DIR-11 Form for Resignation of Director 2026: Filing Process & Procedure

Form DIR-11 is an electronic intimation that a resigning director files with the Registrar of Companies (RoC) under the proviso to Section 168(1) of the Companies Act, 2013, read with Rule 16 of the Companies (Appointment and Qualification of Directors) Rules, 2014. It creates an independent legal record of the resignation date on the MCA database, separate from the company’s mandatory Form DIR-12 filing under Section 170, protecting the director against future liability and MCA-record mismatches.

Since the Companies (Appointment and Qualification of Directors) Amendment Rules, 2018, DIR-11 became optional for the resigning director (the company’s DIR-12 filing remains mandatory). However, most practising directors still file DIR-11 as a protective safeguard, particularly when the company is slow to file DIR-12, when there’s any risk of dispute with the company, or when the director needs independent ROC-side proof of the exact resignation date.

This guide covers the complete DIR-11 framework, the form’s legal purpose, when filing becomes practically necessary, the documents required (including the often-confused “proof of dispatch”), the step-by-step MCA V3 portal procedure, current fees (₹200–₹600 per filing), and how DIR-11 differs from DIR-12 in scope, responsibility, and legal effect.

Key Takeaways

- DIR-11 is now optional, DIR-12 is mandatory: Since the Companies (Appointment and Qualification of Directors) Amendment Rules, 2018, DIR-11 filing by the resigning director is optional (but recommended as a safeguard). The company must still file Form DIR-12 within 30 days under Section 170.

- Governing law: Form DIR-11 falls under the proviso to Section 168(1) of the Companies Act, 2013, and Rule 16 of the Companies (Appointment and Qualification of Directors) Rules, 2014. It is filed entirely on the MCA V3 portal.

- Resignation date is fixed by Section 168(2): The resignation becomes effective on the date the company receives notice or the date specified by the director, whichever is later.

- Filing fee ranges from ₹200 to ₹600: The government fee depends on nominal share capital, ₹200 below ₹1 lakh, ₹300–₹500 for mid-range slabs, and ₹600 for ₹1 crore and above.

- Liability survives resignation: A director remains responsible for actions taken during their tenure under Section 168(2), even after DIR-11 filing. The form only protects against future risks.

- DIR-11 is processed through Straight Through Processing (STP) on the MCA V3 portal; there is no manual approval; the SRN generated at submission is the confirmation.

What is DIR-11? Purpose and Why it Matters

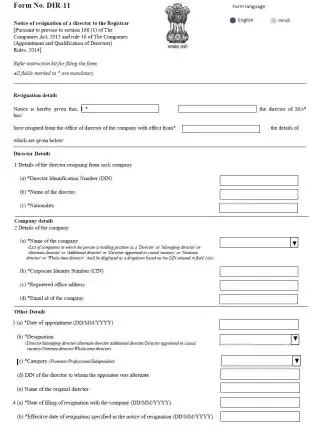

Form DIR-11 is an electronic director resignation form that a director files with the MCA after resigning from a company. Section 168(1) of the Companies Act, 2013, and Rule 16 of the Companies (Appointment and Qualification of Directors) Rules, 2014, govern this filing requirement.

DIR-11 Form generally includes:

- Date of resignation

- Reasons for resignation

- Copy of the resignation letter

- Proof of acknowledgment from the company

The form allows the director to officially inform the Registrar of Companies (ROC) about the resignation. It creates an independent legal record of the resignation date and helps establish when the director’s responsibilities ended.

Filing DIR-11 helps:

- Establish the official resignation date

- Limit liability for company actions after resignation

- Create a legal record with the ROC

- Submit proof of resignation and acknowledgment

- Reduce the risk of future disputes or compliance issues

This filing also strengthens the director’s legal position in case of company defaults, compliance delays, or MCA record mismatches. In many cases, the MCA may notify the company after DIR-11 is filed, prompting it to complete the DIR-12 filing process.

Is Filing DIR-11 Mandatory for Directors?

Filing DIR-11 is no longer mandatory for resigning directors in every case. The Companies (Appointment and Qualification of Directors) Amendment Rules, 2018, made it optional for directors.

Under the current rules, the company is primarily responsible for filing Form DIR-12 with the ROC after receiving the resignation notice from the director. The board typically passes a board resolution for the resignation of a director to record the exit before filing DIR-12.

However, directors still file DIR-11 as a protective measure. It becomes important when:

- The company does not file DIR-12 on time.

- MCA records continue showing the director as active.

- The director needs direct proof of resignation with the ROC.

Although optional, filing DIR-11 reduces legal risk. It ensures the resignation by the director is clearly recorded in MCA systems without dependency on the company’s action.

DIR-11 Time Limit – When Does the 30-Day Clock Start?

Under Rule 16 of the Companies (Appointment and Qualification of Directors) Rules, 2014, a resigning director must file DIR-11 within 30 days from the date of resignation. The “date of resignation” here means the effective date as determined by Section 168(2), i.e., either:

- The date on which the company received the resignation notice, OR

- The date specified by the director in the resignation notice

- Whichever is later

Examples:

- Example 1: The director sends a resignation on 1 April; the company receives it on 3 April; the director did not specify any future date. Effective date: 3 April. DIR-11 must be filed by 2 May (30 days from 3 April).

- Example 2: Director sends resignation on 1 April specifying 30 April as the effective date; the company receives it on 3 April. Effective date: 30 April (the later date). DIR-11 must be filed by 30 May.

- Example 3: Director sends resignation on 1 April specifying 20 March (a past date) as the effective date; the company receives it on 3 April. Effective date: 3 April (the later date, past dates specified in the resignation are overridden by the receipt date).

Filing after 30 days is permitted but attracts additional fees as per the Companies (Registration Offices and Fees) Rules, 2014.

Documents Required for DIR-11 Filing (MCA V3 Portal)

You must provide accurate details in Form DIR-11 to complete filing on the MCA V3 portal. Keep the following information ready before you begin:

Mandatory attachments

- Notice of resignation — Signed copy of the resignation letter addressed to the company’s Board of Directors

- Proof of dispatch to company — Postal receipt, courier tracking record, or email acknowledgement (see the “Proof of Dispatch” section above for accepted formats)

Optional / case-specific attachments

- Acknowledgement of resignation by the company — Letter, email, or board minute confirming receipt of resignation (strengthens the filing but is not mandatory if proof of dispatch is provided)

- Other supporting documents — Only if relevant to a specific dispute or clarification (e.g., if the resignation was contested by the company)

Pre-requisites (not document attachments, but required for filing access)

- Active Director Identification Number (DIN) of the resigning director

- Valid Class 3 Digital Signature Certificate (DSC) of the resigning director, registered on the MCA V3 portal and mapped to the DIN

- MCA V3 portal user account (the director’s individual login, not the company’s account)

Note: PAN, Aadhaar, address proof, and KYC documents are not separately attached to DIR-11; those records are already linked to the director’s DIN through prior DIR-3 KYC filings. If the DIN is deactivated due to a missed DIR-3 KYC, the director must first reactivate the DIN (by filing DIR-3 KYC with a ₹5,000 late fee) before filing DIR-11.

What is “Proof of Dispatch” in DIR-11?

“Proof of dispatch” in DIR-11 refers to documentary evidence that the resigning director actually delivered the resignation letter to the company’s registered office. It is a mandatory attachment to Form DIR-11 because the resignation’s legal effect under Section 168(2) depends on the date the company received the notice, and the proof of dispatch establishes that delivery date.

Acceptable forms of proof of dispatch

| Delivery Method | Proof Document | What It Should Show |

|---|---|---|

| Speed Post / Registered Post | Postal department dispatch receipt + tracking record + delivery confirmation | Date of dispatch, recipient’s registered office address, delivery date |

| Courier (Blue Dart, DTDC, FedEx, etc.) | Courier consignment receipt + online tracking screenshot showing delivery | Tracking number, delivery date, and recipient signature |

| Email to Company Secretary / Director | PDF of email with timestamp + read receipt (if available) + email headers | Sender, recipient at official company domain, date, time |

| Hand delivery | Acknowledgement on company letterhead with stamp and signature | Receiving officer’s name, date, time, signature |

Avoid these common mistakes:

- Sending the resignation only via WhatsApp or personal email is generally treated as informal communication by MCA

- Sending to a personal email of a director instead of the company’s registered email or registered office

- Failing to retain tracking confirmation before the courier portal archives the record (most couriers archive after 90 days)

If the company subsequently issues a written acknowledgement of the resignation, attach that as additional supporting evidence, but the proof of dispatch alone is sufficient for DIR-11 filing.

How to File DIR-11 on the MCA Portal? Procedure for Resignation of a Director

Follow these steps to complete the director resignation form filing on the MCA V3 portal without errors:

Step 1: Draft Resignation Letter

Prepare a formal resignation letter addressed to the Board of Directors. Clearly mention the effective date of resignation and the reason for leaving the company.

Ensure the language remains professional and unambiguous.

Step 2: Send Notice to Company

Send the resignation letter to the company’s registered office using email, courier, or speed post. Preserve proof of dispatch, as you must attach it during filing.

Step 3: Gather Required Documents

Collect all required documents before starting the filing. Keep your resignation letter, proof of dispatch, company acknowledgement (if available), PAN, address proof, and valid DSC ready for upload.

Step 4: Access DIR-11 Form on MCA V3 Portal

Log in to the MCA V3 portal (mca.gov.in) using OTP or your DSC token through your individual user account (not the company’s account).

Navigate to: My Application → Form DIR-11. The form will appear as “DIR-11, Notice of resignation of a director to the Registrar.”

Important: DIR-11 is now a web-based form on MCA V3; you fill it directly in the browser, not by downloading and uploading a PDF/JAR file as on the older MCA V2 portal. Save progress at each section using the “Save & Next” button to avoid losing data if the session times out.

Step 5: Fill CIN, DIN & Resignation Details

Enter the company’s CIN, your DIN, date of resignation, and reason for resigning. The system auto-fetches company details from the CIN. Verify every field carefully, and make sure the resignation date matches your letter exactly.

Step 6: Attach Supporting Documents

Upload the resignation letter, proof of dispatch, and company acknowledgement (if applicable). Use only PDF or JPG files within the prescribed size limits.

Double-check that each document is legible and uploaded to the correct field.

Step 7: Affix DSC

Sign the form using a valid Class 3 Digital Signature Certificate registered on the MCA portal. Confirm that your DSC is active, not expired, and correctly linked to your DIN. The name on the DSC must match your MCA records.

Step 8: Upload Form on MCA Portal

- Review all entered details and uploaded documents before submitting.

- Run pre-scrutiny so the portal validates your entries and flags errors.

- Fix any flagged issues, then submit the signed form on the V3 portal.

Step 9: Payment of ROC Fees

Pay the applicable ROC fee through the MCA payment gateway using net banking, credit/debit card, or UPI. The system automatically calculates filing fees based on the company’s nominal share capital and applicable fee rules in force at the time of filing.

DIR-11 Filing Fee (Based on Nominal Share Capital)

| Company’s Nominal Share Capital | DIR-11 Filing Fee |

|---|---|

| Less than ₹1,00,000 | ₹200 |

| ₹1,00,000 to less than ₹5,00,000 | ₹300 |

| ₹5,00,000 to less than ₹25,00,000 | ₹400 |

| ₹25,00,000 to less than ₹1,00,00,000 | ₹500 |

| ₹1,00,00,000 or more | ₹600 |

| Company without share capital | ₹200 |

For late filing (after the 30-day window): Additional fees apply on a sliding scale based on the delay period under the Companies (Registration Offices and Fees) Rules, 2014, typically 2x to 12x the standard fee depending on the delay. For example, filing 90 days late on a company with ₹1 crore+ capital can cost up to ₹3,600 (6x ₹600).

Tip: Do not close the session until you receive payment confirmation, as incomplete transactions may lead to filing failure or duplication issues.

Step 10: SRN Generation & Acknowledgment

After submission, note the Service Request Number (SRN) the system generates. DIR-11 is processed automatically through Straight Through Processing (STP). This SRN is your proof of filing, so save it and the acknowledgement email for your records.

The entire filing process of filing DIR-11 usually takes around just 20 to 30 minutes online, provided all documents and your DSC are ready in advance.

What Happens After Filing DIR-11?

After you file Form DIR-11 on the MCA V3 portal, the system processes your submission and updates the ROC records based on the details provided.

- The MCA records your resignation details in its database for compliance and verification purposes.

- The MCA may notify the company and prompt it to file Form DIR-12 to complete the resignation process.

- MCA records reflect your resignation status from the effective resignation date mentioned in the form.

- You are no longer responsible for the company’s compliance or operations after the effective resignation date.

- If the company delays DIR-12 filing, your DIR-11 filing continues to act as official evidence of your resignation.

Can DIR-11 Be Withdrawn or Revised After Filing?

DIR-11 cannot be withdrawn or revised once it is filed and processed on the MCA V3 portal. Because DIR-11 is processed through Straight Through Processing (STP), meaning automatic acceptance without manual RoC review, the system treats the SRN as a final intimation to the Registrar.

If you discover an error after filing, you have these options:

- Minor data errors (typo in CIN, wrong attachment) — File a clarification application with the relevant RoC office explaining the error, supported by corrected documents

- Resignation withdrawn or rescinded (you decided to stay in the company). If both you and the company agree to reverse the resignation, the company can pass a fresh board resolution, and you file a fresh DIR-12 (re-appointment); DIR-11 itself cannot be cancelled

- Resignation date specified incorrectly — File a written clarification with the RoC, supported by the original resignation letter, showing the correct date

- Filed by mistake (you didn’t actually resign) — Approach the RoC immediately with an affidavit explaining the circumstances; consult a PCS before taking action

Key point: Because Section 168(2) determines the legal resignation date independently of DIR-11 filing, a wrongly-filed DIR-11 doesn’t automatically end your directorship, but it creates a misleading MCA record that needs prompt correction.

Legal Consequences of Not Filing DIR-11

Not filing Form DIR-11 does not always create immediate penalties, but it can lead to serious practical and legal risks for a resigning director, including:

- The director may continue to appear as active in MCA records, even after resignation.

- The director may face unnecessary compliance queries or notices linked to the company’s future defaults.

- The lack of independent resignation proof can create disputes between the director and the company.

- The director may face difficulty proving the exact resignation date in legal or regulatory matters.

- Ongoing liability concerns may arise if records do not clearly reflect the exit date.

Filing DIR-11 helps avoid these issues by creating an independent record of resignation with the ROC and strengthening the director’s legal position.

Is There a Direct Penalty for Non-Filing of DIR-11?

DIR-11 is no longer mandatory after the 2018 amendment, so there is no direct statutory penalty on the director for not filing it. However, non-filing creates several indirect financial and legal exposures:

| Risk Category | What Happens If DIR-11 Is Not Filed |

|---|---|

| Continued MCA listing as director | If the company also delays DIR-12, the director remains listed as active on MCA — exposing them to director disqualification under Section 164(2) if the company defaults on AOC-4 or MGT-7 for 3 consecutive years |

| Section 164 disqualification risk | The default years count against the director’s eligibility to be a director in any other Indian company for 5 years |

| Compliance notices | MCA-issued show-cause notices, ROC inquiries, or income tax notices arising from the company’s defaults may continue to reach the resigned director |

| No independent resignation proof | In disputes, the director relies entirely on the company-filed DIR-12, which may be wrong, delayed, or contested |

| Late filing fees if filed later | When the director eventually files DIR-11 beyond the 30-day window, additional fees up to 12x the base fee apply |

Effectively: While there is no penalty for not filing DIR-11, the cost of eventually needing to file it late or having no independent proof during a Section 164 challenge can run into lakhs. This is why most practising directors file DIR-11 as a defensive practice within 30 days of resignation.

Common Mistakes While Filing DIR-11 and How to Avoid Them

Many directors face delays, rejections, or validation errors during DIR-11 filing due to small but critical mistakes. Avoid these issues to ensure smooth submission and accurate MCA records:

- Entering incorrect CIN or DIN details: Even a single wrong digit can prevent system validation or pull incorrect company data. Always cross-check details from official MCA records before starting the filing.

- Mismatch in resignation details: Differences between the resignation letter and DIR-11 form, especially in the effective date or reason, can trigger rejection. Ensure consistency across all documents.

- Weak or missing proof of dispatch: Filing without proper evidence of sending the resignation to the company can weaken your legal record. Always retain email acknowledgment, courier receipt, or speed post tracking proof.

- Delayed filing after resignation: Late filing can create confusion in MCA records and increase compliance risk. File DIR-11 as soon as possible after resignation to maintain clear legal proof.

- DIN deactivation or DSC issues blocking filing: If your DIN is deactivated or your DSC has expired, is invalid, or is not mapped correctly, you cannot file DIR-11. Always ensure your DIN is active and your Class 3 DSC is valid and properly registered on the MCA portal before starting the process.

DIR-11 vs DIR-12: Key Differences

DIR-11 and DIR-12 both relate to a director’s resignation, but they serve different purposes. Here’s how they compare:

| Basis | DIR-11 | DIR-12 |

|---|---|---|

| Filed by | Resigning director (individual) | Company (Board of Directors) |

| Purpose | Inform RoC about the director’s resignation | Update MCA records about appointment/resignation/changes in directors |

| Nature | Optional (protective filing for the director) | Mandatory company compliance filing |

| Legal provision | Proviso to Section 168(1) read with Rule 16 of Companies (Appointment & Qualification of Directors) Rules, 2014 | Section 170 read with Rule 18 of the same Rules |

| Time limit | Within 30 days from the date of resignation (effective date under Section 168(2)) | Within 30 days from the date of resignation, appointment, or change |

| Primary function | Creates independent proof of resignation in MCA records | Officially updates the company’s director details in MCA |

| Filed through | Individual director’s MCA V3 account; DSC of resigning director | Company’s MCA V3 account; DSC of authorised director and PCS / CA / CWA certification |

| Filing fee | ₹200–₹600 based on the company’s nominal share capital | ₹200–₹600 based on the company’s nominal share capital |

| Processing | Straight Through Processing (STP) — no manual approval | Straight Through Processing (STP) — no manual approval |

| Penalty for non-filing | No direct penalty (optional filing), but creates indirect Section 164 / liability exposure | Mandatory — non-filing attracts company default consequences |

Let RegisterKaro assist you with end-to-end DIR-11 filing support. We ensure your resignation gets correctly recorded with the ROC without errors or delays. Our team also helps you handle MCA documentation smoothly so you can complete the process with confidence. Contact us today for a free consultation!