Income Tax Return Filing for a Partnership Firm in India

Ensure timely and accurate ITR filing for your partnership firm with expert guidance on ITR-5, audits, capital accounts, and compliance—RegisterKaro simplifies the entire process.

What is a Partnership Firm Tax Return Filing?

Partnership firm tax return filing refers to the process of submitting the Income Tax Return (ITR-5) for a partnership firm to the Income Tax Department of India. Regardless of whether the firm is registered or unregistered, every partnership firm is required to report its income, expenses, and tax liabilities annually. The return must be filed even if the firm has incurred losses or has no taxable income during the financial year.

Filing ensures compliance with the Income Tax Act, 1961, and is essential for claiming refunds, carrying forward losses, or maintaining proper financial records. Additionally, if the firm’s turnover exceeds the specified threshold limits, tax audit provisions under Section 44AB may also apply.

These firms primarily fall into two categories:

1. Registered Partnership Firm

A registered partnership firm has completed the formal registration process with the Registrar of Firms under the Indian Partnership Act, 1932, and possesses a registration certificate as proof of its legal standing.

2. Unregistered Partnership Firm

Conversely, an unregistered partnership firm is any partnership that has not obtained a registration certificate from the Registrar of Firms.

At its core, a partnership is an agreement between two or more individuals who have mutually agreed to share the profits or losses generated from a jointly operated business. The individuals in this arrangement are known as 'partners,' and together they form the 'firm'.

Partners must understand the partnership firm tax rate and its implications for profit distribution. Partners are obligated to act in the firm's best interest, ensure fair dealings, and maintain accurate and transparent records for the benefit of all involved.

Understanding Your Partnership Firm's Tax Duties

Under the Income Tax Act, 1961:

- A partnership firm is subject to a flat tax rate of 30% on its profits.

- A 12% surcharge is levied when the firm's taxable income exceeds Rs. 1 crore.

- A 4% health and education cess is also applicable to firms.

Note: Unlike individuals or Hindu Undivided Families (HUFs), no basic exemption limit applies to partnership firms. Tax is levied on the entire taxable income.

Why must You File a Tax Return Even with No Profit (Nil Income)?

Even if a partnership firm has no profit (or even a loss) in a financial year, filing an Income Tax Return (ITR) is mandatory in India.

1. Legal Obligation: Under the Income Tax Act, 1961, every partnership firm (whether registered or unregistered) is considered a separate taxable entity and is legally obligated to file an ITR (Form ITR-5) annually, regardless of its income or loss position. Failing to do so is a non-compliance.

2. Electronic Filing Requirement: Form ITR-5 must be filed electronically through the Income Tax e-filing portal. If the firm is subject to a tax audit, filing must be done using a Digital Signature Certificate (DSC).

3. Carry Forward of Losses: This is a crucial benefit. If your firm incurs a loss in a financial year, you can only carry forward these losses to offset against future profits and reduce your tax liability in subsequent years if you file your ITR by the due date. If you don't file, you lose the ability to carry forward most types of losses (e.g., business loss, capital loss).

Example: Suppose your partnership firm reports a business loss of Rs. 2.5 lakhs in FY 2024–25. If you file your ITR on time, you can carry forward this Rs. 2.5 lakhs and adjust it against future profits in the next 8 years, reducing future tax burdens. However, if you fail to file the return, you lose this right, and the entire loss lapses.

4. Avoid Penalties and Consequences:

- Late Filing Fees: Even for a NIL return, a late filing fee of Rs. 5,000 is levied under Section 234F. However, if the firm's total income is Rs. 5 lakh or less, the fee is reduced to Rs. 1,000.

- Interest: If any tax was due (even if calculated to be zero after deductions but before filing), interest under Section 234A might be charged.

- Prosecution: In severe cases of non-compliance, particularly if there's a history of not filing, which could be viewed as tax evasion, or if the tax liability (even if unpaid) was substantial, the firm and its partners could face prosecution.

- Operational and Reputational Impact: Not filing can lead to a negative standing with tax authorities, potentially affecting other aspects of the firm's operations.

5. Proof of Financial History: ITRs serve as official proof of the firm's financial activities. This is invaluable for:

- Loan Applications: Banks and financial institutions often require ITRs for the past few years when applying for business loans, overdraft facilities, or even personal loans for partners.

- Visa Applications: When partners apply for international visas, embassies often request ITRs as proof of financial stability.

- Tender Applications: For bidding on government or private tenders, consistent ITR filing demonstrates compliance and financial transparency.

6. Claiming Refunds: If the firm had any Tax Deducted at Source (TDS) on its income (e.g., on interest received, or payments from clients), even if no final tax was payable, you can only claim a refund of this TDS by filing the ITR.

7. Maintaining Records and Transparency: Filing the ITR ensures that the firm maintains accurate financial records, which are essential for good governance, internal transparency among partners, and future financial analysis.

Which ITR Form to Use for a Partnership Firm?

ITR-5 is used by most partnership firms. Non-LLP firms under presumptive taxation can use ITR-4 if the income is within Rs. 50 lakh, and an audit isn’t required.

Regardless of profit or loss, filing the ITR is legally mandatory for a partnership firm, usually via ITR-5, to fulfill compliance, carry forward losses, and avoid penalties.

ITR-5: Main form for partnership firms

ITR-5 is the primary Income Tax Return form mandated for most partnership firms in India. This form is specifically designed for entities such as:

- Partnership Firms (both registered and unregistered)

- Limited Liability Partnerships (LLPs)

- Association of Persons (AOPs)

- Body of Individuals (BOIs)

- Artificial Juridical Persons (AJPs)

- Cooperative Societies

- Local Authorities

- Estates of deceased persons or insolvents

- Business Trusts and Investment Funds

It is crucial to note that ITR-5 is for the firm itself and not for the individual partners. The firm is required to file ITR-5 electronically, and if the firm is subject to an audit, a Digital Signature Certificate (DSC) is mandatory for verification.

When can a Partnership Firm use ITR-4 (Sugam)?

A partnership firm (excluding LLPs) can file ITR-4 (Sugam) only if it opts for the presumptive taxation scheme, which is entirely optional. To be eligible, the firm must meet the following conditions:

- Presumptive Taxation: The firm must opt for the presumptive taxation scheme under Section 44AD (for eligible businesses), Section 44ADA (for eligible professionals), or Section 44AE (for those engaged in the business of plying, hiring, or leasing goods carriages).

- Total Income Limit: The firm's total income should not exceed Rs. 50 Lakh during the financial year.

- No Audit Requirement: Generally, firms opting for presumptive taxation under ITR-4 are not required to maintain detailed books of accounts or get their accounts audited, provided they declare income at the prescribed presumptive rates. However, if their actual income is lower than the presumptive income and they wish to declare the lower income, they would need to maintain books of accounts and get them audited, which would then make them ineligible for ITR-4 and require ITR-5.

- No Complex Income: The firm should not have income from sources like capital gains (with minor exceptions for certain LTCG up to Rs. 1.25 lakhs under Section 112A with no brought-forward losses), more than one house property, lottery winnings, or foreign assets.

Firms must carefully assess eligibility before opting for ITR-4. Incorrect filing can lead to compliance issues and penalties.

Due Dates for Filing Partnership Tax Return (AY 2025-26)

Filing the Income Tax Return (ITR) on time is crucial for partnership firms to remain compliant, avoid penalties, and avail benefits like carry forward of losses. The due dates vary based on whether the firm is subject to audit or transfer pricing provisions.

| Category of Partnership Firm | Due Date for Filing Income Tax Return (ITR-5) | Due Date for Filing Tax Audit Report (if applicable) |

| Not required to be audited | September 15, 2025 | Not applicable |

| Required to be audited | October 31, 2025 | September 30, 2025 |

| Requiring Transfer Pricing Report (Form 3CEB under Section 92E) | November 30, 2025 | October 31, 2025 |

| Belated/Revised Return | December 31, 2025 | - |

| Updated Return (ITR-U) | March 31, 2030 | - |

Notes:

- The original due date for non-audit cases was July 31, 2025, which has been extended to September 15, 2025, by the CBDT.

- The Financial Year (FY) for AY 2025-26 is April 1, 2024, to March 31, 2025.

- Failing to file the return by the due date may attract penalties and interest under the Income Tax Act, 1961.

- These dates are subject to change if the CBDT issues an extension. Always verify the current deadlines on the official portal.

What Happens If You Don’t File Your Partnership ITR?

Failing to file your Income Tax Return (ITR) can lead to several severe consequences, including penalties, interest, and legal action.

Here are the key repercussions you might face:

| Consequence | Details |

| Penalty for Late Filing (Section 234F) |

|

| Interest on Late Payment (Section 234A) | A charge of 1% per month, or part of a month, is levied on the unpaid tax amount. |

| Loss of Carry Forward of Losses | You will lose the ability to carry forward losses under the 'Capital Gains' and business income heads to subsequent years, preventing future tax offsets. |

| Prosecution and Legal Action | Imprisonment can range from three months to two years, in addition to fines. For cases of tax evasion exceeding Rs. 25 lakhs, the imprisonment term can extend from six months to seven years. |

| Penalty for Concealment of Income (Section 270A) | If tax authorities determine you have concealed income or provided inaccurate information, a penalty ranging from 50% to 200% of the tax evaded may be imposed. |

What to do if ITR Filing is Missed?

If you're concerned about missing the ITR filing deadline, there are still avenues to submit your return:

Belated Return

- If you miss the ITR filing due date, you can file a return after the due date, called a belated return.

- However, filing a belated return means you will be subject to a late fee and interest charges. Additionally, you will forfeit the ability to carry forward any losses for future adjustments.

- Despite this, you are still permitted to claim applicable deductions and exemptions.

- The final date for filing a belated return is December 31st of the relevant assessment year (unless an extension is officially granted by the government).

Updated Return

Even if you miss the December 31st deadline, you may still have the option to file an updated return (ITR-U), provided you meet specific conditions.

What is the Cost of Filing a Partnership Tax Return?

The cost of filing a Partnership Tax Return in India involves both government-mandated taxes and potential late fees, as well as professional charges if you opt for expert assistance.

A. Government Fees and Late Payment Charges

Filing a partnership tax return (ITR-5) in India itself does not involve a direct "government fee" for the act of filing if done within the due date. The government charges are related to the tax liability of the firm and penalties/interest if the filing or payment is delayed.

Tax Liability: Partnership firms are taxed at a flat rate of 30% on their taxable income. A surcharge of 12% applies if the taxable income exceeds Rs. 1 crore. Additionally, a 4% Health and Education Cess is levied on the total tax amount (including surcharge). Partnership firms are also subject to Alternative Minimum Tax (AMT) at 18.5% of adjusted total income.

Alternative Minimum Tax (AMT):

- AMT is charged at 18.5% of adjusted total income.

- Applicability: AMT applies only if the firm claims deductions under:

- Chapter VI-A (Sections 80-IA to 80RRB, excluding 80P)

- Section 10AA (for SEZ units)

- AMT does not apply to every firm, especially those not claiming such deductions.

Late Filing Fee (Section 234F):

- If the return is filed after the due date but on or before December 31st of the assessment year, a late fee of Rs. 5,000 is applicable.

- If the total income of the partnership firm is Rs. 5 lakh or less, the late fee is capped at Rs. 1,000.

Interest on Late Payment (Section 234A): If there is any unpaid tax amount, interest at a rate of 1% per month or part of a month is charged on the unpaid tax from the due date until the payment is made.

B. Professional Fees for Filing Your ITR

The cost of filing a partnership tax return through a professional (like a Chartered Accountant service or an online tax filing platform) can vary significantly based on the complexity of the firm's financial transactions, turnover, and whether a tax audit is required.

Online Platforms: Basic partnership firm filing services on online platforms might start from around Rs. 4,000 - Rs. 6,000, especially for firms not requiring a tax audit.

Chartered Accountants (CAs): CA fees are generally higher due to personalized service, detailed advice, and handling of complex scenarios.

- For a standard partnership firm ITR filing without an audit, fees could range from Rs. 5,000 to Rs. 10,000 or more.

- If a tax audit is mandatory (e.g., if the firm's turnover exceeds Rs. 1 crore for businesses or Rs. 50 lakh for professionals), the professional fees will be substantially higher, as it involves a detailed examination of accounts and preparation of the Tax Audit Report (Form 3CD). These charges can range from Rs. 15,000 to Rs. 50,000 or even more, depending on the turnover and complexity of the books.

Factors Influencing Fees

The fees charged by Chartered Accountants (CAs) or accounting professionals can vary significantly based on multiple factors. Understanding these variables can help businesses and professionals better estimate their accounting costs and choose the right service provider.

- Turnover/Gross Receipts: Higher turnover generally means more complex accounting and higher fees.

- Number of Transactions: A large volume of transactions can increase the effort required.

- Nature of Business/Profession: Certain industries or professions might have specific compliance requirements.

- Maintenance of Books of Accounts: If the books are not well-maintained, the CA might charge more for reconciliation and preparation.

- Additional Services: Fees may increase if the firm requires other services like GST compliance, TDS compliance, advisory, or balance sheet preparation.

Documents Needed for Filing Partnership ITR

Filing the Income Tax Return (ITR-5) for a partnership firm requires a comprehensive set of documents to ensure accurate reporting of income, expenses, and tax liabilities.

Regardless of whether your firm's accounts are audited or not, the following documents are crucial for ITR filing:

1. Foundational Documents

These documents show that your partnership firm is officially set up and running. They help identify your firm and make sure it’s eligible for tax filing.

- Partnership Deed: Outlining profit-sharing ratio, roles, and responsibilities of partners

- Partnership Firm Registration Certificate (if registered)

- Udyam Registration Certificate (for MSME classification, if applicable)

- GST Registration Certificate (if the firm is registered under GST)

- ROC Compliance Proof (only if filed mistakenly as LLP; applicable for LLPs, not regular partnership firms)

2. Financial Statements (for the relevant financial year)

These show the financial health of your business during the year.

- Profit & Loss Account: Detailing income and expenses incurred

- Balance Sheet (as of March 31st): Showing assets, liabilities, capital, and current financial position

- Trading Account: For firms involved in the purchase and sale of goods

3. Banking and Accounting Records

These help verify business transactions and support your financial statements.

- Bank Statements: All bank accounts operated by the firm during the year

- Ledger Accounts: Including:

- All heads of income and expenses

- Partners’ capital accounts and drawings

- Loans and advances

- Debtors and creditors

4. Tax-Related Documents

Used to match your tax payments and deductions with government records.

- TDS Certificates (Form 16A, Form 26Q, etc.):

- If TDS is deducted on income received (like professional fees or interest)

- If the firm has deducted TDS on payments made

- Form 26AS / AIS / TIS:

- Consolidated summary of tax deducted, collected, and high-value transactions

- Should be reconciled with the firm’s books

5. Supporting Documents

These add more clarity to the numbers you report in your return.

- Details of Capital Contributions and Drawings: Records of capital introduced and withdrawals by each partner.

- Loan Documents: Details and interest statements for any loans taken or given during the year.

- GST Returns (if applicable): GSTR-1, GSTR-3B, GSTR-9 to match turnover and tax liabilities with ITR.

- Investment Proofs: Details of any investments made by the firm in the financial year.

Additional Documents if Your Firm's Accounts Are Audited

If your partnership firm's turnover or gross receipts exceed the prescribed limits (currently Rs. 1 crore for businesses or Rs. 50 lakh for professionals, with increased limits for certain cash transactions), a tax audit under Section 44AB is mandatory.

1. Tax Audit Report (Form 3CB and Form 3CD): This report is prepared and certified by a Chartered Accountant.

- Form 3CB: The audit report itself.

- Form 3CD: A statement of particulars that contains detailed information about the firm's financial activities, compliance with various tax provisions, and disallowances.

2. Detailed Books of Accounts: The auditor will require comprehensive books of accounts, including:

- Cash Book

- Bank Book

- Sales Register

- Purchase Register

- Journal entries

- Ledgers

- Inventory records

- Fixed Asset Register

3. Vouchers and Bills: All original invoices, bills, payment vouchers, and receipts supporting the firm's income and expenses.

4. Trial Balance: A summary of all ledger balances, used to prepare the final financial statements.

While not directly uploaded with the ITR, these documents are fundamental for the firm's existence and tax compliance:

Partnership Deed: This legal document outlines the terms and conditions of the partnership, including profit/loss sharing ratios, roles and responsibilities of partners, interest on capital/drawings, and remuneration to partners.

It serves as the governing document and is crucial for calculating partners' remuneration and interest on capital as per the Income Tax Act. It's often required by professionals to understand the firm's structure and valid deductions.

PAN Card of the Partnership Firm: The Permanent Account Number (PAN) is a unique 10-digit alphanumeric identifier issued by the Income Tax Department. The firm needs to conduct any financial transaction, including opening bank accounts, and it is the primary identification for filing its ITR.

PAN and Aadhaar of all Partners: While the ITR is filed for the firm, the details of all partners, including their PAN and Aadhaar numbers, are required in the ITR-5 form.

How to File a Partnership Tax Return Online in India?

Filing a Partnership Tax Return (ITR-5) online is mandatory for most partnership firms in India. The process primarily involves preparing your financial data, logging into the Income Tax Department's e-filing portal, filling out the ITR-5 form, and then verifying it.

Here's a step-by-step guide on how to file a Partnership Tax Return online:

1. Log in to the Income Tax e-Filing Portal

- Go to the official Income Tax Department e-filing portal: incometax.gov.in

- Login: Use the firm's PAN as the user ID and enter the password. If you're a new user, you'll need to register first.

2. Navigate to "e-File" and select ITR Form

- After logging in, go to the "e-File" menu.

- Select "Income Tax Returns" and then "File Income Tax Return."

- Select Assessment Year (AY): Choose the relevant Assessment Year (e.g., AY 2025-26 for income earned in FY 2024-25).

- Select Filing Mode: Choose "Online."

- Select ITR Form: Select "ITR-5." This is the form specifically for partnership firms (and LLPs, AOPs, BOIs, etc.).

3. Fill in the ITR-5 Form Online

The ITR-5 form is comprehensive and consists of various parts and schedules. You'll need to fill in the details carefully. The system may pre-fill some information based on your PAN and other data available with the Income Tax Department (e.g., from Form 26AS/AIS/TIS).

- Part A: General Information: Basic details of the firm, nature of business, audit information (if applicable), date of formation, etc.

- Part A-BS: Balance Sheet: Details of assets, liabilities, and partners' capital as of March 31st of the financial year.

- Part A-P&L: Profit & Loss Account: Revenue from operations, expenses, and net profit/loss for the financial year.

- Part A-OI: Other Information: Details of quantitative particulars, method of accounting, and other relevant information.

- Schedules: These are detailed sections for various types of income, deductions, and tax computations:

- Schedule HP: Income from House Property.

- Schedule BP: Computation of Income from Business or Profession (this is a very important schedule for firms).

- Schedule CG: Capital Gains.

- Schedule OS: Income from Other Sources (e.g., interest income).

- Schedule CYLA: Set-off of current year losses.

- Schedule BFLA: Set-off of unabsorbed losses brought forward from previous years.

- Schedule DPM: Depreciation on Plant and Machinery.

- Schedule DOA: Depreciation on Other Assets.

- Schedule DCG: Deemed Capital Gains on sale of depreciable assets.

- Schedule UD: Unabsorbed Depreciation.

- Schedule CFL: Carry Forward of Losses.

- Schedule 80G, 80GGA, etc.: For various deductions under Chapter VIA.

- Schedule AMT: Computation of Alternate Minimum Tax (AMT) payable under Section 115JC.

- Schedule AMTC: Computation of tax credit under Section 115JD.

- Schedule SI: Statement of income taxable at special rates.

- Schedule IF: Information regarding partnership firms in which the firm is a partner (if applicable).

- Schedule PTI: Pass-Through Income details from business trusts or investment funds.

- Part B-TI: Computation of Total Income.

- Part B-TTI: Computation of Tax Liability on Total Income.

- Tax Payments: Details of Advance Tax, Self-Assessment Tax, and TDS/TCS.

- Verification: Declaration and verification section.

4. Review and Validate

- After filling in all the required details, carefully review all the information entered to avoid errors.

- The e-filing portal has a "Validate" option. Click on this to check for any missing mandatory fields or calculation errors. Correct any errors highlighted by the system.

5. Verification of the Return

Once the form is filled and validated, you need to verify the return. There are generally two primary ways for partnership firms to verify ITR-5:

Using Digital Signature Certificate (DSC):

- This is the mandatory method for firms whose accounts are liable to audit under Section 44AB.

- Ensure that the DSC of the designated partner (or authorized signatory) is registered and updated on the e-filing portal.

- Attach the DSC when prompted during the submission process.

Electronic Verification Code (EVC):

- If the firm is not liable for the audit, you might have the option to verify using EVC.

- EVC can be generated through various methods like Aadhaar OTP, Net Banking, Bank Account EVC, or Demat Account EVC.

- A code will be sent to the registered mobile number/email, which you need to enter to complete the verification.

6. Submit the Return

- Once the return is verified, click "Submit."

- Upon successful submission, an acknowledgement (ITR-V) will be generated.

- Download and save this ITR-V for your records. If you verified using DSC, your filing is complete.

7. Send ITR-V (if EVC was chosen and not completed online)

If you chose EVC but could not complete it online (or if you choose the "send ITR-V via post" option), you will need to print two copies of the ITR-V, sign one copy, and send it by ordinary post to:

- Centralized Processing Centre, Income Tax Department, Bengaluru – 560500, Karnataka.

This must be done within 30 days of filing the return. The other copy should be retained for your records. If the ITR-V is not received by CPC within 30 days, the return will be treated as not filed.

How to Verify Your Return without a DSC?

While a Digital Signature Certificate (DSC) is often mandatory for companies and firms whose accounts are liable for audit under Section 44AB, there are several methods to verify your Income Tax Return (ITR) without a DSC, especially for individuals and those not falling under mandatory audit requirements.

Here are the common ways to verify your ITR online without a DSC:

1. Aadhaar OTP

This is one of the most popular and easiest ways to e-verify your ITR. Your PAN must be linked with your Aadhaar, and your mobile number must be registered with Aadhaar.

Process:

- On the e-filing portal, select the option to "e-Verify" your return.

- Choose "I would like to verify using OTP on a mobile number registered with Aadhaar."

- Agree to validate your Aadhaar details and click "Generate Aadhaar OTP."

- A 6-digit OTP will be sent to the mobile number registered with your Aadhaar.

- Enter the OTP on the portal within the stipulated time (usually 15 minutes).

- Click "Validate."

2. Electronic Verification Code (EVC) through Pre-validated Bank Account

You can generate an EVC if your bank account is pre-validated and EVC-enabled on the e-filing portal.

Your bank account must be pre-validated on the e-filing portal. This means your PAN should be linked to your bank account, and the bank details should be verified by the Income Tax Department.

Process:

- On the e-filing portal, select the option to "e-Verify" your return.

- Choose "Through Bank Account" to generate EVC.

- An EVC will be sent to your mobile number and email ID registered with your pre-validated and EVC-enabled bank account.

- Enter the received EVC on the e-filing portal.

3. Electronic Verification Code (EVC) through Pre-validated Demat Account

Similar to a bank account, you can use your Demat account to generate EVC. Your Demat account must be pre-validated and EVC-enabled on the e-filing portal. Your PAN should be linked to your Demat account.

Process:

- On the e-filing portal, select the option to "e-Verify" your return.

- Choose "Through Demat Account" to generate EVC.

- An EVC will be sent to your mobile number and email ID registered with your pre-validated and EVC-enabled Demat account.

- Enter the received EVC on the e-filing portal.

4. Net Banking

Many banks provide a direct link to the Income Tax e-filing portal through their net banking facility. You must have an active net banking facility with a bank that has this service integrated with the Income Tax Department. Your PAN must be linked to your bank account.

Process:

- Log in to your net banking account.

- Look for the "e-Verify Tax" or "Income Tax e-Filing" option.

- You will be redirected to the Income Tax e-filing portal.

- Once redirected, you can proceed to e-verify your pending ITR directly without needing to log in separately on the IT portal.

5. Electronic Verification Code (EVC) through Bank ATM (Offline Method)

This is an offline method to generate an EVC, which can then be used online. This facility is available only for select banks. Your PAN must be registered with the bank, and your mobile number must be registered with the e-filing portal.

Process:

- Visit an ATM of your bank (if it supports this facility).

- Swipe your ATM card and enter your PIN.

- Select "Generate EVC for Income Tax Filing."

- An EVC will be sent to your mobile number and email ID registered with the e-filing portal.

- Log in to the e-filing portal, select "I already have an Electronic Verification Code (EVC)," enter the received EVC, and click "e-Verify."

6. Sending a Signed Physical Copy of ITR-V (Acknowledgement)

If you are unable to use any of the online e-verification methods, you still have the traditional offline option.

Process:

After successfully submitting your ITR online, download the ITR-V (Acknowledgement) form.

- Print two copies of the ITR-V.

- Sign one copy in blue ink.

- Send the signed ITR-V by ordinary post (not speed post or courier) to: Centralized Processing Centre, Income Tax Department, Bengaluru – 560500, Karnataka.

- You must send this within 30 days of filing your ITR.

- Keep the other unsigned copy of ITR-V for your records.

Deductions and Allowances for Partnership Firms

Partnership firms can claim various deductions and allowances to reduce their taxable income. However, specific rules and limits apply, especially concerning payments to partners.

Salary and Interest Paid to Partners: How Much Can You Claim?

The Income Tax Act, 1961, particularly Section 40(b), governs the deductibility of remuneration (salary, bonus, commission, or any other form of remuneration) and interest paid to partners by a partnership firm.

Conditions for Deductibility:

- Partnership Deed: The payment of remuneration and interest must be explicitly authorized by the partnership deed. The deed must specify the amount or the method of calculating these payments.

- Working Partner: Remuneration is deductible only if paid to a working partner, i.e., a partner actively engaged in conducting the affairs of the business or profession of the firm. Remuneration to non-working partners is not deductible.

- Relates to Previous Year: The payment must pertain to the previous year for which the return is being filed.

Limits on Deductions (as per Section 40(b)):

The deduction for remuneration to working partners is subject to the following limits on "book profit":

- On the first Rs. 6,00,000 of book profit (or in case of a loss): Maximum deduction allowed is Rs. 3,00,000 or 90% of book profit, whichever is higher. (Earlier, the limit was Rs. 1,50,000; this change applies from AY 2025–26.)

- On the balance of book profit (exceeding Rs. 6,00,000): The maximum deduction allowed is 60% of such balance book profit.

Book Profit Calculation: "Book profit" for this purpose is calculated by adding back any remuneration paid to partners to the net profit of the firm (before allowing for such remuneration).

Interest on Capital Paid to Partners:

- Interest paid to any partner (working or non-working) on capital contributed to the firm is deductible, but it is capped at a maximum rate of 12% per annum simple interest. Any interest paid above this rate will be disallowed.

Other Business Expenses Deductible From Profit

Beyond payments to partners, a partnership firm can claim deductions for various legitimate business expenses, similar to other businesses. These deductions are primarily governed by Sections 30 to 37 of the Income Tax Act.

- Rent, Rates, Taxes, Repairs, and Insurance for Business Premises: Expenses related to the building used for business purposes.

- Repairs and Insurance of Machinery, Plant, and Furniture: Current repairs and insurance premiums paid for assets used in the business.

- Depreciation: A deduction for the wear and tear of assets like buildings, machinery, plant, and furniture used for business purposes. Depreciation rates are prescribed by the Income Tax Rules.

- Salaries, Wages, Bonuses, and Commissions to Employees: Payments made to employees for services rendered.

- Interest on Business Loans: Interest paid on capital borrowed for the business or profession.

- Legal and Professional Fees: Fees paid to lawyers, accountants, consultants, etc., for services related to the business.

- Advertisement Expenses: Costs incurred for advertising products or services.

- Travelling Expenses: Expenses incurred for business-related travel.

- Communication Expenses: Telephone, internet, postage, etc.

- Electricity and Water Bills: Utility expenses for the business premises.

- Office Expenses: Stationery, printing, sundry expenses, etc.

- Bad Debts: Debts that have become irrecoverable.

- Scientific Research Expenditure: Certain expenditures incurred on scientific research.

- Amortization of Preliminary Expenses: Certain specified expenses incurred before the commencement of business can be amortized over five years.

General Conditions for Deductibility (Section 37(1)):

Any expenditure (not being capital expenditure or personal expenses of the assessee) that is laid out or expended wholly and exclusively for the business or profession is generally allowed as a deduction. However, certain expenses are specifically disallowed (e.g., expenses incurred for any purpose that is an offense or prohibited by law, or expenditure on CSR activities).

What is the Alternate Minimum Tax (AMT) for Partnership Firms?

The Alternate Minimum Tax (AMT) is a provision in the Income Tax Act (Section 115JC) designed to ensure that taxpayers, including partnership firms, who claim significant deductions or exemptions, still pay a minimum amount of tax. This prevents firms with substantial income from reducing their tax liability to nil or a very low amount due to various incentives.

Applicability:

AMT provisions apply to partnership firms (and LLPs, individuals, HUFs, AOPs, BOIs) if they claim deductions under certain sections of the Income Tax Act, specifically:

- Deductions under Chapter VI-A (e.g., Section 80G, 80GGA, but excluding Section 80P for cooperative societies).

- Deduction under Section 10AA (for units in Special Economic Zones - SEZ).

- Deduction under Section 35AD (for specified business ventures).

Threshold for Applicability: AMT applies only if the "adjusted total income" of the partnership firm exceeds Rs. 20 lakh.

Computation of AMT:

- Compute Normal Tax Liability: First, calculate the income tax payable by the firm as per the regular provisions of the Income Tax Act (flat 30% tax + surcharge + cess).

- Compute Adjusted Total Income (ATI): This is calculated by taking the firm's total income (computed as per normal provisions) and adding back the deductions claimed under the specific sections mentioned above (e.g., Chapter VI-A, 10AA, 35AD).

- Calculate AMT: AMT is levied at the rate of 18.5% (plus applicable surcharge and Health & Education Cess) on the Adjusted Total Income.

- Compare and Pay Higher: The firm is liable to pay the higher of:

- The normal tax liability.

- The AMT is calculated on the adjusted total income.

AMT Credit: If a firm pays AMT (i.e., the AMT liability is higher than the normal tax liability), the difference between the AMT paid and the normal tax liability can be carried forward as an AMT credit. This credit can be set off against the normal tax liability in subsequent years (up to 15 assessment years) when the normal tax payable exceeds the AMT in those years. This ensures that the firm does not pay tax twice on the same income.

Tax Audit for Partnership Firms

A tax audit is a detailed examination of a business's accounts and financial records by a Chartered Accountant. For partnership firms in India, it's crucial to understand when a tax audit becomes mandatory.

When is a Tax Audit Compulsory for a Partnership Firm?

A tax audit is compulsory for a partnership firm under Section 44AB of the Income Tax Act, 1961, if its:

- Total sales, turnover, or gross receipts in the business exceed Rs. 1 crore in the financial year.

- Gross receipts in the profession exceed Rs. 50 lakh in the financial year.

Note: There is a higher threshold of Rs. 10 crore for businesses if the cash transactions are less than 5% of the total receipts and payments.

Understanding the Tax Audit Limit for Your Business

Businesses: If your partnership firm is involved in business activities, the key factor is your turnover or gross receipts. If this exceeds Rs. 1 crore (or Rs. 10 crore under specific conditions related to cash transactions), a tax audit is mandatory.

Professionals: If your partnership firm is engaged in a profession (e.g., legal, medical, engineering, architecture, accountancy, technical consultancy, interior decoration), the threshold is based on your gross receipts. If these exceed Rs. 50 lakh, a tax audit is required.

Example:

- A trading firm with a turnover of Rs. 1.2 crore needs a tax audit.

- A law firm with gross receipts of Rs. 60 lakh needs a tax audit.

- A small manufacturing unit with a turnover of Rs. 90 lakh does not need a tax audit unless its cash transactions exceed the specified limit.

What Happens During a Tax Audit?

During a tax audit, a Chartered Accountant (CA) examines the firm's books of accounts and financial records to ensure compliance with the Income Tax Act. The CA will:

- Verify the correctness and completeness of the books of accounts.

- Check for compliance with various provisions of the Income Tax Act.

- Report any discrepancies or observations.

- Prepare a Tax Audit Report in the prescribed forms (Form 3CA/3CB and Form 3CD).

Key Activities During a Tax Audit

- Verification of Transactions: The CA will verify a sample of transactions to ensure they are properly recorded and supported by evidence.

- Examination of Financial Statements: The Profit & Loss Account, Balance Sheet, and other financial statements will be reviewed for accuracy and compliance with accounting standards.

- Checking Compliance: The CA will check if the firm has complied with various tax laws, such as TDS provisions, and has correctly claimed deductions and allowances.

- Reporting: The CA will report any observations or discrepancies noted during the audit in the Tax Audit Report. This report is then submitted to the Income Tax Department.

Tax Audit Report (Form 3CA/3CB and 3CD)

When a partnership firm is liable for a tax audit under Section 44AB of the Income Tax Act, it must submit a Tax Audit Report comprising Form 3CA or 3CB along with Form 3CD, depending on the nature of its audit obligations.

- Form 3CA: It is used when the firm is already subject to an audit under any other law, such as a statutory audit under the Companies Act or any other regulatory framework. It summarizes the Chartered Accountant’s (CA’s) opinion on the financial statements audited under that law.

- Form 3CB: This is used when the firm is not required to be audited under any other law. In such cases, the CA conducts an independent audit specifically for tax purposes and reports its findings in this form.

- Form 3CD: It is a detailed annexure submitted along with either Form 3CA or 3CB. It provides a comprehensive breakdown of the firm’s financial particulars, including turnover, various expenses, deductions claimed, compliance with tax provisions, and any notable observations or qualifications made by the auditor.

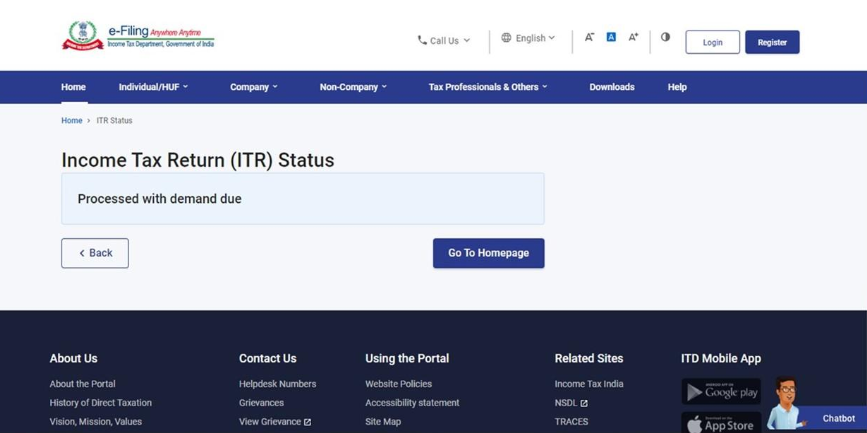

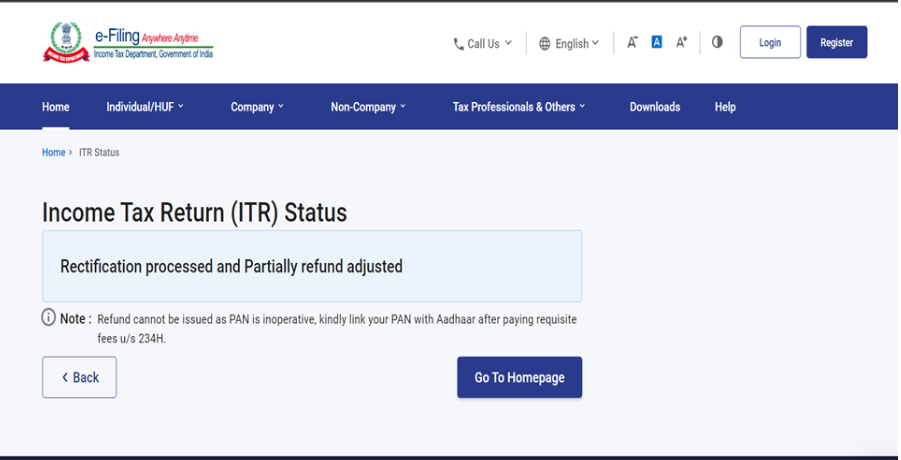

How to Check a Partnership Firm’s ITR Status?

After filing your Income Tax Return (ITR), it's important to track its status to ensure it has been successfully processed by the Income Tax Department. Whether you're waiting for a refund or simply want to confirm the filing, checking your ITR status is a quick and easy process.

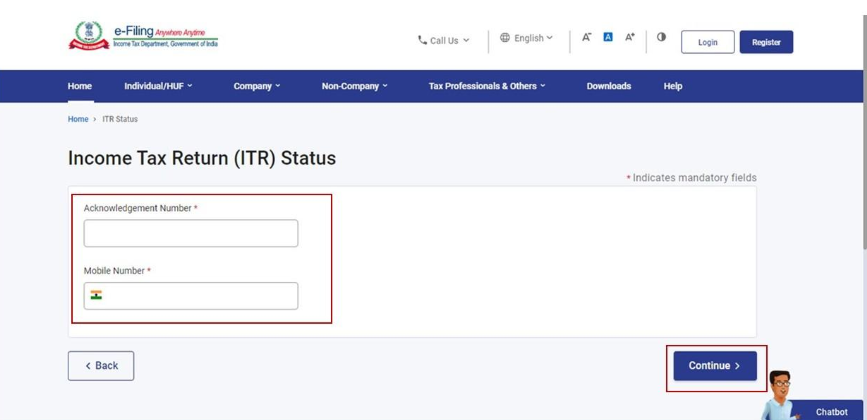

Case 1: Checking ITR Status Without Login

Step 1: Go to the e-Filing portal homepage.

Step 2: Click Income Tax Return (ITR) Status.

Step 3: On the Income Tax Return (ITR) Status page, enter your acknowledgement number and a valid mobile number and click Continue.

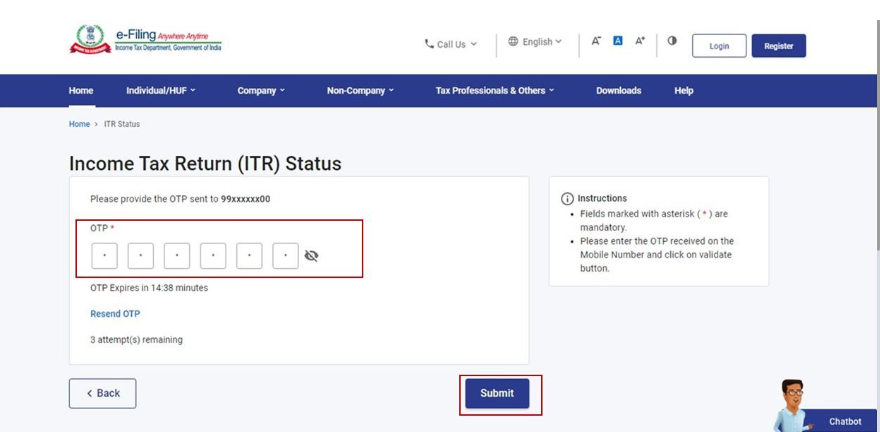

Step 4: Enter the 6-digit OTP received on your mobile number entered in Step 3 and click Submit.

Note:

- OTP will be valid for 15 minutes only.

- You have 3 attempts to enter the correct OTP.

- The OTP expiry countdown timer on screen tells you when the OTP will expire.

- On clicking Resend OTP, a new OTP will be generated and sent.

On successful validation, you will be able to view the ITR status.

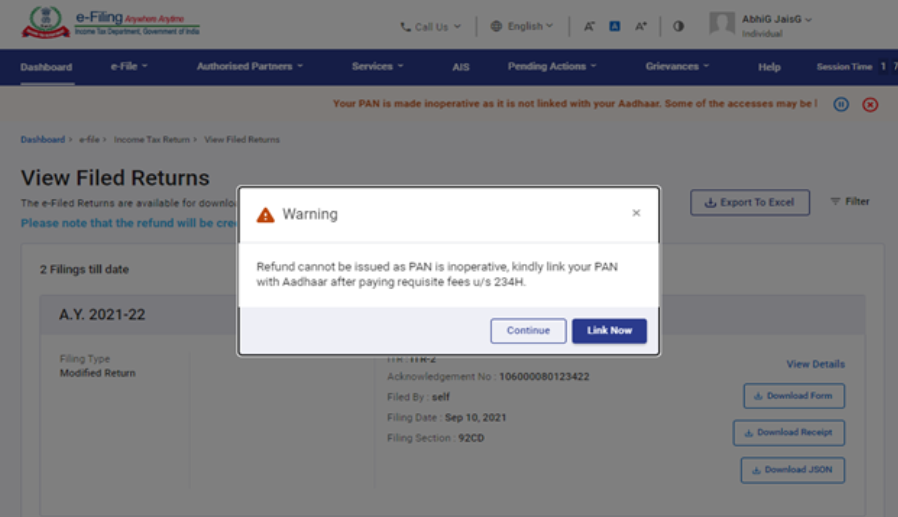

If your PAN is inoperative, a refund cannot be issued. Kindly link your PAN with Aadhaar after paying the requisite fee u/s 234H.

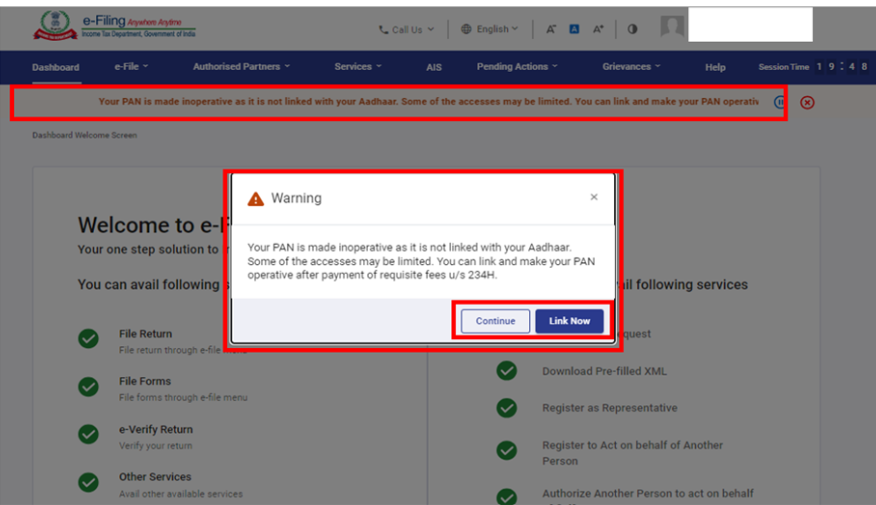

Case 2: Checking ITR Status After Login

Step 1: Log in to the e-Filing portal using your valid user ID and password.

For individual users, if PAN is not linked with the Aadhaar, you will see a pop-up message that your PAN is made inoperative as it is not linked with your Aadhaar.

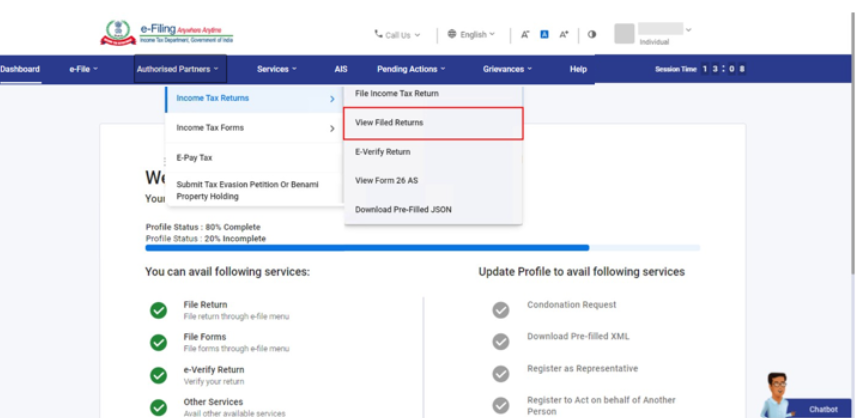

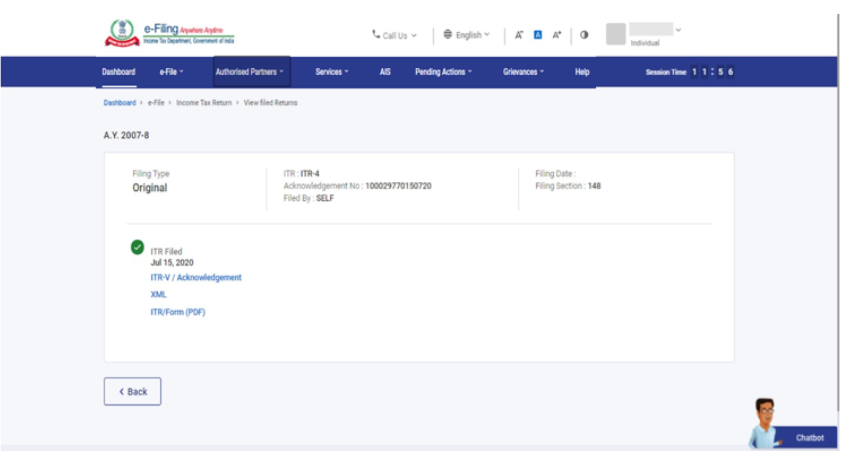

Step 2: Click e-File > Income Tax Returns > View Filed Returns.

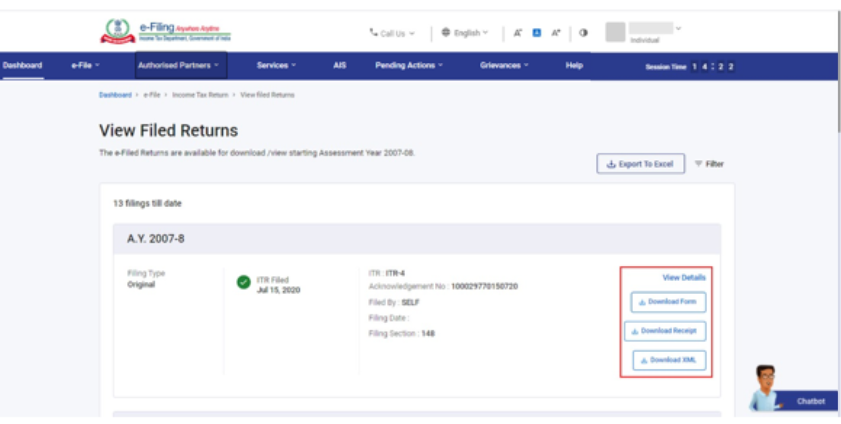

Step 3: On the View Filed Returns page, you will be able to view all the returns filed by you. You will be able to download the ITR-V Acknowledgement, upload JSON (from the offline utility), complete the ITR form in PDF, and the intimation order (by using the options on the right-hand side).

Note:

If your PAN is inoperative, you will see a pop-up message that a Refund cannot be issued as your PAN is Inoperative.

Note:

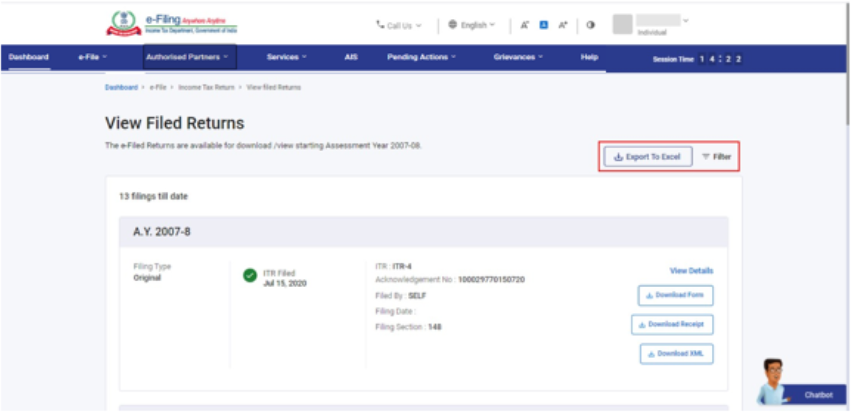

- Click Filter to view your filed returns based on different criteria (AY or Filing Type).

- Click Export to Excel to export your returns data to Excel format.

Click View Details to view the life cycle of the return and action items related to it (e.g., returns pending for e-Verification).

What to do if you get a notice from the Income Tax Department?

Receiving a notice from the Income Tax Department can be unsettling, but it's important to remember that not all notices are cause for alarm. Often, they are simply requests for clarification or additional documentation.

What is an Income Tax Notice?

An Income Tax notice is an official communication from the Income Tax Department to taxpayers regarding various aspects of their income tax filings. These notices can range from simple requests for more information or clarification to more serious matters like discrepancies in tax returns, audits, or demands for tax dues.

The primary goal of these notices is to ensure compliance with tax laws and to correct any inconsistencies or errors in income tax return filings. Many notices are auto-generated during routine scrutiny and do not necessarily indicate any wrongdoing. Their main purpose is to ensure compliance and accuracy in tax returns.

It's crucial for taxpayers to carefully review any notice received, understand exactly what is being asked, and respond appropriately within the specified timeframe to avoid legal or financial penalties.

Common Sections under which Income Tax Notices are Issued:

- Section 139(9): Defective return notice.

- Section 142(1): Inquiry before assessment (seeking documents or explanation).

- Section 143(1): Intimation of tax computation and adjustments.

- Section 143(2): Scrutiny notice for detailed assessment.

- Section 148: Reassessment for income that may have escaped assessment.

- Section 156: Demand notice for outstanding tax dues.

- Section 245: Adjustment of refunds against pending dues.

Steps to Take After Receiving an Income Tax Notice

Here are the essential steps to follow when you receive a notice from the Income Tax Department:

- Understand the Notice: First, thoroughly read the notice to grasp its nature. The Income Tax Department issues various notices under different sections of the Income Tax Act, 1961, each serving a unique purpose, such as requesting additional information, highlighting discrepancies in your tax return, or notifying you of outstanding dues.

- Verify Your Details: Double-check the information in the notice, including your name, PAN number, and the assessment year. Confirm that the notice is indeed for you and relates to your tax filings.

- Identify the Reason: Notices are sent for specific reasons, which are typically stated in the communication. Common reasons include not filing returns, differences between declared income and taxes paid, or failing to disclose all income sources.

- Gather Required Documents: Based on the reason for the notice, collect all relevant documents and information needed for an accurate response. This might include bank statements, investment proofs, Tax Deducted at Source (TDS) certificates, and previous years' tax returns.

- Respond Promptly: Notices usually have a deadline for your response. Adhering to this timeline is critical to prevent further penalties or legal action. In some cases, you can request an extension if you need more time.

- Seek Professional Help: If you're unsure how to proceed or if the notice involves complex tax issues, consider seeking professional assistance. Chartered accountants and tax advisors can offer expert guidance and help you prepare an appropriate response.

- Submit Your Response: Depending on the notice type and department requirements, you may need to submit your response online via the e-filing portal or in person at the designated income tax office. Ensure your response is clear, factual, and supported by all necessary documentation.

- Keep Records: After submitting your response, retain copies of the notice, your reply, and all supporting documents. These will be valuable for future reference and in case the department has any follow-up questions.

- Follow Up: If you don't receive an acknowledgment or a resolution from the department within a reasonable period, follow up through official channels. You can check the status of your response on the e-filing portal or contact the helpline for assistance.

- Stay Compliant: Finally, use this experience as a learning opportunity to ensure your future tax filings are accurate and compliant. Maintain meticulous records of your income, investments, and deductions to facilitate smoother tax filing processes.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

Is it compulsory to file a tax return for a dormant partnership firm?

−Yes, even a dormant partnership firm is generally required to file an income tax return. While it may not have active business operations or significant income, the Income Tax Act, 1961, mandates all firms to file a return, especially if they are registered. This ensures compliance and provides a record of the firm's status.

How are the partners taxed on their share of profit from the firm?

+Can a partnership firm revise its income tax return?

+What is the difference between a partnership firm and an LLP for tax purposes?

+Which ITR form should a partnership firm use to file its return?

+Can a partnership firm opt for presumptive taxation under Section 44AD or 44ADA?

+Are partners required to file separate returns apart from the firm’s return?

+Is an audit compulsory for all partnership firms?

+How can a partnership firm file its income tax return online?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for Filing ITR for a Partnership Firm?

Navigating partnership tax returns can be complex, but RegisterKaro makes it easy.

- Expert Tax Guidance: Our team of seasoned professionals provides expert advice on all aspects of partnership tax return filing, staying updated on the latest tax laws.

- Simple, Fast, and Online: Our streamlined online platform lets you easily submit documents, track progress, and communicate with our experts from anywhere.

- Clear, Upfront Pricing: We believe in transparency, offering clear pricing with no hidden fees so you know exactly what you're paying for.

- Timely Deadline Reminders: Never miss a tax deadline again. Our automated system sends timely reminders for all crucial filings, helping you avoid penalties.

Your Trusted Financial Partner: Beyond just filing, we're your partner in financial compliance, handling your tax burdens so you can focus on growing your business.

What Our Clients Say

View AllKesha Ram

Register Karo is a company carryout all task which you demand from Registeration process to final compliance of commencement of the new company. My e... Read more

Dhamodaran Narayana...

Thank you for the exceptional support provided by Vishakha throughout this process. My experience with RegisterKaro's company wind-up service was exce... Read more

Jit

Register Karo is the best platform to register your company, @kajal chowhan helped me a lot, to make the process smoothly. Thank you team registerkaro

Guru

professional work, good team work by the team allocated to us, on time delivery for incorporation of my company, Ankit followed a good workflow throug... Read more

yayati

I reached out to registerkro for company windup. Would like to give shout out to Astha gupta who was extremly helpful throughout the process. Kudos to... Read more

Vijay Azad

Hi It was pleasure to contact you@alka for company registration .Happy with the dedication and support during process and working beyond timeline...

aravind raj

We did startup registeration with their team, it was point to point approach and they were clear in those procedures and their followup is too good...

vinay kumar

Your staff Ankita Matta is a polite person the way of handling the issues was good. I hope in future register karo team handle the issues in a same wa... Read more

Riya Singh

Register karo demonstrated professionalism and expertise in navigating complex legal and regulatory issues related to our industry. Special thanks Ank... Read more

ganesh patil

Had a great experience with Register Karo. The LLP registration process was handled smoothly and everything was explained clearly. Highly recommended!

Related Blogs

View All

LLLP vs LLP: Key Differences, Liability, Taxation & Structure 2026

LLP Amendment Rules 2017: Form 24, Rule 37 & Strike-Off Process

LLP Rules 2009: Rule 24, Rule 37, Forms & Compliance 2026

LLP Partner Limit in India: Maximum & Minimum Partners

Appointment of Auditor in LLP: Procedure & Rules 2026

Procedure for Change of Name of LLP in India: Section 19

Convert Sole Proprietorship to LLP in India: Process & Fees

Can a Company Be a Partner in a Partnership Firm? Rules & Process

Difference Between Partnership and Joint Stock Company in India

Can LLP Buy Property in India? Rules, Process & Tax Guide