Many businesses miss statutory deadlines like annual returns, AGM requirements, or ROC filings due to operational pressure. These delays often trigger legal proceedings under the Companies Act, 2013, and create financial as well as reputational risks. To handle these situations, the law provides a practical solution known as the compounding of offenses.

This process allows companies and their officers to resolve specific compliance defaults by paying a prescribed amount instead of facing court proceedings. Section 441 of the Companies Act, 2013, governs this process and enables companies to fix compliance issues quickly while avoiding unnecessary litigation. It also supports smoother business operations by offering a structured legal remedy.

This guide explains the meaning of compounding of offenses, eligible violations, ineligible offenses, authorities, procedure, and legal consequences.

What is Compounding of Offenses Under Section 441 of the Companies Act 2013?

Compounding of offenses under the Companies Act 2013 is a legal process that settles compliance violations without prosecution. A company or its officers pays a prescribed amount to the competent authority instead of facing criminal proceedings.

The National Company Law Tribunal (NCLT) or the Regional Director handles such cases depending on the offense category and penalty limit. Once the authority approves compounding, the case closes permanently for that specific violation.

This process helps companies correct compliance errors and avoid court trials for minor or procedural defaults. The Registrar of Companies cannot reopen proceedings for the same offenses once they have been compounded.

Section 441 of the Companies Act 2013 governs this mechanism. It was notified with effect from 1 June 2016 and replaced Section 621A of the Companies Act 1956. The objective is clear: reduce the burden on courts and tribunals, and encourage voluntary compliance.

After receiving the compounding order, the company must complete compliance within the specified timeframe, typically within 30 to 60 days.

Which Offenses Can Be Compounded Under the Companies Act 2013?

Section 441(1) of the Companies Act, 2013 allows compounding of specific offenses based on their nature and penalty structure. The law provides a list of compoundable offences under the Companies Act, 2013, and classifies them into 2 clear categories to simplify compliance resolution:

Category 1: Offenses Punishable with Fine only

Companies can directly compound offenses that attract only monetary penalties. The NCLT or the RD handles these cases without requiring Special Court approval.

Most procedural and filing-related defaults fall under this category. These offenses usually arise from delays or non-compliance with statutory timelines.

Common examples include:

- Delay in filing the annual return under Section 92

- Delay in filing financial statements under Section 137

- Failure to hold an Annual General Meeting under Section 96

- Non-maintenance of statutory registers under Section 88

- Delay in issuing share certificates under Section 56

- Failure to file a return of allotment under Section 39

- Failure to report a change of registered office under Section 12

Category 2: Offenses Punishable with Imprisonment or Fine

Certain offenses under the Companies Act carry imprisonment or fine, but not mandatory imprisonment in all cases. These offenses require approval from the Special Court before compounding.

The offender must first approach the Special Court under Section 441(6)(a). After approval, the authority allows compounding following the procedure under the Code of Criminal Procedure, 1973.

This process ensures judicial oversight in cases involving higher legal severity.

Which Offenses Cannot Be Compounded Under Section 441?

Section 441(1), Section 441(2), and Section 441(6)(b) exclude the following from compounding:

- Offenses punishable with imprisonment only: The law does not allow compounding when an offense leads only to imprisonment. Such cases always go through full legal proceedings in court.

- Offenses punishable with both imprisonment and fine mandatorily: Some offenses under the Act involve both imprisonment and fine together. These offenses cannot be handled by the NCLT or the Regional Director through compounding.

- Offenses where investigation is pending: Section 441(1) explicitly bars compounding when an investigation against the company has been initiated or is pending under the Act.

- Offenses compounded within the last three years: Under Section 441(2), if the same offense was compounded less than three years ago, it cannot be compounded again. However, if three years have passed since the previous compounding, the subsequent offense is treated as a first offense.

These rules ensure that only minor and procedural violations qualify for compounding, while serious offenses always go through proper legal action.

Authorities for Compounding: NCLT vs Regional Director

The authority that handles a compounding application depends on the maximum penalty prescribed for that offense under the Companies Act, 2013.

| Authority | When It Applies |

| Regional Director (RD) | The Regional Director handles cases where the maximum fine for the offense does not exceed ₹25 lakh. These are usually less serious procedural defaults. |

| National Company Law Tribunal (NCLT) | The National Company Law Tribunal handles cases where the maximum fine exceeds ₹25 lakh. These cases usually involve higher-value or more serious compliance violations. |

| Special Court | The Special Court handles offenses that involve imprisonment or both imprisonment and fine. In such cases, compounding happens only after court approval under Section 441(6)(a). |

How Authority is Decided?

The Registrar of Companies checks the offense details after receiving Form GNL-1. It then forwards the application to the correct authority based on the maximum fine under the law, not the actual penalty or compounding amount.

Important Legal Clarification

Companies often face confusion when the same default continues over multiple years or involves several officers. The law provides clear guidance on how to handle such situations.

A company and its defaulting officers can file a single compounding application for the same offence, even if it continues across multiple financial years. This approach helps simplify the process and avoids unnecessary duplication.

However, companies must file separate applications for different offences. For example, failure to file an annual return under Section 92 and failure to file financial statements under Section 137 require separate applications.

This position was clarified by the NCLAT in Pahuja Takii Seeds Ltd. & Ors. vs Registrar of Companies (2018). The tribunal allowed a joint application for the same offence across multiple years, confirming that the law supports a practical and streamlined approach for repeated procedural defaults.

Step-by-Step Procedure for Compounding of Offenses

To understand how compounding of offences works in practice, companies must follow a structured process:

Step 1: Identify the Default and Correct it

The company must first identify the compliance default clearly. It must correct the violation before filing the application.

If the default involves ROC filings under the Companies Act, the company must file all pending forms immediately. The company must also pay applicable late fees and additional fees under Section 403.

Authorities like the NCLT and the Regional Director require proof of rectification before considering the application. The company must attach SRN numbers, payment receipts, and filing acknowledgements as evidence.

Step 2: Convene a Board Meeting

The Board of Directors must hold a formal meeting and pass resolutions for the following actions:

- Approve filing of compounding application under Section 441.

- Authorize a director or officer to sign and submit the application on behalf of the company.

- Appoint a professional advocate, Practicing Company Secretary, or Chartered Accountant to appear before the RD or NCLT at the hearing.

This step ensures proper legal approval within the company.

Step 3: Prepare the Compounding Application

The company must prepare the compounding application in triplicate (three identical copies of the same document) and include:

- Full details of the company and the officers in default

- The specific section under which the offense occurred

- The nature and period of the default

- Steps taken to rectify the default

- The grounds for seeking compounding

Clear and complete documentation improves approval chances and helps authorities review the case without delays.

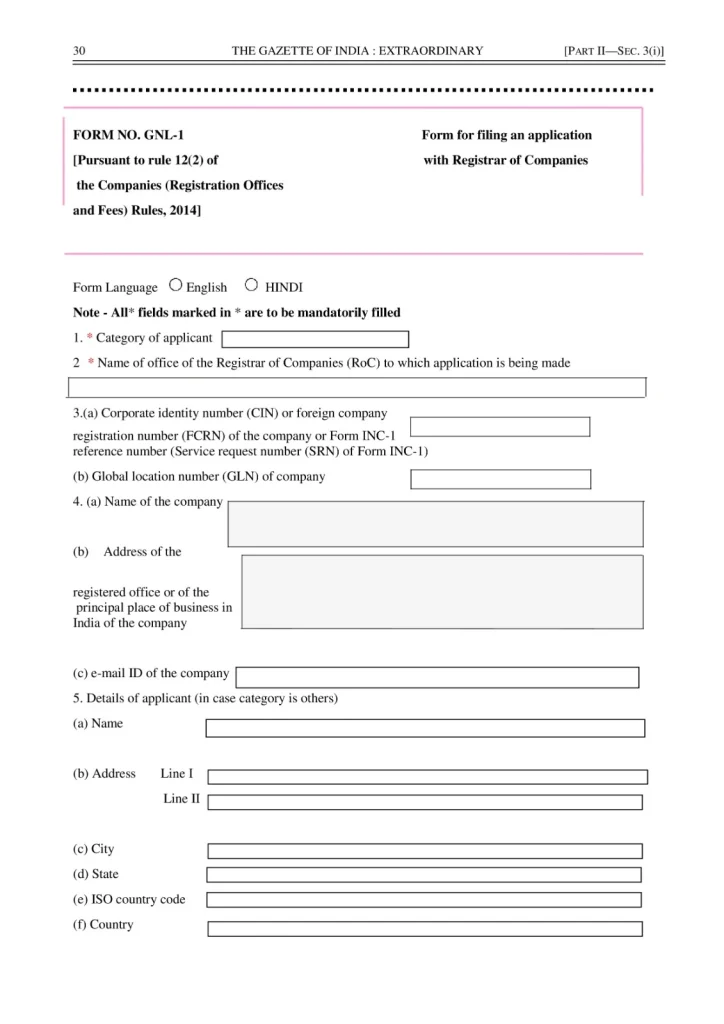

Step 4: File Form GNL-1 with the ROC

The company must file the compounding application electronically using Form GNL-1 on the MCA portal (mca.gov.in).

The government fee for filing is ₹1,000 as per the NCLT Rules, 2016. The form allows details of up to 8 individuals, excluding the company.

If more officers are involved, the company must attach additional details separately.

Documents required with the application include:

- Board resolution authorizing the application and the representative

- Affidavit verifying the facts stated in the application

- Power of attorney in favour of the authorized representative

- Memorandum of appearance from the representative

- Proof of rectification (SRN of filed forms, payment receipts)

- Financial statements of the company

- Details of the company’s shareholding and paid-up capital

- Any prior correspondence with the ROC regarding the default

Step 5: ROC Forwards the Application

After receiving Form GNL-1, the Registrar of Companies verifies the details and prepares a report. ROC then forwards the application to the NCLT or the Regional Director based on the maximum fine applicable.

This review process may take a few weeks, depending on workload and case complexity.

Step 6: Personal Hearing Before NCLT or RD

The NCLT or the Regional Director conducts a personal hearing for the case.

The company’s director, officer, or authorized representative attends the hearing and presents the case.

The authority checks:

- Whether the default is rectified

- Whether documents are complete

- Whether the explanation is valid

Note: The NCLAT has confirmed that a compounding application cannot be rejected without proper consideration and without giving reasons.

Step 7: Payment of Compounding Fee

If the NCLT or RD decides to allow compounding, it issues an order specifying the compounding fee. The fee cannot exceed the maximum fine prescribed for that offense under the relevant section of the Act. Any additional fees already paid under Section 403 are taken into account while determining the compounding fee.

The company and its officers must pay the compounding fee to the Central Government within the time specified in the order. Payment is made through the MCA portal (mca.gov.in).

Step 8: File Form INC-28 with ROC

After payment and order approval, the company must file Form INC-28 within 7 days.

This filing informs the ROC that the case has been officially closed. It updates the company’s compliance record and confirms final settlement of the offense.

What Happens After Compounding of Offenses?

After compounding of offenses under the Companies Act, 2013, the legal position depends on whether prosecution has started or not.

a. If compounding happens before prosecution

If the company completes compounding before any prosecution starts, authorities cannot initiate legal proceedings for that specific default. Section 441(3)(c) clearly provides this protection to the company and its officers.

The case is treated as fully closed once the company files Form INC-28 with the Registrar of Companies. The ROC updates the records, and the default stands resolved from that date.

b. If compounding happens after prosecution starts

If prosecution has already started, the company can still apply for compounding of offenses under the Companies Act 2013. After approval, the compounding order is submitted to the Special Court handling the case.

The court then discharges the company and its officers from the case. This action formally ends the criminal proceedings related to that default.

Consequences of Not Using Compounding

When a business, after company incorporation, ignores its compliance defaults and does not apply for compounding, the following consequences follow:

- The Registrar of Companies files a complaint before the Special Court and starts criminal prosecution against the company and its officers.

- Directors face disqualification risk under Section 164(2) if the company fails to file financial statements or annual returns for three continuous years.

- The company faces an increasing financial burden as additional fees and penalties continue to accumulate for ongoing defaults.

- Key officers such as the Managing Director, CEO, and CFO face personal liability for non-compliance under Section 203(5) of the Act.

- The company’s credibility reduces with banks, investors, and regulators, which affects future funding and business growth opportunities.

Timely use of compounding helps companies avoid these risks and maintain a clean compliance record.

Compounding vs Penalty: Key Difference

Many companies often confuse compounding of offenses with penalties, so understanding the difference is essential to choosing the right compliance approach:

| Basis | Compounding of Offenses | Penalty / Adjudication |

| Nature | The company or officer in default starts the process | Authority imposes a penalty after identifying non-compliance |

| Initiated by | The case is settled and treated as closed | ROC or MCA initiates the action |

| Authority | NCLT or the Regional Director handles the case | Adjudicating Officer under Section 454 handles the case |

| Legal proceedings | Avoids or closes prosecution for the offense | Does not automatically stop prosecution |

| Director impact | Does not lead to director disqualification | May affect directors in certain situations |

| Compliance record | An adjudicating officer under Section 454 handles the case | Penalty order remains recorded on the MCA portal |

How RegisterKaro Helps with Compounding of Offenses?

Filing a compounding application requires correct authority selection, proper documentation, and timely compliance correction. Any mistake or missing detail can delay approval or lead to rejection.

RegisterKaro manages the entire process with accuracy and professional support. We help you:

- Identify compoundable offenses and the correct authority

- Prepare and draft the application properly

- File Form GNL-1 on the MCA portal

- Handle ROC coordination and hearing representation

- File Form INC-28 within the required timeline

Get your offense resolved quickly while filing for private limited company registration or post-compliance, with expert assistance. Contact us today for end-to-end assistance with compounding applications and ROC compliance.