A GST notice is an official communication issued under the CGST Act, 2017, to registered taxpayers regarding compliance issues. GST officers issue these notices for return mismatches, unpaid taxes, excess Input Tax Credit claims, or registration-related discrepancies. The GSTN system also automatically generates certain notices when taxpayers fail to meet prescribed compliance requirements.

Receiving a GST notice does not always indicate fraud, tax evasion, or intentional non-compliance under GST laws. Many notices arise from reconciliation mismatches between GSTR-1, GSTR-3B, e-way bills, or supplier-reported transaction details. However, taxpayers must review every GST notice carefully because delayed responses may trigger penalties, interest, or recovery proceedings.

Businesses should maintain accurate GST records, reconcile returns regularly, and monitor portal communications to reduce compliance-related risks. This guide explains GST notice types, common reasons, reply procedures, applicable timelines, penalties, and online checking processes.

Key Takeaways

- GST notices are official communications issued under the CGST Act, 2017, to address discrepancies, non-compliance, or pending GST obligations.

- Authorities and the GSTN system issue notices for issues such as return mismatches, incorrect ITC claims, unpaid taxes, and registration-related discrepancies.

- A GST notice does not automatically indicate fraud; many notices arise from routine data mismatches between GSTR-1, GSTR-3B, GSTR-2B, and e-way bills.

- Taxpayers must review and respond to GST notices within the prescribed timelines to avoid penalties, interest, recovery actions, or ex parte orders.

- The GST compliance process generally follows a structured flow: Notice → Order → Demand/Recovery Notice.

- Different notice types serve different purposes, including return filing defaults (GSTR-3A), scrutiny (ASMT-10), show cause notices (DRC-01), audits (ADT-01), refunds (RFD-08), and registration cancellation (REG-17).

- Section 73 applies to non-fraud cases, while Section 74 applies to fraud or willful misstatement cases, with significantly higher penalties under Section 74.

- From FY 2024-25 onwards, Section 74A introduces a unified GST demand framework with stricter timelines and simplified procedures.

- Ignoring GST notices leads to serious consequences such as best judgment assessments, ex parte orders, interest at 18%, registration cancellation, and recovery proceedings.

Who Issues a GST Notice and Why is it Issued?

Different authorities handle GST notices depending on the nature of the compliance issue and the taxpayer’s jurisdiction. For example:

- Central GST (CGST) officers issue GST notices for taxpayers under the central tax jurisdiction.

- State GST (SGST) officers issue notices under GST for taxpayers administered by state tax departments.

- The GSTN system also automatically generates certain notices, such as GSTR-3A for non-filing, without manual intervention by a tax officer.

Common Reasons Why Businesses Receive GST Notices

The GSTN system runs automated checks on data filed by taxpayers and flags mismatches or anomalies. The table below lists the most common triggers that result in a notice under GST being issued to a business:

| Reason for GST Notice | What It Means |

|---|---|

| GSTR-1 and GSTR-3B mismatch | Outward supplies declared in GSTR-1 do not match the tax paid in GSTR-3B for the same period |

| ITC mismatch in GSTR-2B | Input tax credit claimed in GSTR-3B exceeds or does not match the ITC available in GSTR-2B as per supplier filings |

| Non-filing or late filing of returns | The taxpayer has not filed one or more GST returns by the due date, triggering an automated GSTR-3A notice |

| Excess ITC claims | The taxpayer has claimed ITC on ineligible expenses or above the amount reflected in GSTR-2B |

| Short payment of GST | Tax paid in GSTR-3B is lower than the liability declared in GSTR-1 or calculated by the system |

| E-way bill discrepancies | Goods transported under e-way bills do not match the corresponding invoices or GSTR-1 data |

| Suspicious or high-value transactions | Unusual patterns in turnover, ITC claims, or refund requests flagged through GSTN’s automated risk assessment systems |

| Incorrect GST refund claims | Refund applications contain errors, unsupported claims, or excess amounts compared to filed returns |

| Non-payment of TCS / TDS by e-commerce operators | TCS or TDS deductions under Section 51/52 not deposited or reported correctly |

| Reverse Charge Mechanism (RCM) liability missed | Indian businesses failing to report and pay RCM on foreign platform invoices (Google Ireland, Meta Ireland, etc.) |

Difference Between a GST Notice, Order, and Demand

Many taxpayers confuse these three terms; they represent different stages of the same process:

- A GST notice is the first communication asking the taxpayer to explain discrepancies, submit documents, or clarify compliance-related issues.

- An order follows the GST notice when the officer reviews the reply and decides the matter based on available records.

- A GST demand notice or recovery notice is issued after the order is passed and requires the taxpayer to pay the confirmed tax, interest, and penalty.

Process Flow: Notice → Order → Demand Notice

Types of GST Notices in India

The GST law prescribes different notice formats for different situations. Each notice type mentioned below has a specific purpose, a defined reply period, and consequences for non-response:

a. GSTR-3A: Notice for Non-Filing of Returns

The GSTN system automatically generates a GSTR-3A notice if taxpayers fail to file a return by the due date. This is a GST return notice that informs the taxpayer of the non-filing and requires them to file the pending return within 15 days of receiving the notice.

If the taxpayer does not respond within this period, the GST officer may pass a best judgment assessment order under Section 62 of the CGST Act and raise a tax demand based on available information.

b. ASMT-10: Scrutiny Notice for Return Discrepancies

A GST officer issues Form ASMT-10 when scrutiny of a filed GST return identifies discrepancies requiring clarification. Common triggers include:

- a mismatch between GSTR-1 and GSTR-3B figures

- or a difference between the ITC claimed and the amount available in GSTR-2B.

The taxpayer must reply within 30 days of receiving the ASMT-10 notice by filing Form ASMT-11 on the GST portal with a proper explanation and supporting documents.

c. DRC-01A: Pre-Show Cause Notice

Before issuing a formal show-cause notice under GST, an officer may send Form DRC-01A as a pre-show-cause intimation. This allows the taxpayer to review the proposed tax demand and either pay the outstanding tax with interest voluntarily or respond with a written explanation.

Responding at the DRC-01A stage helps the taxpayer avoid a formal show-cause notice and the associated penalties in many cases.

d. DRC-01: Show Cause Notice for Tax Demand

Form DRC-01 is the formal GST show cause notice issued under Section 73 or Section 74 of the CGST Act to recover short-paid, not paid, or wrongly refunded taxes. A show-cause notice under GST requires the taxpayer to explain why the proposed tax, interest, and penalty should not be imposed against them.

The reply deadline is stated in the notice itself, and the taxpayer must respond within that period to avoid an ex parte order.

Section 73 vs Section 74: Key Differences

The GST law created two separate frameworks for issuing demand notices based on whether fraud was involved. This distinction mattered because the penalty exposure and timelines differed significantly:

| Parameter | Section 73 (No Fraud) | Section 74 (Fraud or Wilful Misstatement) |

|---|---|---|

| Applicability | Genuine errors, negligence, or bona fide mistakes in tax payment | Fraud, suppression of facts, or wilful misstatement to evade tax |

| Penalty if paid before notice issued | No penalty (Section 73(5)) | 15% of tax (Section 74(5)) |

| Penalty if paid within 30 days of notice | No penalty; proceedings deemed concluded (Section 73(8)) | 25% of tax (Section 74(8)) |

| Penalty if paid after 30 days of notice but before the order | 10% of tax or ₹10,000, whichever is higher | — |

| Penalty if paid within 30 days of the order | 10% of tax or ₹10,000, whichever is higher | 50% of tax (Section 74(11)) |

| Penalty if not paid within 30 days of the order | 10% of tax or ₹10,000, whichever is higher | 100% of tax |

| Time limit for issuing notice | 2 years 9 months from the due date of the annual return for the relevant FY (notice within 3 years; order within 3 years) | 4 years 6 months from the due date of the annual return (notice within 5 years; order within 5 years) |

| Applicability period | FY 2023-24 and earlier | FY 2023-24 and earlier |

Critical Update: From FY 2024-25 onwards, the new Section 74A introduced by the Finance (No. 2) Act, 2024, replaces both Section 73 and Section 74 with a unified demand framework. Sections 73 and 74 continue to apply only to demands relating to FY 2023-24 and earlier financial years.

Introduction of Section 74A Under Finance Act 2024

The Finance Act 2024 introduced Section 74A as a new unified framework for GST demand proceedings, effective from FY 2024-25 onwards. Section 74A replaces the earlier distinction between Section 73 and Section 74 and creates a single mechanism for handling GST demand notices.

Important: From FY 2024-25 onwards, authorities issue all GST demand notices under the new unified Section 74A. Sections 73 and 74 continue to apply only to FY 2023-24 and earlier financial years.

Section 74A introduces several important procedural changes and taxpayer-friendly measures, including:

- A 42-month time limit for issuing demand notices from the due date of filing the annual return for the relevant financial year.

- A 60-day cure window for taxpayers to make payments and resolve disputes, increased from the earlier 30-day period.

- A ₹1,000 de-minimis threshold, below which authorities will not issue demand notices.

- A 12-month adjudication timeline for passing orders, extendable by an additional 6 months in specified cases.

Under Section 74A, authorities aim to streamline GST demand proceedings by reducing litigation complexity and establishing a more uniform compliance framework.

e. REG-17: GST Registration Cancellation Notice

A GST officer issues Form REG-17 as a GST registration notice proposing the GST Cancellation. Common reasons include non-filing of returns for 6 consecutive months, fraud, or business discontinuation. Taxpayers must respond within 7 working days through Form REG-18 with a valid justification to avoid cancellation.

f. ADT-01: GST Audit Notice

A GST officer issues Form ADT-01 to inform a registered taxpayer that their accounts and records will be audited under Section 65 of the CGST Act. The notice provides at least 15 working days’ advance notice before the audit commences.

The taxpayer must make all books of accounts, records, and documents available to the audit team during the audit period.

g. RFD-08: GST Refund Notice

When a taxpayer applies for a GST refund, and the processing officer identifies a discrepancy or requires additional information, the officer issues Form RFD-08 as a show cause notice.

The taxpayer must respond to RFD-08 within 15 days by filing Form RFD-09 with clarification or additional documents. Non-response results in rejection of the refund application.

How to Check GST Notices on the GST Portal?

Every GST notice issued by the department or generated by the GSTN system appears on the taxpayer’s dashboard on the official GST portal. Taxpayers must check the portal regularly to avoid missing notice deadlines:

1. Visit gst.gov.in and log in using your GSTIN, username, and password.

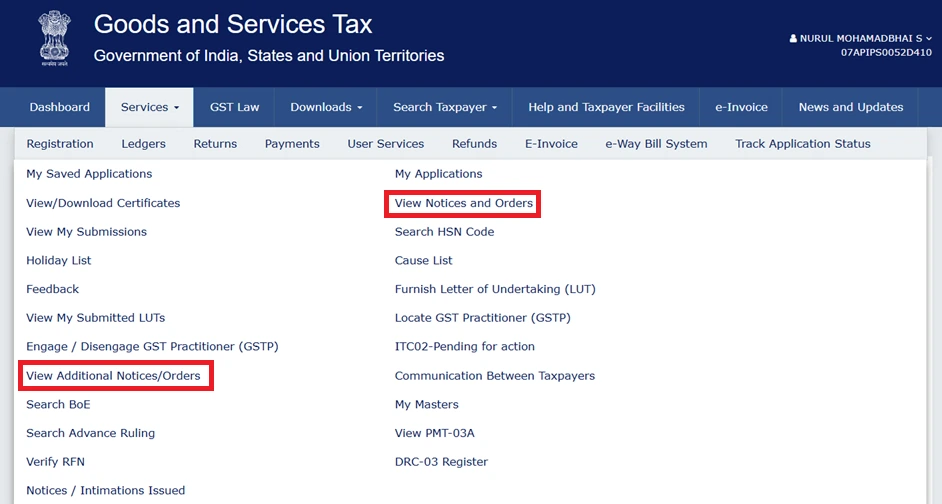

2. On the taxpayer dashboard, navigate to Services in the top menu bar.

3. Under Services, click on “User Services” and then select “View Notices and Orders” or “View Additional Notices/Orders” from the dropdown menu.

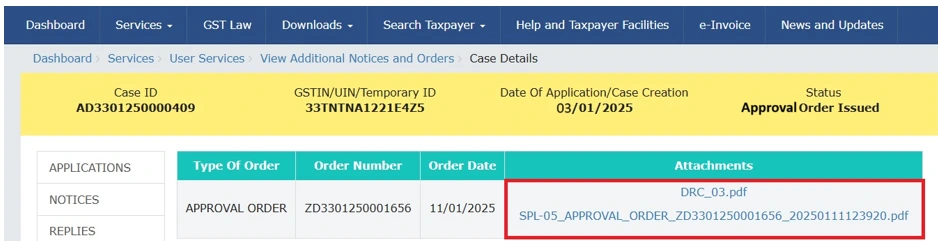

4. The portal displays all notices, orders, and communications issued against the GSTIN, arranged by date.

5. Click on the relevant notice reference number to open the notice details and read the full content.

6. Click the hyperlink under the attachment column to download as a PDF document for offline review.

7. Track the reply status of any notice you have already responded to by checking the status column on the same screen.

Note: Taxpayers who receive a GST notice via email should note that the email notification is only an alert. The official notice document always resides on the GST portal, and the reply must also be filed through the portal within the stipulated deadline.

Taxpayers must respond to GST notices within the prescribed timeline and submit complete supporting documents to avoid adverse orders and penalties. A timely and well-prepared response significantly improves the chances of resolving the matter without further litigation.

For a detailed step-by-step process on replying to GST notices online, read our complete guide on “How to Reply to GST Registration Notice.”

Time Limits to Respond to GST Notices

Different GST notices carry different response timelines based on the nature of the issue and the legal provision involved. The table below outlines the key GST notice types, their forms, reply deadlines, and consequences of non-response:

| Notice Type | Form | Reply Deadline | Consequence of Non-Response |

|---|---|---|---|

| Non-filing of return | GSTR-3A | 15 days from the notice date | Best judgment assessment under Section 62 |

| Scrutiny of returns | ASMT-10 (Reply: ASMT-11) | 30 days from the notice date | Further scrutiny or a show-cause notice |

| Pre-show cause intimation | DRC-01A | As specified in the notice (typically 15 days) | Formal DRC-01 issued |

| Show cause notice | DRC-01 (Reply: DRC-06) | As specified in the notice (typically 30 days) | Ex parte demand order under Section 73/74/74A |

| GST registration cancellation | REG-17 (Reply: REG-18) | 7 working days | GST registration cancelled |

| GST refund deficiency | RFD-08 (Reply: RFD-09) | 15 days | Refund application rejected |

| GST audit notice | ADT-01 | 15 working days before the audit | Adverse findings during the audit |

| Special audit | ADT-03 | As specified | Audit conducted by a CA / CMA nominated by the Commissioner |

| Section 62 best judgment order | Self (withdraw by filing a return) | Within 60 days of the order | Best judgment assessment becomes final |

Penalties for Ignoring GST Notices

Failure to respond to a GST notice within the prescribed timeline can lead to serious legal and financial consequences, including:

- Best judgment assessment under Section 62.

- Ex-parte demand orders.

- Interest at 18% per annum.

- GST registration cancellation.

- Recovery proceedings through bank attachment or property attachment.

- Criminal prosecution in fraud-related cases.

Common Mistakes in GST Notice Replies and How to Avoid Them

Businesses often make errors while replying to GST notices, which increases compliance risks and financial exposure. The table below highlights common mistakes, their impact, and the correct approach to prevent issues:

| Mistake | Impact | Solution |

|---|---|---|

| Not checking the GST portal regularly | Important notices and deadlines get missed | Monitor the GST portal weekly; subscribe to SMS/email alerts |

| Missing reply deadlines | GST department passes ex parte orders | Respond immediately within the prescribed timeline; track every notice on a compliance calendar |

| Submitting an incomplete reconciliation | Authorities confirm tax demand due to mismatches | Reconcile GSTR-1, GSTR-3B, and GSTR-2B fully before responding |

| Filing replies outside the GST portal | The department does not record the submission | Always file replies through the GST portal only |

| Not consulting professionals | Responses remain weak or incomplete | Seek CA or GST expert guidance for accurate replies |

| Treating email alerts as the full notice | Missing official notice details and deadlines | Always open and read the official notice on the GST portal |

| Paying tax without legal review | Voluntary payment locks in liability that could have been challenged | Get a professional opinion on disputed amounts before paying |

| Ignoring GSTR-3A (non-filing) notices | Best judgment assessment under Section 62 | File the pending return within 30 days of the best judgment order to have the order withdrawn |

| Not maintaining records for 72 months | Failure to defend old period notices | Retain invoices, contracts, bank statements, and reconciliations for 72 months (Section 36) |

GST notices are an unavoidable part of doing business under the GST regime, but the difference between a smooth resolution and a costly demand order often lies in how the reply is drafted and submitted. The most common drivers of escalated disputes are missed deadlines, vague replies, and incomplete reconciliations. Businesses managing multi-state filings, high ITC volumes, or recurring audits benefit significantly from a structured compliance workflow.

For founders managing both registration and ongoing filings, GST registration followed by regular GST return filing, combined with monthly GSTR-2B reconciliation, is the most effective way to prevent notices in the first place. When a notice does arrive, professional drafting and timely portal-based reply submission remain the only paths to resolution.

Contact RegisterKaro today to manage your GST compliance efficiently and stay aligned with GST requirements without delays or errors!