorporation process handled by your team. A big thank you for being available and supportive throughout. The entire... Read more

Shakti Sharma

I had an excellent experience with Bindiya from Register Karo during my company registration process. She was prompt, professional, and guided me smoo... Read more

nitin mishra

Shivansh was handling my case, and I had a great experience working with him. He was very polite, professional, and patient throughout the process. He... Read more

Sarat Shaji

Ritesh Gawri and his brilliant team helped me register my company: CultureCafe Ventures. They have been very active, responsive and responsible with t... Read more

Nishant Raman

We have found Registerkaro on google.. Me and my partner decided to go with Registerkaro for our new company registration… Trust me it was awesome exp... Read more

Gaurav Pahal

I have had nothing short of a great support from the team. Manisha Chandra has been a great person to reach out for any concerns and questions i had.... Read more

Amrendra Kumar

Incorporation of LLP through register karo experience was good, swati vasisth was my point of contact she is helpful and when ever i got any confusion... Read more

Debjit Chakraborty

I had a mixed experience at the beginning with many people calling and trying to give misleading information to take the complete payment asap, till M... Read more

Related Blogs

View All Certificate by Mobile Number")

How to Download Udyam (MSME) Certificate by Mobile Number

Difference Between Brand and Trademark in India

How to File Trademark Form TM-M: Purpose, Fees & Process

Duration of Design Protection in India: 10 to 15 Years

Design Registration Fees in India: 2026 Cost Breakdown

How to Check Design Registration Status Online in India?

How to Object to a Trademark Application in India?

How to Withdraw a Trademark Application in India?

How to Search a Trademark by Application Number on IP India?

How to Oppose a Trademark Application in India: Full Process