Dissolution of Partnership Firm in India: Modes, Steps, Format

The dissolution of a partnership firm is the complete legal closure of a partnership business under the Indian Partnership Act, 1932. It permanently ends the firm’s legal existence — partners must execute a dissolution deed, settle all accounts in the order prescribed by Section 48, publish a public notice under Section 45, file a Section 63 intimation with the Registrar of Firms, cancel GST and other registrations, and file final tax returns. The Act recognises five legal modes of dissolution (Sections 40–44). A straightforward dissolution takes 2–4 weeks; complex closures with disputes or multiple registrations take 3–6 months.

At a Glance:

- Governing Law: Indian Partnership Act, 1932 (Sections 39–55)

- Five Modes: Mutual Agreement (S.40), Compulsory (S.41), Contingencies (S.42), Notice (S.43), Court Order (S.44)

- Mandatory Steps: Dissolution deed → Public notice → Section 48 settlement → Section 63 intimation → Cancel registrations → File final ITR & GSTR-10

- Liability: Partners stay personally liable until public notice is published in the Official Gazette + a local newspaper

- Timeline: 2–4 weeks (simple) / 3–6 months (complex)

Most partnership firms in India don’t fail loudly; they simply stop trading. Bank accounts go dormant, returns lapse, and partners assume the business is “closed.” But unless the firm is legally dissolved under the Indian Partnership Act, 1932, every partner stays personally liable for the firm’s debts, tax demands, and statutory dues — sometimes years after operations end.

A critical distinction to understand upfront: dissolution of a partnership firm is not the same as reconstitution. When one partner retires, and the others continue, the firm only reconstitutes; it does not dissolve. Dissolution occurs only when all partners end the business, and the firm ceases to exist as a legal entity. If you are unsure whether your situation calls for dissolution or reconstitution, our experts at Partnership Firm Registration can help you decide before you take an irreversible step.

If you are wondering how to close a partnership firm without leaving residual liability, the answer is to follow the Indian Partnership Act, 1932 procedure end-to-end. This guide walks through it step by step, the five legal modes, documents required, dissolution deed format, procedure, tax and accounting treatment, consequences under Sections 45–55, and post-dissolution compliance.

What is the Dissolution of a Partnership Firm?

Dissolution of a partnership firm is the legal process by which a firm permanently stops all business operations, settles its accounts, and ceases to exist as a legal entity.

Section 39 of the Indian Partnership Act, 1932, defines it clearly: the dissolution of a partnership between all partners of a firm constitutes the dissolution of the firm itself. Once dissolved, the firm cannot enter into any new transactions. It can only wind up: sell assets, pay off debts, and distribute whatever remains among the partners.

Dissolution of Partnership vs Dissolution of Partnership Firm

These two terms sound similar but carry very different legal meanings. Confusing them is one of the most common mistakes partners make during closure.

| Basis | Dissolution of Partnership | Dissolution of Partnership Firm |

|---|---|---|

| Meaning | Change in the relationship between partners | Complete closure of the firm and its business |

| Does the firm continue? | Yes — remaining partners reconstitute and carry on | No — the firm ceases to exist entirely |

| Example | One partner retires; others continue under the same name | All partners agree to shut the business down permanently |

| Legal effect | Partners draw up a new partnership agreement | Partners settle all accounts and cancel all registrations |

| Governed by | Sections 40–43, Indian Partnership Act, 1932 | Section 39, Indian Partnership Act, 1932 |

A change in the composition of partners constitutes a reconstitution of the firm, whereas the complete cessation of business operations amounts to dissolution.

Who is Affected by the Dissolution of a Partnership Firm?

Dissolution creates legal and financial obligations for multiple stakeholders, not just the partners:

Tax authorities require the firm to file final income tax returns, cancel its GST registration, and settle all outstanding statutory dues.

- Partners remain personally liable for all pre-dissolution debts until the firm publishes a public notice of dissolution.

- Creditors and lenders must be paid in full before partners can recover any capital.

- Employees’ employment contracts are terminated, and the firm must immediately clear all pending dues.

- Clients and customers may find existing contracts lapsed or requiring formal transfer to another entity.

What are the Reasons for the Dissolution of a Partnership Firm?

Partnership firms dissolve for a wide range of reasons; some are planned well in advance, while others are triggered by unexpected events. The Indian Partnership Act, 1932, recognizes both voluntary and involuntary grounds for dissolution. Here are the most common reasons:

| # | Reason | Type | Statutory Reference |

|---|---|---|---|

| 1 | Mutual disagreement among partners | Voluntary | Section 40 |

| 2 | Completion of the specific venture | Contingency | Section 42(b) |

| 3 | Expiry of the fixed term in the deed | Contingency | Section 42(a) |

| 4 | Continuous business losses | Court Order | Section 44(f) |

| 5 | Death of a partner | Contingency | Section 42(c) |

| 6 | Insolvency of a partner | Contingency | Section 42(d) |

| 7 | Business becomes illegal | Compulsory | Section 41 |

| 8 | Wilful misconduct or breach of agreement | Court Order | Section 44(c)/(d) |

| 9 | Transfer of partner interest to a third party | Court Order | Section 44(e) |

| 10 | Just and equitable grounds | Court Order | Section 44(g) |

If you are considering Partnership Firm Registration instead of closing the firm, explore your options before making a final decision.

Modes of Dissolution of a Partnership Firm (Sections 40–44)

The Indian Partnership Act, 1932, recognizes five legally valid modes through which partners can dissolve a firm. Each mode applies to different circumstances and carries its own legal requirements.

1. Dissolution by Mutual Agreement: Section 40 (Voluntary Dissolution)

This is the simplest and most common mode. Under Section 40, all partners mutually agree to dissolve the firm, either by deciding so at any time during the partnership or through a clause already included in the original partnership deed. Because all parties consent, this method avoids disputes and allows partners to control the timeline and terms of closure.

Partners typically execute a dissolution deed to formally record the decision, settle accounts, and distribute assets.

Key requirement: The consent of all partners is mandatory. The Madras High Court confirmed this in Ramesh Kumar v. Smt. Latha Devi & Ors. (2007), in the absence of any agreement to the contrary, unanimous consent is compulsory.

2. Compulsory Dissolution: Section 41

Section 41 mandates dissolution by operation of law, meaning it happens automatically, regardless of whether the partners want it or not.

The Insolvency and Bankruptcy Code, 2016 (Act 31 of 2016), excluded the insolvency ground from Section 41. The insolvency of a partner is treated as a contingency under Section 42(d). Partners can contractually agree in the partnership deed to continue the firm despite a partner’s insolvency.

The only remaining ground for compulsory dissolution under Section 41 is:

The business becomes unlawful if a change in law or circumstances makes the firm’s activity illegal; the firm must dissolve compulsorily.

Important exception: If the firm runs multiple businesses and only one activity becomes unlawful, Section 41 requires dissolution only in respect of that unlawful activity. The firm may continue its other lawful operations.

3. Dissolution on Contingencies: Section 42

Section 42 triggers dissolution automatically when certain predefined events occur, unless the partnership deed explicitly states otherwise. These contingencies include:

- Expiry of fixed term: The firm was constituted for a specific period, and that period has ended.

- Completion of a specific venture: The firm was formed to complete one project, and that project is now finished.

- Death of a partner: The death of a partner triggers dissolution unless the deed allows continuation with the remaining partners or the legal heir.

- Insolvency of a partner: A partner adjudicated as insolvent can no longer legally participate,

Note: Partners can override most of these contingencies through their partnership deed. For example, they may include a clause allowing the firm to continue despite the death of a partner.

4. Dissolution by Notice of Partnership at Will: Section 43

A partnership at will is one formed for no fixed term and with no specific venture in mind. Under Section 43, any single partner can dissolve such a firm simply by serving a written notice to all other partners expressing the intention to dissolve.

Effective date of dissolution:

- If the notice specifies a date, dissolution takes effect from that date.

- If no date is mentioned, dissolution takes effect from the date the other partners receive the notice.

Legal point: The Supreme Court clarified in Banarsi Das v. Kanshi Ram, AIR 1963 SC 1165, that merely filing a suit for dissolution does not count as a notice under Section 43. The effective date of dissolution is the date of the court’s preliminary decree, not the date of filing.

5. Dissolution by Court Order: Section 44

When partners cannot resolve disputes among themselves, any one partner can file a suit in court and request dissolution. The court holds the power to dissolve the firm under Section 44 on any of the following grounds:

- A partner becomes mentally incapacitated due to insanity or unsoundness of mind, making them unable to perform their duties.

- A partner suffers from a permanent physical or other incapacity that prevents them from fulfilling their role.

- A partner engages in misconduct that negatively affects the firm’s business or reputation (in Pearce v. Foster, speculation in cotton by a partner was held to constitute misconduct justifying dissolution).

- A partner persistently breaches the partnership agreement, making it impractical for others to continue the business.

- A partner transfers their entire interest in the firm to a third party without the consent of the other partners.

- The firm incurs continuous losses and cannot operate viably, making continuation purposeless.

- The court finds any other just and equitable reason for dissolution, including a complete deadlock in management.

Important: A court can only dissolve a registered partnership firm. An unregistered firm cannot seek dissolution through court intervention.

Five Modes of Dissolution at a Glance

| Mode | Section | Trigger | Consent Needed | Court Involved? |

|---|---|---|---|---|

| Mutual Agreement | S.40 | Voluntary decision by all partners | All partners | No |

| Compulsory | S.41 | Business becomes unlawful | None — automatic | No |

| Contingencies | S.42 | Term expiry, project completion, death, insolvency | Default rule (overridable by deed) | No |

| Notice (Partnership at Will) | S.43 | One partner serves a written notice | Single partner only | No |

| Court Order | S.44 | Disputes, misconduct, deadlock, losses | Court decree | Yes — registered firms only |

Which Documents are Required for the Dissolution of a Partnership Firm?

Dissolving a partnership firm requires proper documentation to ensure legal compliance and a smooth closure. The key documents typically include:

| # | Document | Purpose |

|---|---|---|

| 1 | Original partnership deed + amendments | Establishes original terms and any reconstitutions |

| 2 | Dissolution deed (signed & notarised) | Records the dissolution decision and terms |

| 3 | Written resolution / consent of all partners | Proof of unanimous decision |

| 4 | Written notice (for partnership at will) | Required under Section 43 |

| 5 | PAN card of the firm and all partners | Identity & tax verification |

| 6 | Aadhaar card of all partners | Identity proof |

| 7 | Registered office address proof | Rent agreement / ownership document + utility bill |

| 8 | NOC from landlord (if rented premises) | Permission for use as registered office |

| 9 | Final balance sheet & P&L up to dissolution date | Statutory financial closure |

| 10 | Statement of pending litigations (if any) | Disclosure of legal exposure |

| 11 | Public notice — newspaper clipping + Official Gazette copy | Section 45 compliance |

| 12 | Intimation to Registrar of Firms | Section 63 filing |

| 13 | GST REG-16 + GSTR-10 acknowledgement | GST cancellation & final return |

| 14 | Cancellation certificates — MSME, IEC, EPF, ESI, trade licence | Closure of all linked registrations |

If a firm has all these documents, it can dissolve smoothly without any legal complications or delays.

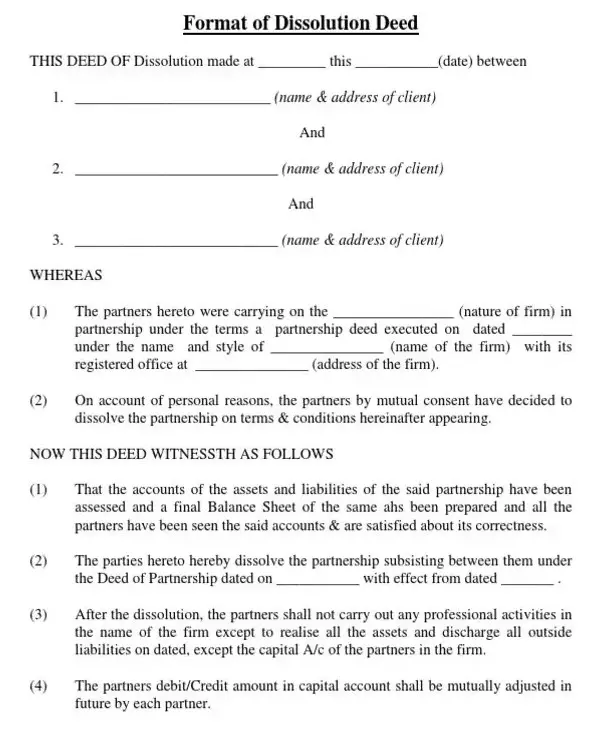

Dissolution Deed of Partnership Firm: Format and Key Clauses

A dissolution deed of a partnership firm is the foundational document that records every partner’s agreement to close the firm. It must be executed on appropriate stamp paper (state-dependent) and notarised. While the Indian Partnership Act, 1932, does not prescribe a fixed format, a valid dissolution deed should contain:

| Clause | What It Covers |

|---|---|

| Parties & recital | Names, addresses, and PAN of all partners + reference to the original partnership deed |

| Effective date of dissolution | The exact date from which the firm stands dissolved |

| Reason for dissolution | Mutual agreement / expiry of term / completion of venture, etc. |

| Settlement of accounts | Order of payment as per Section 48 — outside debts → partner loans → capital → profit-share distribution |

| Asset distribution | How tangible and intangible assets (including goodwill under Section 55) will be allocated |

| Liability indemnity | Cross-indemnity among partners for pre-dissolution debts |

| Public notice undertaking | Commitment to publish under Section 45 |

| Tax & registration cancellation | Responsibility for filing final ITR, GSTR-10, and cancelling other registrations |

| Mutual release & dispute resolution | Release of future claims; jurisdiction or arbitration clause |

| Signatures & witnesses | All partners’ signatures + 2 witnesses |

Once executed, retain the original with each partner and a notarised copy with the Registrar of Firms (for registered firms).

What is the Procedure for Dissolution of a Partnership Firm in India?

Here is the complete step-by-step process to dissolve a partnership firm in India legally:

Step 1: Take the decision to dissolve: All partners record the decision formally through mutual resolution, written notice, or court order.

Verbal agreement isn’t enough.

Step 2: Execute the dissolution deed: All partners sign a stamped, notarized dissolution deed recording the effective date, asset distribution, liability settlement, and mutual release clauses.

Step 3: Publish a public notice: Partners must publish a dissolution notice in the Official Gazette and a local newspaper. Under Section 45 read with Section 72 of the Indian Partnership Act, 1932, partners remain personally liable to third parties until they issue this notice.

Step 4: Settle all accounts (Section 48 order): The firm first pays third-party creditors, followed by repayment of partner loans and return of partner capital. Any remaining balance is then distributed among the partners in their profit-sharing ratio.

Step 5: Intimate the Registrar of Firms (Section 63): Registered firms must file a dissolution notice with the Registrar of Firms under Section 63. Most states, including Maharashtra, mandate this within 90 days. The form and procedure vary state by state.

Step 6: Cancel all registrations: File GST REG-16 to apply for GST cancellation, then file GSTR-10 (final return) within 3 months of the cancellation order. Also cancel PAN, TAN, trade licence, MSME, IEC, EPF, and ESI registrations.

Step 7: File all pending tax returns: File the firm’s final ITR and all pending GST returns before closing tax accounts.

Step 8: Close the firm’s bank accounts: Submit the dissolution deed and no-dues certificate to the bank to formally close all firm accounts.

Cost and Timeline for Dissolving a Partnership Firm

Estimated Cost:

| Cost Component | Approximate Range (₹) |

|---|---|

| Stamp duty on dissolution deed (state-dependent) | 500 – 2,000 |

| Notary charges | 200 – 500 |

| Public notice publication (Gazette + newspaper) | 1,500 – 5,000 |

| Section 63 filing fees (Registrar of Firms) | 100 – 500 |

| GST cancellation + GSTR-10 filing | 0 – 1,000 (govt) + professional fees |

| Professional fees (CA / lawyer) | 5,000 – 25,000 |

| Total estimated cost | ₹7,000 – ₹35,000 |

Estimated Timeline:

| Scenario | Working Days |

|---|---|

| Simple dissolution (no disputes, single registration) | 2 – 4 weeks |

| Multiple registrations (GST, MSME, IEC, EPF) | 4 – 8 weeks |

| Disputed accounts or court-ordered dissolution | 3 – 6 months |

| Pending litigation or tax assessments | 6 – 12 months |

What are the Consequences of Dissolution of a Partnership Firm?

Dissolution does not immediately end the firm; it triggers legal, financial, and operational consequences under Sections 45 to 55 of the Indian Partnership Act, 1932. Partners must understand these provisions before starting the process:

- The firm ceases to exist as a legal entity and cannot enter into new contracts, or sue or be sued in its name.

- Under Section 45, partners remain jointly liable to third parties for any act done in the firm’s name after dissolution until they publish a public notice. The estate of a deceased or insolvent partner is not liable for acts performed after they cease to be a partner.

- Under Section 46, every partner has the right to ensure that the firm’s assets are applied toward settling debts and that any surplus is distributed according to their rights.

- Under Section 47, each partner retains authority only to complete winding-up activities and cannot bind the firm in any new business.

- Under Section 50, any profit a partner earns from a firm-related transaction after dissolution must be shared with all other partners.

- Under Section 51, a partner who paid a premium to join a fixed-term firm is entitled to a refund if the firm dissolves before the term ends, unless the dissolution results from that partner’s misconduct or the death of a partner.

- Under Section 53, no partner can use the firm’s name or property for personal benefit until the winding-up process is fully completed.

- Under Section 55, goodwill forms part of the firm’s assets and must be included in the settlement of accounts.

- Under Section 189 of the Income Tax Act, 1961, every ex-partner remains jointly and severally liable for all taxes, penalties, and dues payable by the firm.

- Upon dissolution, all employment contracts and client agreements terminate, and the firm must clear all pending salaries and statutory dues before closure.

Tax Implications and Accounting Treatment of Dissolution of Partnership Firm

Dissolution triggers specific obligations under the Income Tax Act, 1961 and accounting requirements that partners must address before closure.

Tax obligations:

- Section 189, Income Tax Act, 1961: Every ex-partner remains jointly and severally liable for taxes, penalties, and dues even after dissolution.

- Section 45(4): Distribution of capital assets to partners on dissolution is treated as a transfer; capital gains tax may apply.

- Final ITR: File the firm’s final return for the year of dissolution within the due date.

- GST closure: File GST REG-16 (cancellation application) and GSTR-10 (final return) within 3 months of cancellation.

- TDS reconciliation: Issue Form 16/16A to employees and contractors before closure.

Accounting treatment:

- Realisation Account: Open to record the sale of assets and payment of liabilities.

- Partner’s Capital Account: Adjust for accumulated profits, drawings, and revaluation.

- Section 48 order of settlement: External liabilities → partner loans → partner capital → profit/loss share.

- Goodwill: Must be valued and treated as an asset under Section 55 unless the deed says otherwise.

Common Mistakes to Avoid During Dissolution of a Partnership Firm

Most dissolution issues arise from procedural lapses rather than legal complexity. These common mistakes can expose partners to future liability, penalties, and disputes:

- Under Section 45 read with Section 72, partners remain personally liable for all acts of the firm until they publish a public notice in the Official Gazette and a local newspaper. A signed dissolution deed alone does not discharge this liability.

- Partners who distribute assets before settling third-party debts become personally liable for those unpaid obligations. Section 48 prescribes a mandatory order of settlement that partners must follow.

- Failure to file GSTR-10 after GST cancellation can lead to penalties and notices even years after the firm has ceased operations.

- Registered firms that do not file a dissolution notice under Section 63 continue to appear as active in government records, creating ongoing compliance obligations.

- A verbal agreement to dissolve has no legal validity. Partners must document the dissolution in writing and retain proof of execution and delivery.

- Leaving GST, trade licenses, MSME, or EPF registrations active after dissolution results in continued tax demands and regulatory notices in the firm’s name.

Properly understanding these consequences ensures partners can close the firm efficiently and remain compliant with legal obligations.

Closing a partnership firm correctly protects each partner from years of residual liability. If you are unsure about the dissolution deed, public notice format, Section 48 settlement order, or GST/ITR closure, RegisterKaro’s experts handle the entire process end-to-end. We also help businesses considering an alternative structure: many firms restructure rather than dissolve, especially when one or more partners want to continue operations. Talk to a RegisterKaro expert.