Change of Auditor in India

Seamlessly manage auditor change for your company with expert legal support. Stay compliant with Companies Act mandates, whether due to resignation, rotation, or during your AGM.

What is a Company Auditor and Why Would You Change One?

A company auditor is a Chartered Accountant who reviews your company’s financial records to ensure everything is accurate and legally compliant. In India, appointing a statutory auditor is required under Section 139 of the Companies Act, 2013 — a compliance obligation that begins right after your pvt ltd company registration. While the role is largely regulatory, it also brings trust and transparency to your company’s financial statements.

Sometimes, a change of auditor becomes necessary, not because of any wrongdoing, but due to evolving business needs, policy changes, or a shift in the company's direction, regardless of whether the business was established through one person company registration online or any other business structure. However, it’s important to note that the new auditor must be a Chartered Accountant in full-time practice, not just any CA.

Role of a Statutory Auditor in Your Business

The statutory auditor provides an independent opinion on your financials. Their responsibilities include:

- Reviewing and signing off on the financial statements

- Ensuring compliance with applicable laws and standards

- Identifying errors or inconsistencies in reporting

- Reporting their findings to the shareholders

An auditor holds office for five years. However, companies may change auditors earlier by following a proper process. This often takes place during the Annual General Meeting (AGM).

Note: To ensure independence and avoid potential conflicts of interest, certain companies must follow mandatory auditor rotation rules. This involves a 'cooling-off' period before the same auditor or firm can be reappointed.

Top Reasons for a Change of Auditor in India

Companies may consider replacing an auditor for various reasons, such as:

- Completion of the auditor’s term under Section 139(2)

- Resignation, death, or disqualification of the existing auditor under Section 140

- Increased audit fees or reduced satisfaction with audit quality

- Delays in submitting audit reports or a lack of responsiveness

- Business restructuring or a change in registered office location

- The need for industry-specific expertise or a different audit approach

- Internal policy decisions requiring rotation

- If a company changes its registered office to a different city or state, the existing auditor may need to resign if they cannot effectively service the new location. They would file Form ADT-3, stating the reason for their resignation.

Once the decision is made, companies must report the change of auditor in the directors' report and mention it under the Notes to Accounts in the annual financial statements.

Note: It is mandatory to notify the Registrar of Companies (ROC) of these changes: Form ADT-3 must be filed by the auditor upon resignation, and Form ADT-1 must be filed by the company to report the appointment of a new auditor.

Companies Act, 2013 on Auditor Changes

The Companies Act, 2013, sets out the legal rules for the appointment, removal, and resignation of auditors. Here's a closer look at the key sections:

1. Section 139: The Law on Auditor Appointment and Rotation

This section mainly deals with how auditors are brought on board and reappointed. It also introduces a key concept: mandatory auditor rotation for certain types of companies.

- Who it affects: This rule applies to:

-

- Companies listed on stock exchanges

- Public companies meeting specified criteria such as paid-up capital, turnover, or borrowings

- Insurance companies, banking companies, and government-controlled companies

- Rotation periods:

- An individual auditor cannot be appointed for more than one term of five years.

- An audit firm cannot be appointed for more than two terms of five years each.

- Why it's there: This rule aims to make auditors more independent and prevent them from getting too comfortable or complacent over long periods.

- How new auditors are appointed: The appointment of a new auditor is usually done at the AGM by passing a simple ordinary resolution.

2. Section 140: The Law on Auditor Removal and Resignation

Section 140 covers situations where auditors are removed or decide to step down.

- Removing an auditor mid-term:

- An auditor can only be removed before their term ends if the Central Government gives its prior approval.

- The company must pass a special resolution to remove the auditor.

- An application must be submitted to the Central Government using Form ADT-2.

- This strict process ensures auditors are not removed without a valid reason.

- Auditor resignation:

- If an auditor wishes to resign, they must inform the company and the RoC.

- They do this by submitting a statement in Form ADT-3.

- This form must be filed within 30 days of their resignation.

How to Change an Auditor in India?

The procedure for changing an auditor varies based on the specific circumstances, such as:

Scenario 1: Removal of an Auditor Before Their Term Ends

Removing an auditor before their term concludes is a detailed and controlled process.

- Board Meeting: The Board of Directors holds a meeting to approve calling an Extra-Ordinary General Meeting (EGM) for auditor removal and to request approval from the Central Government.

- Application to Central Government: The company files an application in Form ADT-2 with the Central Government (Ministry of Corporate Affairs) within 30 days of the Board Resolution, providing clear reasons for the removal.

- Central Government Approval: The Central Government reviews the application and, if satisfied with the justification, grants approval.

- Shareholder Approval (Special Resolution): After receiving Central Government approval, the company must seek shareholder approval via a Special Resolution. This can be done in two ways:

-

- At an EGM specially called for this purpose.

- As an agenda item in the next AGM.

Key points to note about the Special Resolution:

- It must be clearly stated in the meeting notice.

- Shareholders must vote in favour of the resolution.

- The resolution is passed only if the number of votes in favour is at least three times the number of votes against.

Once approved, the company can proceed with filing Form MGT-14 with the Registrar of Companies within 30 days.

- Filing with RoC: Within 30 days of passing the Special Resolution, the company files Form MGT-14 with the RoC.

- Appointment of New Auditor: The company then proceeds to appoint a new auditor to fill the casual vacancy created.

Scenario 2: When an Auditor Resigns and Creates a Casual Vacancy

When an auditor resigns, a casual vacancy is created that needs to be filled.

- Auditor's Resignation: The auditor submits a formal resignation letter to the company and files Form ADT-3 with the RoC within 30 days of their resignation.

- Board Meeting: The Board of Directors meets to acknowledge the resignation and to consider appointing a new auditor. The Board has the authority to fill the casual vacancy within 30 days of the resignation.

- Shareholder Ratification (if applicable): If the Board initially fills the casual vacancy, this appointment must be approved by the members at a general meeting convened within three months of the Board's recommendation.

- Filing with RoC: The company files Form ADT-1 with the RoC for the appointment of the new auditor within 15 days of the new auditor's appointment.

Scenario 3: Changing an Auditor at the End of Their Term (Rotation or Non-Reappointment)

This is the most frequent and straightforward method for changing an auditor.

- Board Meeting: The Board of Directors recommends either the non-reappointment of the existing auditor or the appointment of a new auditor. This recommendation is often reflected in the directors' report.

- Annual General Meeting (AGM): At the AGM, an Ordinary Resolution is passed by the shareholders for the appointment of the new auditor. This outlines the procedure for the change of auditor in an AGM.

- No-Objection Certificate (NOC): Though not legally required, it’s considered good practice for the new auditor to obtain a No-Objection Certificate (NOC) from the outgoing auditor. This confirms there are no pending issues or dues and reflects professional courtesy.

- Filing with RoC: The company files Form ADT-1 with the RoC within 15 days of the AGM, officially notifying the appointment of the new auditor.

Documents Required to Change an Auditor

The specific documents needed for a change of auditor vary depending on the scenario, but generally include:

- Board Resolution for recommending removal, appointing an auditor in a casual vacancy, or proposing a new appointment.

- Special Resolution (required if the auditor is removed before the expiry of their term).

- Ordinary Resolution (for appointing or re-appointing the auditor at the AGM).

- Application to the Central Government in Form ADT-2 (mandatory if removing an auditor before their term ends).

- Resignation Letter from the outgoing auditor.

- Form ADT-3 (filed by the resigning auditor with the Registrar of Companies).

- Consent Letter from the proposed new auditor, confirming their willingness to act.

- An Eligibility Certificate from the proposed new auditor, confirming they meet legal requirements.

- No-Objection Certificate (NOC) from the outgoing auditor (recommended as a professional practice, but not mandatory).

- Form ADT-1 (to notify the Registrar of Companies about the appointment of the new auditor).

- Form MGT-14 (required for filing special resolutions with the ROC).

These documents ensure the change is properly approved and recorded as per legal guidelines.

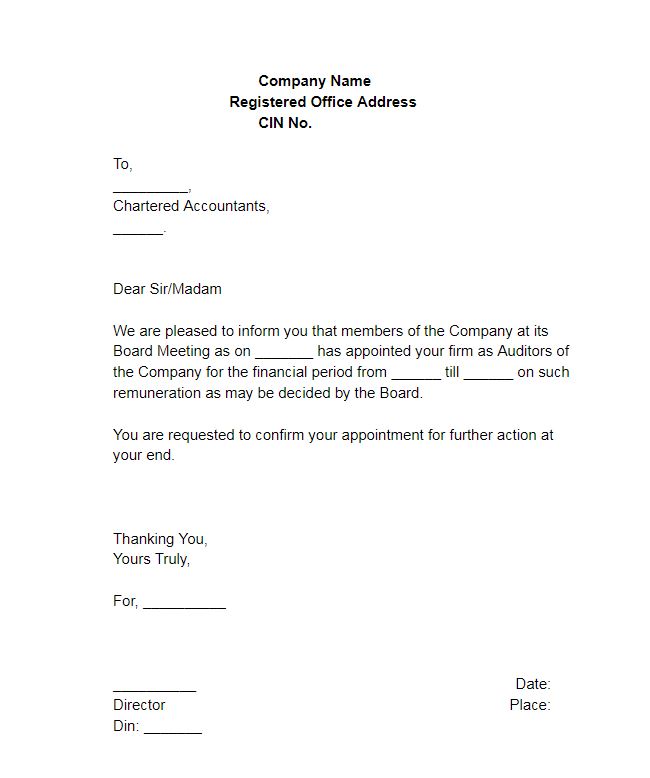

Sample Board and Special Resolution for Change of Auditor in AGM

Here are examples of resolutions passed for auditor changes, including a resolution for a change of auditor in an AGM scenario. For the letter format for a change of auditor, companies adapt these resolutions into formal communication.

Sample Board Resolution for Calling EGM for Change of Auditors (Scenario 1 - Removal)

"RESOLVED THAT according to the provisions of Section 140(1) of the Companies Act, 2013, and other applicable provisions, if any, the consent of the Board of Directors be and is hereby accorded to make an application to the Central Government for the removal of [Name of Existing Auditor/Firm], Chartered Accountants, as the Statutory Auditors of the Company before the expiry of their term.

RESOLVED FURTHER THAT a request be made to the Central Government to grant its approval for the removal of the said auditors.

RESOLVED FURTHER THAT an Extraordinary General Meeting of the members of the Company be convened on [Date] at [Time] at [Venue] to consider and, if thought fit, to pass a Special Resolution for the removal of [Name of Existing Auditor/Firm] upon obtaining the approval of the Central Government and for the appointment of new auditors."

Sample Special Resolution for Change of Auditor in AGM (Scenario 1 - Removal after CG Approval)

"RESOLVED THAT, according to the provisions of Section 140(1) of the Companies Act, 2013, and other applicable provisions, if any, and subject to the approval granted by the Central Government vide its order no. [Order No.] dated [Date], [Name of Existing Auditor/Firm], Chartered Accountants, is hereby removed from the office of the Statutory Auditors of the Company before the expiry of their term.

RESOLVED FURTHER THAT [Name of New Auditor/Firm], Chartered Accountants, having Membership/Firm Registration No. [MRN/FRN], be and is hereby appointed as the Statutory Auditors of the Company to fill the casual vacancy caused by the removal of the previous auditors, to hold office until the conclusion of the next Annual General Meeting of the Company, at such remuneration as may be mutually agreed upon between the Board of Directors and the new auditors."

Sample Ordinary Resolution for Change of Auditor in AGM (Scenario 3 - Non-Reappointment/Rotation)

"RESOLVED THAT according to the provisions of Section 139 and other applicable provisions, if any, of the Companies Act, 2013, and rules made thereunder, [Name of Existing Auditor/Firm], Chartered Accountants, be and is hereby not re-appointed as the Statutory Auditors of the Company for the financial year [mention financial year] as their term of office is concluding at this Annual General Meeting/due to mandatory rotation/for other reasons.

RESOLVED FURTHER THAT [Name of New Auditor/Firm], Chartered Accountants, having Membership/Firm Registration No. [MRN/FRN], be and is hereby appointed as the Statutory Auditors of the Company to hold office from the conclusion of this Annual General Meeting until the conclusion of the [number, e.g., fifth] consecutive Annual General Meeting, subject to ratification by members at every subsequent Annual General Meeting, at such remuneration as may be mutually agreed upon between the Board of Directors and the new auditors."

Costs Involved in Changing an Auditor

Changing an auditor in India involves two key types of expenses: government filing charges and professional service fees. The total cost depends on your company structure and the complexity of the change process.

Government Fees for ROC Filings (Form ADT-1)

Filing Form ADT-1 with the ROC is a mandatory part of the change of auditor procedure, especially when the appointment happens at the AGM. The fees are based on the company’s authorized share capital:

| Authorized Capital | ROC Filing Fee (₹) |

| Up to ₹1,00,000 | 200 |

| ₹1,00,001 to ₹5,00,000 | 300 |

| ₹5,00,001 to ₹25,00,000 | 400 |

| ₹25,00,001 to ₹1,00,00,000 | 500 |

| Above ₹1,00,00,000 | 600 |

Note: Delay in filing ADT-1 may result in late fees and penalties under the Companies Act, 2013.

Professional Fees for Auditor Change Services

You may also need help from professionals (CS/CAs/legal consultants) to handle drafting, resolutions, and ROC filings. These services may include:

- Drafting a resolution for the change of auditor in the AGM.

- Preparing a letter format for the change of auditor.

- Updating the Director’s Report and Notes to Accounts.

- Ensuring compliance with the procedure for the change of auditor in a private limited company or OPC.

Estimated professional fees range between ₹2,000 and ₹10,000 depending on:

- Type of company.

- Whether it's a tax audit or a routine change.

- Number of resolutions and forms involved.

- Urgency of work (same-day filings may cost more).

Auditor Change for Different Types of Companies

The procedure to change an auditor is similar across most companies, but can vary slightly based on the company structure and regulatory body involved.

1. Procedure for Change of Auditor in a Private Limited Company

For a private limited company, the change of auditor typically happens at the AGM. Here’s the step-by-step process:

- Hold a board meeting and approve the proposal.

- Obtain the proposed auditor’s consent and eligibility certificate as per Section 141.

- Call and hold the AGM.

- Pass an ordinary resolution for auditor appointment or removal.

- File Form ADT-1 with the ROC within 15 days.

- Update company records and the Director’s Report.

This process must follow Sections 139 and 140 of the Companies Act, 2013.

2. Procedure for Change of Auditor in One Person Company (OPC)

Since an OPC doesn’t hold an AGM, the process is slightly different:

- The board passes a resolution approving the new auditor.

- A consent and eligibility letter is obtained from the new auditor.

- File Form ADT-1 within 15 days of board approval.

- Mention the change in the next annual filing.

The process is simpler, but it must still comply with Rule 4 of the Companies (Audit and Auditors) Rules, 2014.

3. Special SEBI Regulations for Listed Companies

Listed companies must follow extra steps while changing auditors, as required by the Securities and Exchange Board of India (SEBI) under the Listing Obligations and Disclosure Requirements (LODR) Regulations, 2015. These include:

- Disclosure of auditor resignation or removal within 24 hours to the stock exchanges.

- Providing detailed reasons for the auditor's resignation.

- Appointing the new auditor only after board and audit committee approval.

- Disclosing an auditor change in the quarterly compliance report.

- Mentioning the change in the Director’s Report and Notes to Accounts.

- Filing Form ADT-1 with the Registrar of Companies (ROC) as required.

The process must be transparent and follow timelines set by SEBI and the Ministry of Corporate Affairs (MCA).

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

What is the difference between an ordinary and a special resolution for changing an auditor?

−An ordinary resolution requires a simple majority (over 50%) and is used for routine matters like appointing or re-appointing an auditor at the end of their term. A special resolution needs at least 75% approval and is required for major decisions such as removing an auditor before their term ends.

Is it mandatory to change the auditor every 5 years for a small private limited company?

+Who files Form ADT-3, the company or the auditor?

+What happens if we want to remove our auditor but the Central Government denies our application in Form ADT-2?

+Can we appoint a new auditor without getting an NOC from the old one?

+How do we fill the vacancy if our auditor resigns?

+What is the procedure for the change of auditor in an AGM?

+Do tax audit fees change when we change our auditor?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for a Change in Auditor Service?

Changing an auditor involves legal paperwork, board approvals, and filings with the ROC. RegisterKaro simplifies this process with reliable and expert support. Here's why businesses choose us:

- Experienced Legal Team: We assist with drafting board and shareholder resolutions and ensure all filings are done correctly.

- End-to-End Service: From document preparation to ROC filing, we manage the entire process.

- Timely Processing: Our team works efficiently to complete the auditor change without unnecessary delays.

- Affordable Plans: We offer clear and cost-effective pricing with no hidden charges.

- Reliable Compliance Assurance: All steps are aligned with MCA rules to reduce legal risks.

What Our Clients Say

View AllJit

Register Karo is the best platform to register your company, @kajal chowhan helped me a lot, to make the process smoothly. Thank you team registerkaro

Guru

professional work, good team work by the team allocated to us, on time delivery for incorporation of my company, Ankit followed a good workflow throug... Read more

yayati

I reached out to registerkro for company windup. Would like to give shout out to Astha gupta who was extremly helpful throughout the process. Kudos to... Read more

Vijay Azad

Hi It was pleasure to contact you@alka for company registration .Happy with the dedication and support during process and working beyond timeline...

aravind raj

We did startup registeration with their team, it was point to point approach and they were clear in those procedures and their followup is too good...

vinay kumar

Your staff Ankita Matta is a polite person the way of handling the issues was good. I hope in future register karo team handle the issues in a same wa... Read more

Riya Singh

Register karo demonstrated professionalism and expertise in navigating complex legal and regulatory issues related to our industry. Special thanks Ank... Read more

ganesh patil

Had a great experience with Register Karo. The LLP registration process was handled smoothly and everything was explained clearly. Highly recommended!

Ayush

Really impressed with the service provided by Prayansh Jindal. He handled everything efficiently and ensured that all my queries were answered promptl... Read more

Sanjeev Rai

Register karo Helped me A lot in ICEGATE Registration Process, Highly satisfied with their Service , Kind and polite staff Overall Excellent Experienc... Read more

Related Blogs

View All

Difference Between Brand and Trademark in India

How to File Trademark Form TM-M: Purpose, Fees & Process

Duration of Design Protection in India: 10 to 15 Years

Design Registration Fees in India: 2026 Cost Breakdown

How to Check Design Registration Status Online in India?

How to Object to a Trademark Application in India?

How to Withdraw a Trademark Application in India?

How to Search a Trademark by Application Number on IP India?

How to Oppose a Trademark Application in India: Full Process

")

Principles of Trademark Registration in India (2026 Guide)