GSTR-9 Annual Return Filing Online in India

Avoid penalties and last-minute stress with reliable GSTR-9 return filing. Stay compliant with GST laws and ensure your business meets all regulatory requirements before the due date. What you get:

What is GSTR-9?

GSTR-9 is an annual return that GST-registered persons are required to submit at the close of every financial year. It provides a detailed summary of all GST transactions reported through monthly or quarterly returns like GSTR-1 (outward supplies) and GSTR-3B (summary return).

The form includes details of:

- Sales and purchases made during the financial year,

- Input Tax Credit (ITC) claimed and reversed,

- Taxes paid under Central Goods and Services Tax (CGST), State Goods and Services Tax (SGST), Integrated Goods and Services Tax (IGST), and Cess,

- Interest, refunds, and demand adjustments (if any).

Purpose of Filing GSTR-9

The main reasons for filing GSTR-9 are to:

- Match data: Align information reported in monthly/quarterly returns (GSTR-1 and GSTR-3B) with the taxpayer's yearly financial records.

- Ensure compliance: Provide a full yearly declaration of GST transactions with all GST laws.

- Identify discrepancies: Assist taxpayers and authorities in detecting errors or inconsistencies in previously filed GST returns.

- Summarise data: Provide a concise, unified summary of all GST transactions for the entire financial year.

Different Forms Under GSTR-9 Annual Return

While GSTR-9 is the main annual return form under GST, there are a few related forms designed for different types of taxpayers and reporting needs. Each serves a specific purpose depending on the taxpayer’s registration type, turnover, and role in the GST system.

Here’s a breakdown of the different forms:

- GSTR-9: This is the standard annual return form for regular taxpayers registered under GST. It includes consolidated details of outward and inward supplies, ITC, tax paid, and other related information for the full financial year.

- GSTR-9B: This form is an annual statement for e-commerce operators who collect Tax at Source (TCS) and file Form GSTR-8. It is intended to be a consolidated summary of all TCS collected by the operator during the financial year.

- Note: The requirement to file GSTR-9B has been deferred by the government since its introduction. Therefore, e-commerce operators are currently not required to file it.

- GSTR-9C: This is a reconciliation statement for taxpayers whose annual turnover exceeds Rs. 5 crores (applicable from FY 2020–21 onwards; earlier the limit was Rs. 2 crore).

It includes:

- A comparison between the data filed in GSTR-9 and the audited financial statements.

- The form must be self-certified by the taxpayer (audit by a CA or CMA was required earlier, but is now optional).

- Helps ensure transparency and accuracy in reporting.

Choosing the right form and understanding your GSTR-9 filing eligibility is essential to ensure error-free annual return filing under GST.

Note: GSTR-9A has been suspended and replaced by GSTR-4 for annual filing from FY 2019-20 onwards. This form is meant for taxpayers under the Composition Scheme, which allows small businesses to pay tax at a fixed rate.

Who is Required to File GSTR-9?

Most regular GST-registered taxpayers must file the GSTR-9 annual return, depending on their turnover and category.

If your annual turnover is more than Rs. 2 crore, filing GSTR-9 is mandatory. For businesses with a turnover up to Rs. 2 crore, filing GSTR-9 is optional. This rule helps smaller businesses reduce their compliance burden.

Turnover Limits for GSTR-9 Filing

| Annual Turnover | GSTR-9 Filing Requirement |

| More than Rs. 2 crore | Must file GSTR-9 |

| Rs. 2 crore or less | Filing is optional |

Exclusions from Form GSTR-9 Filing

Not all registered taxpayers are required to file GSTR-9, the annual GST return. The following categories are specifically excluded:

- Casual Taxable Persons – These are individuals or entities registered for a limited period (like for exhibitions or seasonal businesses). Since their registration is not ongoing, they are exempt from filing GSTR-9.

- Input Service Distributors (ISDs) – ISDs distribute the input tax credit to their branches or units. They don’t supply goods or services directly, so they aren’t required to file the annual return.

- Non-Resident Taxable Persons – These are foreign individuals or businesses providing goods or services in India without a permanent place of business. Due to their short-term presence, they are exempt from the annual filing.

- TCS Collectors under Section 52 of the GST Act – E-commerce operators collecting Tax Collected at Source (TCS) from suppliers are not required to file GSTR-9, as their compliance is governed under a different section.

- TDS Deductors under Section 51 of the GST Act – Government departments or agencies that deduct Tax Deducted at Source (TDS) are also excluded, as they do not engage in the regular supply of goods or services.

- Online Information Database Access and Retrieval (OIDAR) Services – OIDAR service providers supply services like software, cloud storage, or streaming to Indian consumers. They are exempt from GSTR-9 filing.

Documents Required to File GSTR-9 in India

To correctly file GSTR 9 online, you will need these documents and information:

- GSTR-1 data: Details of all sales for the financial year.

- GSTR-3B data: Summary of GST taxes owed and ITC claimed for the financial year.

- Audited Financial Statements: Profit & Loss Account and Balance Sheet, especially if you need to file GSTR-9C for reconciliation.

- Books of Accounts: Purchase and sales records, expense ledgers, and other accounting documents for cross-checking data.

- Reconciliation Statements: Documents showing any differences between your GSTR-1, GSTR-3B, and accounting books.

- ITC Register: Details of all input tax credits taken, reversed, or denied during the year.

- HSN-wise Summary: Breakdown of outward and inward supplies according to Harmonized System of Nomenclature (HSN) codes. This summary is a mandatory part of the GSTR-9 return.

Having these documents ready will help ensure a smooth and accurate GSTR-9 filing process.

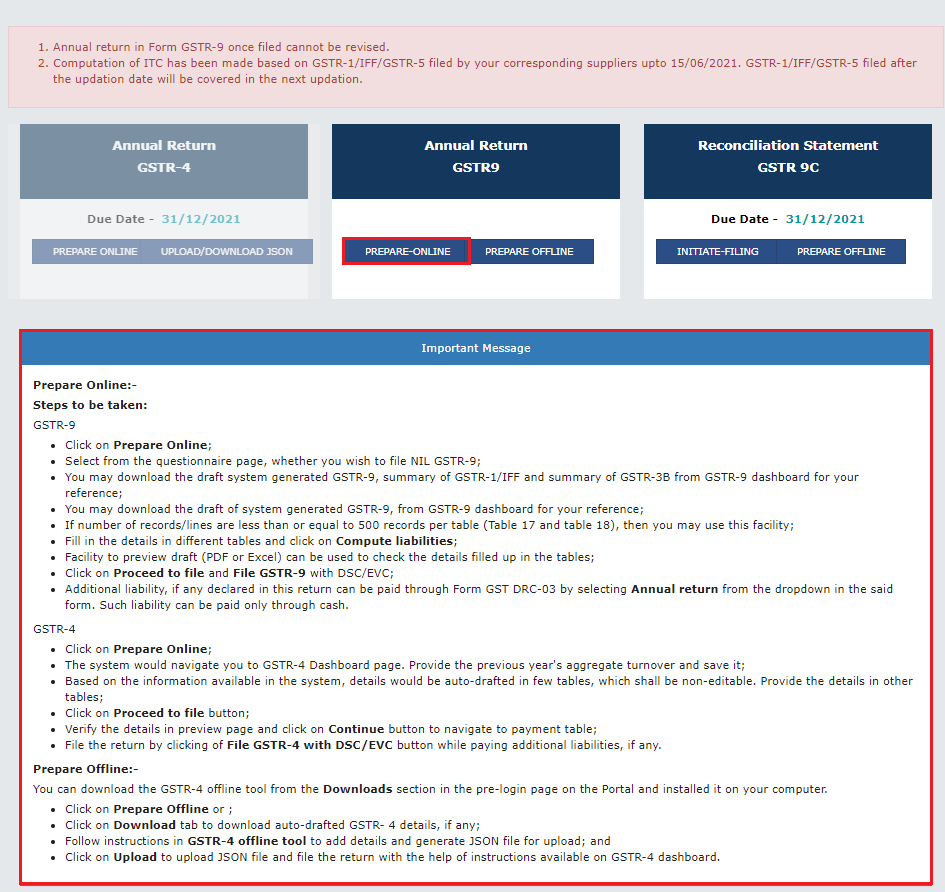

How to File GSTR 9 Online?

You must file GSTR-1 and GSTR-3B for the full financial year before filing GSTR-9. The GSTR 9 filing process involves several steps to ensure accuracy and follow the rules.

Here's how to file the GSTR 9 annual return online:

1. Log in to GST Portal: Go to the GST portal (gst.gov.in) using your login details.

2. Go to Returns Dashboard: Select the financial year for which you want to file GSTR-9.

3. Start GSTR-9 Filing: Choose "Prepare Online" or "Prepare Offline." The 'Prepare Online' option is suitable for taxpayers with a smaller volume of data.

4. Check Auto-Populated Data: The system will fill in many fields based on your filed GSTR-1 and GSTR-3B returns. Carefully check this data against your records.

5. Enter Missing Details: Manually enter any additional required information in the various tables of GSTR-9, such as:

-

- Details of sales and purchases reported during the financial year.

- Details of ITC reported, reversed, or not allowed.

- Details of tax paid, including tax due and tax paid by cash or ITC.

- Include any changes or corrections made this year for transactions from the previous financial year. These revised entries are reported in the current year's return.

- The HSN Summary is important in GSTR-9 for both sales and purchases, as this offers important data for review.

6. Calculate Taxes Due: The portal will calculate any additional tax liability.

7. Make Payment (if any): Pay any outstanding taxes or late filing fees.

8. Preview and Check: Download the draft GSTR-9 and carefully look over all the details for errors before final submission.

9. Submit the Return: Once satisfied, send the return using a Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

10. File GSTR-9C (if it applies): If your annual turnover exceeds Rs. 5 crore, file GSTR-9C after submitting GSTR-9.

Note: You must file GSTR-1 and GSTR-3B for the entire financial year before submitting GSTR-9.

GSTR-9 Return Filing Fees

There are no official fees charged by the government for filing GSTR-9 on the GST portal. Filing your annual return is free if done directly online. However, significant penalties apply for late filing or non-filing of GSTR-9. These penalties are significant and are applied to ensure on-time compliance.

If you choose to hire a GST professional or use paid software for filing, the costs generally range as follows:

- Professional Fees: Rs. 1000 to Rs. 3,000 per GSTR-9 filing, depending on the complexity and service provider.

- Paid Software Charges: Rs. 300 to Rs. 1,500, depending on the features and support offered.

These fees vary based on the service quality and volume of filings handled.

GSTR 9 Due Dates & Late Filing Penalties

The GSTR 9 filing due date is usually December 31st of the year after the relevant financial year. For example, for the financial year 2024-25, the GSTR-9 due date would be December 31, 2025. Following this GSTR 9 filing date is important to avoid penalties.

Penalty for late filing of GSTR 9 / GSTR 9 late filing fees:

- A late fee of ₹200 per day (₹100 for CGST and ₹100 for SGST) is charged for each day of delay, up to a maximum of 0.5% of the taxpayer's turnover in the State or Union Territory (0.25% for CGST and 0.25% for SGST).

- Late fees must be paid in cash. They cannot be paid using an Input Tax Credit.

- Interest at 18% per year may be charged on any outstanding tax amount. This applies only to the net tax paid in cash, not to the entire turnover.

- In cases of significant delay, these penalties can add up quickly, making it costly to miss the deadline.

Filing GSTR-9 on time helps avoid these fees and keeps your GST compliance in good standing, making future audits and assessments smoother.

Format of GSTR 9 Annual Return

The format of the GSTR-9 return is divided into several parts, each requiring specific information as per the GST rules. Generally, it covers:

- Part I: Basic Details: Financial Year, GSTIN, Official Name, Business Name.

- Part II: Details of Outward and Inward Supplies declared during the financial year: This includes taxable outward goods/services, zero-rated goods/services, exempted goods/services, and goods/services where tax is paid under reverse charge.

- Part III: Details of ITC declared in returns filed during the financial year: Information on ITC taken, ITC reversed, and net ITC available.

- Part IV: Details of tax paid as declared in returns filed during the financial year: Details of tax owed and tax paid.

- Part V: Details of previous year’s transactions reported between April and September of the current year, or up to the date of filing the previous year’s annual return, whichever comes first. This section records any changes made to last year’s transactions that are reported in the current financial year.

- Part VI: Other Information: This includes details like demands and refunds, HSN-wise summary of sales and purchases, and late fees due and paid.

The GSTR 9 annual return is a detailed document. Understanding each section is key to accurate filing. A checklist for filing GSTR 9 can be very helpful to make sure all needed details are covered and prevent common mistakes.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

Who has to file GSTR 9?

−Every registered taxpayer under GST must file a GSTR-9. Exceptions include temporary taxable persons, non-resident taxable persons, Input Service Distributors, and those who must deduct or collect TDS/TCS. It is required for businesses with total yearly sales over Rs. 2 crore.

Is it mandatory to file GSTR 9?

+What if GSTR 9 is wrongly filed?

+Is the HSN Summary important in GSTR-9?

+How many subcategories are there under GSTR 9?

+Is there any late fee if there is a delay in filing GSTR9?

+Can I file GSTR 9 after the due date?

+What is the difference between GSTR9 and 9C?

+How to check the GSTR 9 filing status?

+What are the GSTR 9 filing exemptions?

+Is there any option to file a Nil GSTR 9?

+

Reviewed by

Joel DsouzaJoel Dsouza is a Chartered Accountant (CA) and compliance expert with over 7 years of hands-on experience in company registration, tax structuring, GST, ROC filings, and MCA compliance. As a qualified member of the Institute of Chartered Accountants of India (ICAI) and Co-Founder at RegisterKaro, he has personally advised more than 1,000 startups and SMEs across India, helping founders navigate incorporation, regulatory frameworks, and financial planning from Day 1. With deep expertise across all three levels of Finance and Portfolio Management, Joel is committed to promoting financial literacy and simplifying India's startup ecosystem through clear, actionable guidance that entrepreneurs can act on immediately.

Why Choose RegisterKaro for the GSTR-9 Filing Services?

You should choose RegisterKaro for your GSTR-9 filing because we offer expert support, reliable service, and complete peace of mind. Here are the top reasons:

- CA-Reviewed Filing: Benefit from Chartered Accountant-reviewed filings that boost accuracy and compliance, reducing the risk of audits or notices.

- Hassle-Free Process: We manage data reconciliation, error checks, and online submission for you.

- Timely Reminders: Stay on top of deadlines with automated alerts so you never miss your GSTR-9 due date.

- Secure & Confidential: Your financial data is protected with strict security measures.

- Affordable Pricing: Professional service at competitive rates for filing with no hidden fees.

What Our Clients Say

View AllMAYUR KAKADE

RegisterKaro has been an absolute game-changer for managing all our company's filings and legal requirements. From company incorporation to annual com... Read more

Kesha Ram

Register Karo is a company carryout all task which you demand from Registeration process to final compliance of commencement of the new company. My e... Read more

Jit

Register Karo is the best platform to register your company, @kajal chowhan helped me a lot, to make the process smoothly. Thank you team registerkaro

Guru

professional work, good team work by the team allocated to us, on time delivery for incorporation of my company, Ankit followed a good workflow throug... Read more

yayati

I reached out to registerkro for company windup. Would like to give shout out to Astha gupta who was extremly helpful throughout the process. Kudos to... Read more

Vijay Azad

Hi It was pleasure to contact you@alka for company registration .Happy with the dedication and support during process and working beyond timeline...

aravind raj

We did startup registeration with their team, it was point to point approach and they were clear in those procedures and their followup is too good...

vinay kumar

Your staff Ankita Matta is a polite person the way of handling the issues was good. I hope in future register karo team handle the issues in a same wa... Read more

Riya Singh

Register karo demonstrated professionalism and expertise in navigating complex legal and regulatory issues related to our industry. Special thanks Ank... Read more

ganesh patil

Had a great experience with Register Karo. The LLP registration process was handled smoothly and everything was explained clearly. Highly recommended!

Related Blogs

View All

Top 10 CA Firms in Kolkata 2026: Best Chartered Accountants for Audit, Tax, GST & Compliance

Top 10 CA Firms in Mumbai 2026: Big 4, Mid-Size List

Top 10 CA Firms in Delhi: A 2026 Guide to Big 4, Mid-Size & Local Firms

")

How to Register a Company in Bangalore: A Complete Step-by-Step Guide (2026)

Top 10 CA Firms in Bangalore 2026: Best Chartered Accountants List

")

Startup India Certificate: How to Get, Download & Verify DPIIT Recognition (2026)

Startup India Registration Fees in 2026: Complete Cost & Charges Breakdown

Singapore Company Registration Fees in 2026: Cost Breakdown for Indians

UK Company Registration Fees in 2026: Cost Breakdown for Indians

Nidhi Company Registration Fees in India: Govt Costs & Other Charges

Featured In