")

Did you know that over 2.5 million businesses and professionals in India comply with Section 44AB of the Income Tax Act requirements annually? Authorities in the tax department analyze the reports to confirm that high-turnover companies are tax-compliant.

So, if your business turnover is coming close to the set limits, don’t worry. Being familiar with section 44AB of the Income Tax Act will ease the way you handle an audit. It carefully explains everything there is to know about tax audit requirements.

What is Section 44AB of the Income Tax Act?

Section 44AB of the Income Tax Act refers to the mandatory tax audit provision for businesses and professionals. This audit verifies your financial records through a qualified chartered accountant.

Key aspects of this section:

- It ensures accuracy in reporting taxable income

- The CA examines your books of accounts thoroughly

- The audit confirms compliance with tax laws

The tax law requires an annual audit of accounts for the taxpayers named in section 44AB of the Income Tax Act bare act. Following this rule ensures that businesses are open with their finances and more likely to comply with taxes. As a verification process, the department uses the provision to confirm that all individuals are honest in reporting their money and taxes.

Applicability of Section 44AB

When you receive a notice about an income tax audit under Section 44AB, it’s important to know if it applies to you. The applicability of section 44AB depends on your business category and annual turnover.

Entities covered under this provision:

- Individuals and HUFs running businesses

- Partnership firms and LLPs

- Companies and other business entities

- Professionals like doctors, lawyers, and architects

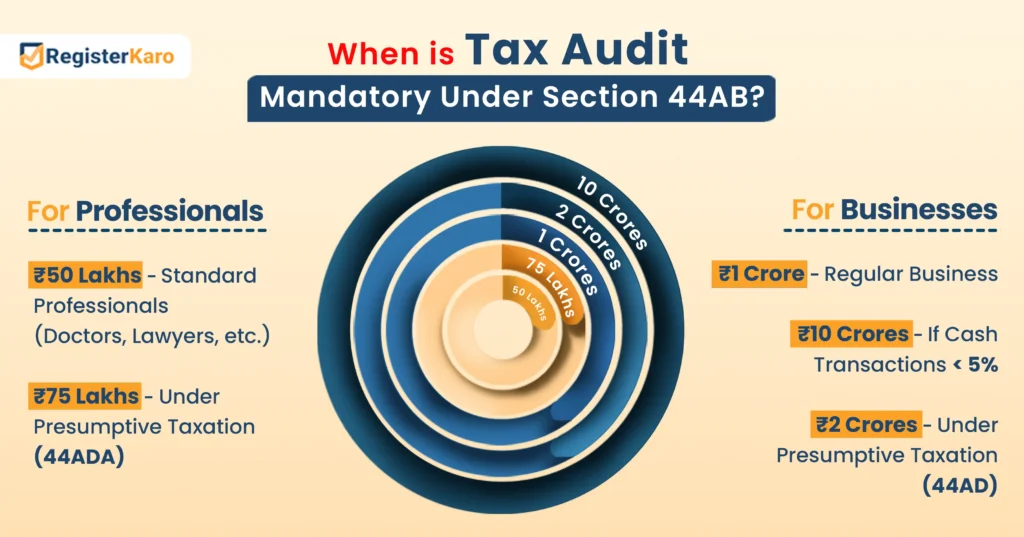

Section 44AB Turnover Limit

The current section 44AB turnover limit applies differently based on your business type:

For Businesses:

- Rs. 1 crore for general businesses

- Rs. 10 crores if cash receipts/payments are below 5% of the total

- Rs. 2 crores for businesses opting for presumptive taxation under 44AD

For Professionals:

- Rs. 50 lakhs for professionals like doctors, lawyers, and architects

- Rs. 75 lakhs for professionals opting for presumptive taxation under 44ADA

Section 44AB includes the First and Third Proviso

First Proviso: If a business receives or pays cash for less than 5% of its transactions, the First Proviso permits it to have an increased threshold of ₹10 crore.

Third Proviso: Third Proviso to Section 44AB explains that the limit will come into effect if the aggregate cash transactions are less than 5% of the total sales or purchases.

Tax Audit Procedure Under Section 44AB

If a company’s annual turnover goes above the thresholds mentioned in Section 44AB, it must be audited. Complying with the requirement helps maintain your accounts correctly and ensures your income is properly reported to the tax office.

Appointment of Auditor

The first step towards a tax audit under section 44AB involves appointing a qualified chartered accountant. Choose a CA with expertise in your business domain.

Important considerations:

- The CA must hold a valid certificate of practice

- Appoint the auditor well before the due date

- Ensure they understand your industry-specific requirements

Documentation Required for Section 44AB Audit

Proper documentation makes your tax audit under section 44AB smooth and hassle-free. Have these ready before your auditor arrives:

- Complete books of accounts with all entries

- Bank statements for all business accounts

- GST returns filed during the financial year

- TDS returns and certificates

- Previous year’s financial statements

- Fixed asset register with depreciation details

- Stock register with closing inventory valuation

Missing documents can delay your audit and risk missing submission deadlines. Organize everything systematically for efficient verification.

Preparation of Form 3CA/3CB and 3CD

For the income tax audit section 44AB, your CA must prepare and file specific forms:

Form 3CA:

- Used when a statutory audit is required under other laws

- Applicable for companies and certain specified entities

Form 3CB:

- Used when no statutory audit is required

- Common for individuals, partnerships, and small businesses

Form 3CD:

- Comprehensive annexure with 44 clauses

- Contains detailed business and financial information

- Section 44AB clause E requires specific reporting of brought forward losses

Your CA will digitally sign these forms before submitting them along with your ITR. The section 44AB requirements must be fulfilled precisely in these forms.

Due Dates for Section 44AB Tax Audit

Being aware of the timeline for tax audit under section 44AB prevents you from paying penalties. Mark these important dates:

September 30: Standard due date for filing tax audit report

October 31: Due date for filing ITR with tax audit report

November 30: Extended deadline for transfer pricing cases

The Income Tax Department occasionally extends these deadlines. However, don’t rely on extensions and plan your audit well in advance.

Late filing triggers section 44AB penalty provisions. The department monitors compliance through its automated system.

Section 44AB Penalty for Non-Compliance

Failing to comply with section 44AB of the Income Tax Act triggers penalties. Know what you might face:

- Rs. 1.5 lakhs or 0.5% of turnover, whichever is lower

- Potential disallowance of certain expenses and deductions

- Higher scrutiny in subsequent assessment years

- Interest charges on additional tax liability

The section 44AB penalty applies under section 271B of the Act. You can request a waiver only for reasonable causes like serious illness or natural calamities.

Special Provisions: Section 44AB(a) for Regular Businesses

Section 44AB Clause E

Section 44AB clause E deals with reporting requirements for brought forward losses. Your CA must report:

- Amount of loss brought forward from previous years

- Assessment year from which losses are carried forward

- Section under which losses were originally computed

This provision helps the tax department track loss adjustment claims. Many taxpayers overlook the section 44AB clause E and face scrutiny.

Proper documentation of past losses makes this reporting easier. Ensure your CA completes this section accurately.

Section 44AB A

Section 44AB is aimed at businesses that do not want to use the presumptive taxation schemes.

Under this provision:

- Regular businesses must maintain proper books of accounts

- All transactions must have supporting documentation

- Income computation follows normal accounting principles

The section 44AB requirements differ from other presumptive taxation sections. This makes many small businesses liable for audit under section 44AB.

If your turnover exceeds the threshold, compulsory tax audit under section 44AB applies regardless of profit margins.

Recent Amendments in Section 44AB

A recent amendment in section 44AB of the Income Tax Act has significantly changed audit requirements. Key changes include:

- Increased turnover threshold from Rs. 1 crore to Rs. 10 crores for businesses with limited cash transactions.

- Modified section 44AB limit for professionals from Rs. 25 lakhs to Rs. 50 lakhs.

- Introduced a 5% cash transaction limit rule to promote digital payments.

- Changed reporting requirements for section 44AB for professionals.

These amendments aim to reduce the compliance burden on small businesses. The government regularly updates section 44AB of the Income Tax Act to align with broader economic policies.

Stay updated with the latest amendments in section 44AB of the Income Tax Act through official notifications.

Practical Tips for Section 44AB Compliance

Follow these practical tips to ensure smooth compliance with section 44AB of the Income Tax Act:

- Maintain daily books of accounts without backdating entries.

- Reconcile bank statements with your books monthly.

- Track your turnover throughout the year to anticipate audit requirements.

- Keep digital backups of all financial documents.

- Implement accounting software for better record-keeping.

- Engage with your CA at least quarterly for guidance.

- Review your gross receipts under section 44AB regularly.

These practices make the tax audit under section 44AB process easier. They also strengthen your financial management system overall.

Facing problems with tax audit under section 44AB? Contact our expert team today for specialized assistance!