Sole Proprietorship vs LLC: Differences, Taxes & Best Fit (2026 Guide)

A Sole Proprietorship is a business owned and run by one individual with no legal separation between the owner and the business. An LLC (Limited Liability Company) is a US-specific business structure that combines partnership-style flexibility with corporate-style limited liability protection. Its closest Indian equivalents are the Limited Liability Partnership (LLP) and Private Limited Company.

The most important difference between the two is legal separation: a sole proprietor is personally liable for every business debt and lawsuit, while an LLC (or LLP/Pvt Ltd in India) is a separate legal entity that shields the owner’s personal assets. That single distinction drives most other differences: taxation, compliance burden, fundraising potential, and exit options.

This guide compares Sole Proprietorship vs LLC head-to-head on taxes, liability, ownership, setup cost, scalability, and compliance, and maps each LLC feature to its Indian equivalent (LLP / Private Limited / OPC) so readers in India can pick the right local structure.

Key Takeaways

- Sole Proprietorship = one person owns the business with no legal separation; unlimited personal liability; simplest setup; taxed as personal income.

- LLC = US-specific limited liability entity governed by individual state laws; offers personal asset protection; flexible tax treatment.

- In India, “LLC” does not exist as a legal entity. The closest Indian equivalents are Limited Liability Partnership (LLP) under the LLP Act, 2008, and Private Limited Company under the Companies Act, 2013.

- Tax treatment: US LLCs default to pass-through taxation; Indian LLPs and Pvt Ltds are taxed at flat 30% / 22%-25% respectively (with surcharge & cess).

- Best for: Sole Proprietorship suits low-risk solo ventures; LLC (or LLP/Pvt Ltd in India) suits businesses needing liability protection, investor funding, or scale.

- Conversion path: Sole proprietorships can be restructured into an LLC in the US, or LLP/Pvt Ltd/OPC in India, as the business grows.

What is a Sole Proprietorship?

A Sole Proprietorship is the simplest form of business structure, where the business is owned and operated by one individual. It is commonly chosen by small business owners, freelancers, and independent contractors due to its ease of setup and minimal costs.

Key Features of Sole Proprietorship

One of the most notable features of a sole proprietorship is single ownership and management. The owner independently handles profits, losses, and business strategies without the need to consult partners or shareholders. Similarly, other prime characteristics of sole proprietorship are:

- Complete Control: As a sole proprietor, you have full control over the business. You make all decisions regarding the operations. The structure also offers direct ownership of profits. All income earned belongs to the proprietor, and profits are taxed as personal income under individual income tax slabs. This also means the proprietor pays tax on the entire profit at slab rates, which can reach 30%+.

- No Formal Registration Needed: It is the simplest and most affordable structure to start with, requiring minimal paperwork and regulatory compliance. Sole proprietorship registration is a combination of multiple registrations, namely GST, MSME, Shop & Establishment, and Professional Tax. As a whole, it is not a mandatory requirement; however, multiple registrations under it are required for legal standing for Indian businesses.

- Income Taxation: The owner directly reports profits from a sole proprietorship on their personal tax return and taxes them as personal income.

- No Separation Between Business and Owner: Legally, you and the business are the same. You get unlimited liability, meaning personal assets such as savings or property can be used to settle business debts or liabilities. While this increases risk, it also simplifies compliance and reporting requirements.

Read also: Benefits of Registering a Sole Proprietorship in India

Example of Sole Proprietorship

US example: John, a freelance graphic designer in Texas, starts as a sole proprietorship to avoid the state filing fee and the Operating Agreement complexity of forming an LLC. He reports his business income on Schedule C of Form 1040 along with his personal tax return.

India example: Priya, a Bengaluru-based freelance graphic designer, starts as a sole proprietor with only GST and Udyam (MSME) registrations. She files ITR-3 or ITR-4 (presumptive scheme); her freelance income is taxed at her personal slab rate without any separate corporate filing.

Important: One significant drawback of this structure is that the owner is personally liable for any debts or legal claims against the business, meaning personal assets like savings or property could be at risk. Hence, it’s crucial to understand the pros and cons of LLC vs sole proprietorship.

What is an LLC (Limited Liability Company)? Key Features

A Limited Liability Company (LLC) combines the simplicity and flexibility of a sole proprietorship with the legal protections of a corporation. LLCs are designed to offer limited liability protection to the owners (members), meaning personal assets are generally protected from business-related debts and legal actions.

Key Features of LLC

A Limited Liability Company (LLC) combines the flexibility of a traditional partnership with the benefits of limited liability. Below are the key features of an LLC, with notes on how each feature maps to the equivalent Indian business structure (LLP or Private Limited Company):

- Limited Liability Protection: LLCs generally protect the owners’ personal assets (like homes, cars, and savings) from business debts and lawsuits.

- Flexible Taxation Options (US LLCs only): US LLCs can elect their tax classification under IRS rules, taxed as a sole proprietorship (single-member LLC default), partnership (multi-member default), S-Corp, or C-Corp via Form 8832 or Form 2553. In India, this election does not exist; LLPs are always taxed at a flat 30% under Section 115BBI of the Income Tax Act, 1961, and Pvt Ltd companies are taxed at the applicable corporate rate (22% under Section 115BAA, 25% for turnover ≤ ₹400 crore, or 30% otherwise).

- Ownership Flexibility: LLCs can have one or more owners (members), and can even have corporations or other LLCs as members.

- Credibility and Trust: LLCs are often viewed as more professional and credible by banks, investors, and customers.

- Separate Legal Entity: An LLC has its own legal identity, separate from its partners. This means the LLC can own property, enter into contracts, sue, or be sued in its own name. Even if partners change, the LLC continues to exist without interruption.

- Reduced Compliance Burden: Compared to private limited companies, LLCs have fewer compliance requirements. Annual filings, board meetings, and statutory audits are simpler, helping businesses save time, effort, and compliance costs.

Example of LLC

A small e-commerce business might start as an LLC to gain credibility and protect the owners’ personal assets. The LLC can raise capital by bringing in investors, which would not be possible with a sole proprietorship.

Read Also: Demystifying Indian Taxes for Limited Liability Companies

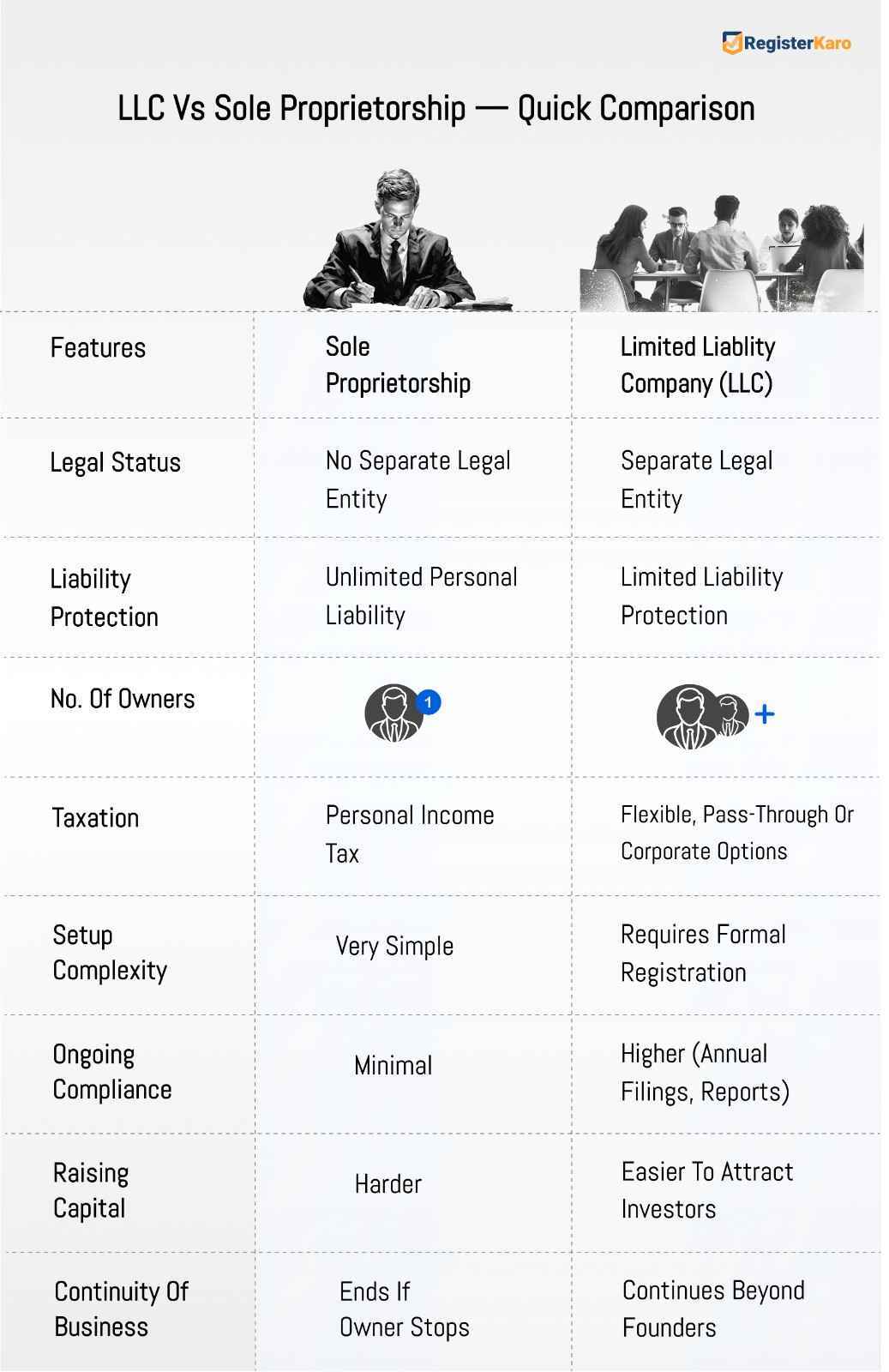

LLC vs Sole Proprietorship – Comparison

When comparing a Limited Liability Company vs a Sole Proprietorship, several key differences can impact the future of your business:

a. Legal Liability

- Sole Proprietorship: No separation between business and owner, meaning you’re personally liable for business debts.

- LLC: Provides liability protection, separating the owner’s personal assets from business debts and lawsuits.

b. Taxation

- Sole Proprietorship: Income is reported on the owner’s personal tax return.

- LLC: LLCs have more flexibility in taxation and can opt to be taxed as a corporation, potentially reducing self-employment taxes.

c. Compliance and Costs

- Sole Proprietorship: Easy to set up with minimal paperwork and no registration fees.

- LLC: Requires state registration, potentially higher setup costs, and ongoing compliance with legal formalities.

d. Ownership

- Sole Proprietorship: Owned by a single individual.

- LLC: Can have multiple members (owners) and can even include corporations as members.

Similarities Between LLC and Sole Proprietorship

Although LLCs and Sole Proprietorships differ in structure and legal protections, they share a few fundamental similarities. Some of them are:

- Easy to Start: Both structures are relatively simple to set up compared to corporations, making them suitable for new entrepreneurs.

- Pass-Through Taxation (US LLCs default; Indian LLPs partially): A US LLC and a US sole proprietorship both default to pass-through taxation; profits flow to the owner’s personal return without entity-level corporate tax. In India, an LLP is technically taxed at the entity level (flat 30%), but partners’ profit shares are exempt in their hands under Section 10(2A), achieving an effective single-layer tax outcome. A sole proprietor is always taxed at personal slab rates.

- Owner Control: The business owner retains full decision-making authority in a Sole Proprietorship and significant control in a single-member LLC.

- Flexible Operations: Both allow flexible operations without strict requirements like board meetings or complex record-keeping.

- Suitable for Small Businesses: Both models work well for freelancers, consultants, and small businesses that prefer straightforward management and taxation.

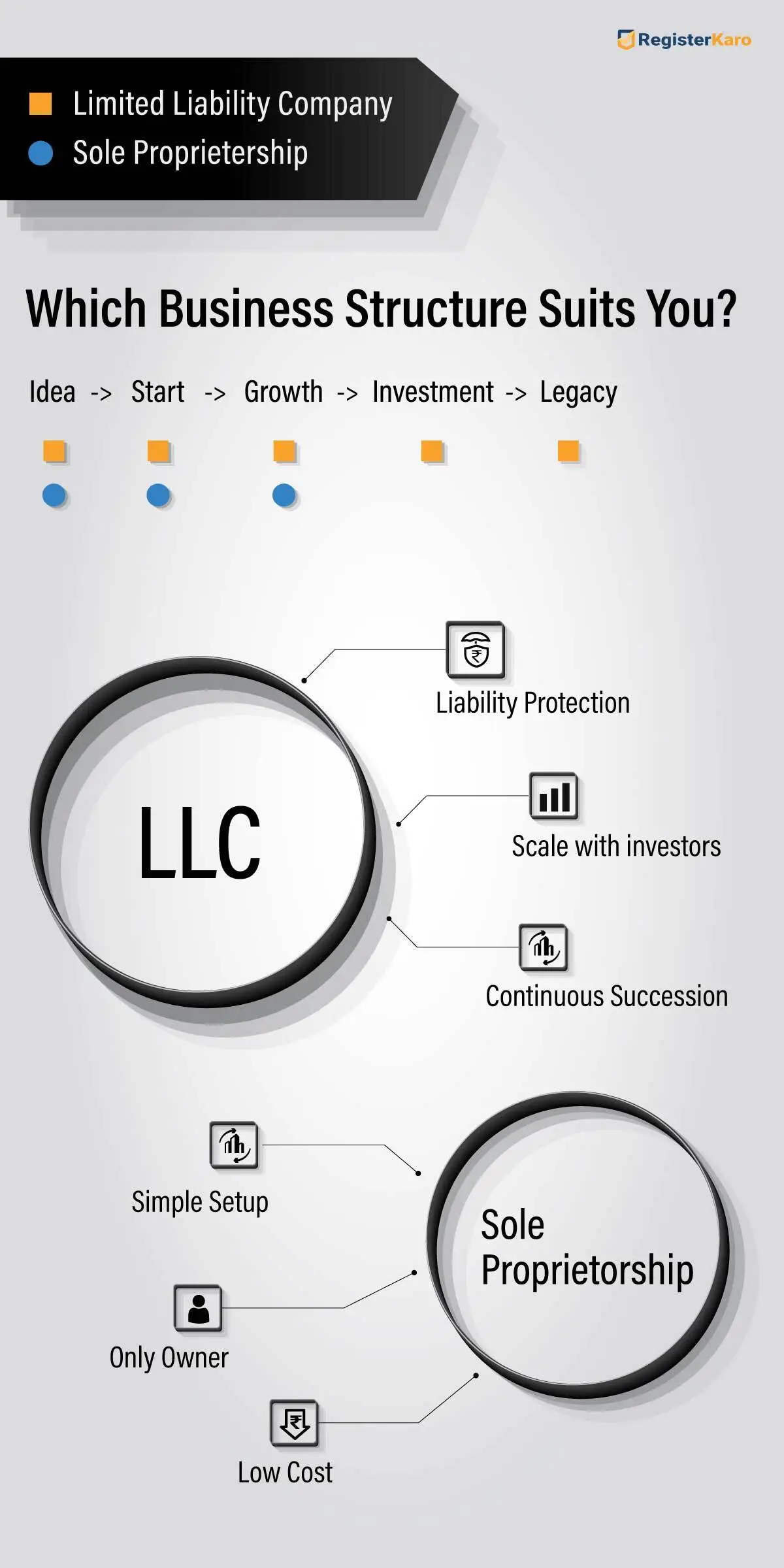

LLC vs Sole Proprietorship: How to Decide What’s Best for You?

Choosing between a Limited Liability Company and a Sole Proprietorship depends on your business goals and your risk appetite.

- If you’re looking for simplicity and control, a sole proprietorship may be the way to go.

- However, if you plan on scaling your business, seeking investment, or needing liability protection, an LLC is a more suitable choice.

Questions to Consider

- Do you want personal asset protection?

If yes, an LLC offers this protection, unlike a sole proprietorship.

- Is your business expected to grow?

An LLC offers scalability that a sole proprietorship may not.

Example

A budding entrepreneur looking to establish a neighborhood café might opt for a sole proprietorship because of its ease and reduced expenses. In contrast, a proprietor of an online retail business aiming for growth would find an LLC structure more advantageous for liability protection and tax adaptability.

Single Member LLC and the Indian One Person Company (OPC)

A Single Member LLC (SMLLC) in the US combines the simplicity of a sole proprietorship with the liability protection of an LLC — it has one owner but full corporate-style asset protection.

India’s closest equivalent is the One Person Company (OPC) — introduced under Section 2(62) of the Companies Act, 2013, specifically to give solo founders the benefits of a Private Limited Company without needing co-founders. An OPC offers:

- Limited liability — same protection as a Private Limited Company

- Separate legal entity — your personal assets stay protected

- One shareholder + one director — both can be the same person

- Mandatory nominee — required at incorporation to take over if the founder dies or becomes incapacitated

- Corporate tax rate — taxed at corporate rates (22% under Section 115BAA), not personal slab rates

For Indian solo entrepreneurs who like the SMLLC concept, OPC is the closest equivalent. For service-based solo founders, an LLP with a sleeping designated partner can also work.

Comparison Table: Sole Proprietorship vs LLC (with Indian Equivalents)

| Feature | Sole Proprietorship | US LLC | Indian Equivalent of LLC |

|---|---|---|---|

| Liability Protection | None — owner personally liable | Yes — members protected | LLP / Pvt Ltd — limited liability |

| Taxation | Personal income tax | Flexible — pass-through or corporate | LLP: flat 30%; Pvt Ltd: 22%/25%/30% |

| Ownership | Single owner | Single or multiple members | LLP: 2+ partners; Pvt Ltd: 2+ shareholders; OPC: 1 |

| Setup Cost | Minimal — basic registrations | US state filing fee ($50–$500) | LLP: ₹6K–₹15K; Pvt Ltd: ₹6K–₹30K |

| Ongoing Compliance | Minimal (GST/ITR only) | State annual report + EIN filings | LLP: Form 11 + Form 8; Pvt Ltd: MGT-7 + AOC-4 |

| Business Scalability | Limited | Excellent | Excellent (LLP/Pvt Ltd) |

| Legal Separation | None | Yes — separate legal entity | Yes (LLP and Pvt Ltd) |

| Raising Capital | Limited to personal funds/loans | Easy — issue membership interests | LLP: limited; Pvt Ltd: equity, ESOP, VC |

| Perpetual Succession | No — ends with owner | Yes | Yes (LLP and Pvt Ltd) |

| Best For | Solo freelancers, low-risk ventures | US-based scaling businesses | LLP for service firms; Pvt Ltd for startups raising funds |

When to Convert from Sole Proprietorship to LLC (or LLP / OPC / Pvt Ltd in India)

Sole proprietorships are excellent starting points, but rarely the right long-term home for a growing business. Consider converting when:

- Your business carries financial or legal risk — contracts above ₹10 lakh, employees on payroll, or any product liability exposure

- You’re approaching the ₹1 crore turnover mark — tax audit obligations under Section 44AB kick in regardless of structure

- You’re planning to raise outside investment — VCs and angels do not fund sole proprietorships

- You want to issue ESOPs or equity — only possible through corporate structures

- You’re hiring senior talent — registered structures look more credible to executive candidates

In the US, convert to an LLC by filing Articles of Organisation with your state’s Secretary of State and obtaining an EIN from the IRS.

In India, convert to a Private Limited Company under Section 366 of the Companies Act, 2013, an LLP under the LLP Act, 2008, or an OPC if you’re a solo founder. Each conversion requires NOC from any existing creditors, fresh PAN, fresh GST registration, and transfer of bank accounts and contracts.

In conclusion, the choice between a sole proprietorship and an LLC depends on your business goals, risk tolerance, and growth plans. Sole proprietorships are great for solo entrepreneurs starting small, but LLCs provide protection, scalability, and tax flexibility that are better suited for businesses that plan to expand.

For further assistance, RegisterKaro is here to help you make the best decision and register your business hassle-free! Contact Us now!